Stocks remain rangebound amid AI disruption

E*TRADE from Morgan Stanley

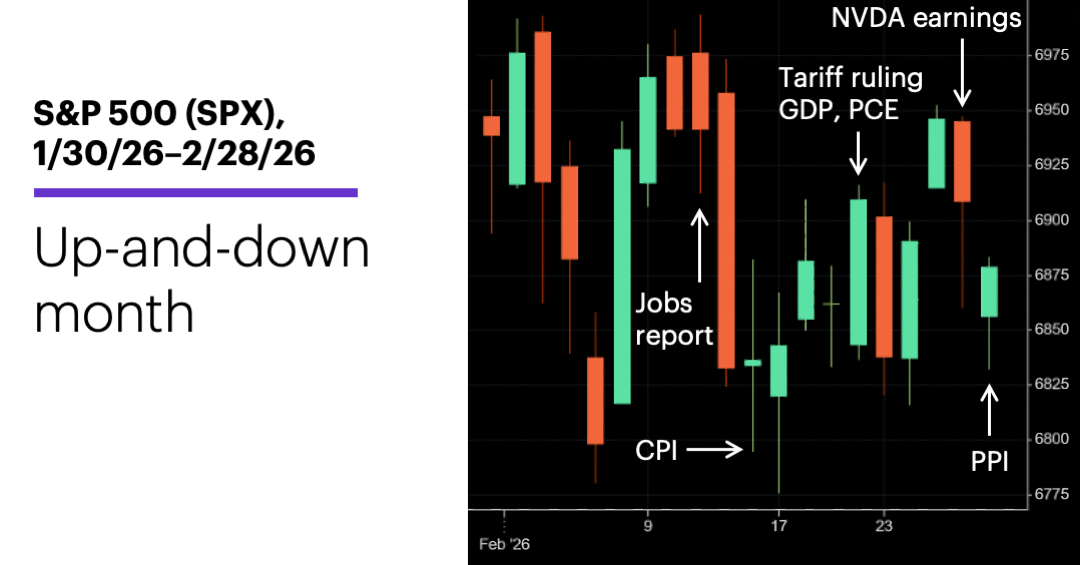

More up-and-down trading last month left the US stock market in a familiar position—not too far from record highs, but still locked in a multi-month consolidation.

The geopolitical and policy issues that monopolized headlines in January initially gave way to a series of “AI disruptions” in February, followed by a renewed focus on tariffs later in the month. Then, after the final trading day of the month, geopolitics returned to the forefront amid US-Israeli strikes against Iran. More broadly, “tech rotation” remained an important market theme, as investors continued to move away from many of the market’s longstanding megacap leaders.

The S&P 500 (SPX) tested the upper and lower boundaries of its multi-month consolidation early in February, ending the month near the middle of that range as another bout of tech selling unfolded in the wake of AI chip leader NVIDIA’s (NVDA) coolly-received earnings release:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.)

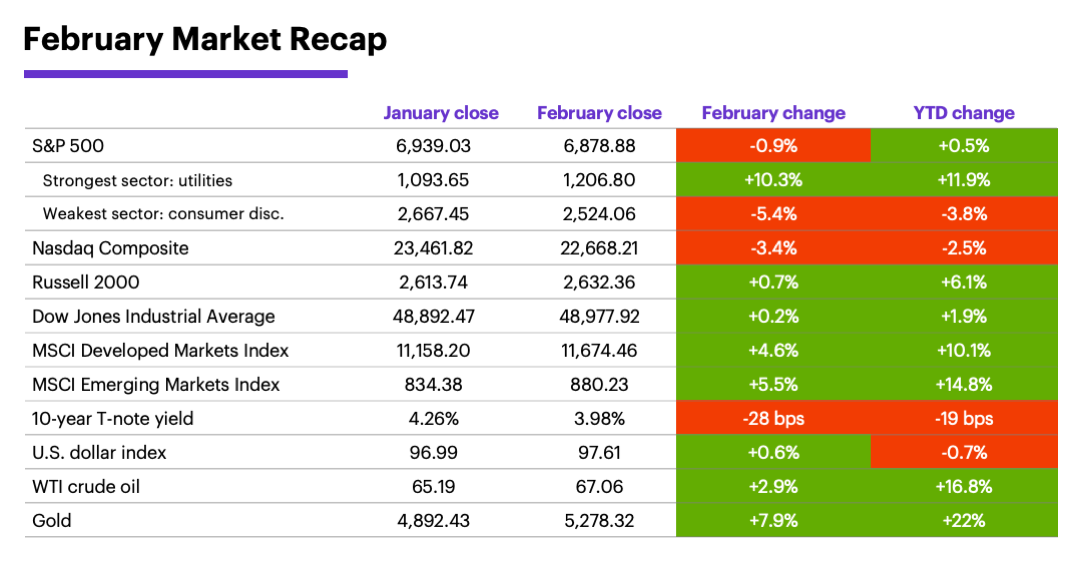

Utilities was the strongest S&P 500 sector (followed by energy), while consumer discretionary was the weakest (followed by communications services). Rising oil prices (as US-Iran tensions escalated) buoyed energy stocks for much of the month, while the rotation away from megacap tech leaders weighed on the communications services sector.

Mid-cap and small-cap stocks led the US stock market again in February. The S&P 400 (MID) mid-cap index gained 4% in February—far more than any other major US index. In terms of small-cap stock selection, Morgan Stanley & Co. strategists favor S&P 600 names over the Russell 2000, because the former index is “higher quality and less geared toward speculative growth areas.”1

The US stock market fell further behind global markets. The MSCI developed and emerging markets indexes both gained ground in February, expanding their ongoing outperformance over US stocks.

Bonds rallied as yields declined, while the dollar and gold both climbed. The benchmark 10-year Treasury yield fell more than it has in any month since February 2025, while the US dollar Index climbed modestly. Gold extended its rally, despite more volatility in the precious metals arena.

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment). Past performance is not indicative of future results.

Opportunities amid the disruption? The concerns about GenAI undermining traditional business models that initially hit software stocks spread to other areas of the market in February, including financial (insurance and brokerage) and cybersecurity stocks. But Morgan Stanley & Co. strategists argued that some of these setbacks may present opportunities in “well-positioned incumbents” and “AI adopters with pricing power.”2

A new chapter opened in the tariff story. While the Supreme Court’s February 20 ruling struck down the tariffs President Trump implemented using the International Emergency Economic Powers Act (IEEPA), it left others intact. Also, the White House quickly announced new tariffs (15%)—which Congress would need to extend after 150 days—to replace the ones the Court nullified.

But the latest developments may have made lower tariffs more likely in the long run, according to Morgan Stanley & Co. strategists. While acknowledging the uncertainty surrounding the newly announced tariffs, they also noted the Court’s ruling and the White House’s subsequent pivot were in line with their expectations, and did not alter their US economic outlook.3

While subsectors like software are “rightly being questioned, they should produce both winners and losers.”

A “broadening” stock market doesn’t mean everything will go up. While some investors appear to view stock market rotation merely as “tactical repositioning,” Morgan Stanley Wealth Management argues for a more cautious view. Instead of chasing small-caps and low-quality momentum trades, they lean toward “quality opportunities among industrials, energy, materials and financials, which we believe will benefit from the productivity/capex-renaissance theme.” They also note that while “subsectors like software are rightly being questioned,” they will likely produce both winners and losers.4

Insight of the month: Identifying disruption risk. Morgan Stanley & Co. research showed that portfolios of AI adopters have underperformed AI infrastructure stocks year to date because of the adopters’ much higher “service exposure”—that is, they provide services more easily replaced or marginalized by GenAI. AI infrastructure stocks, by contrast, are more insulated from this risk, while also benefiting from “demand for compute, semiconductors, and enabling hardware.”5

Sticky inflation will likely keep the Fed on hold in March. Last month’s inflation data were mixed, leaning more hot (PPI and PCE Price Index) than cool (CPI). With labor-market numbers remaining solid, the Fed appears to have little incentive to cut interest rates at its March meeting, despite last month’s weaker-than-expected GDP reading.

March market history. The third month of the year has been net bullish for US stocks in the long run, but its returns have been middle of the road compared to other months. March was positive for the S&P 500 in 63% of all years since 1991 (fifth place), with a 1.1% median return (seventh place).6

Important March dates: Employment Report (3/6), CPI (3/11), PPI (3/12), GDP (3/13), PCE Price Index (3/13), retail sales (TBD), Fed interest rate decision (3/18).

1 MorganStanley.com. Weekly Warm-up: Are Structural AI Disruption Fears Premature? 2/17/26.

2 MorganStanley.com. AI Disruption Debate: Our Analysts Weigh In. 2/25/26.

3 MorganStanley.com. Global Tariffs: Moving Past IEEPA. 2/23/26.

4 MorganStanley.com. The GIC Weekly: The New Productivity Dynamics. 2/23/26.

5 MorganStanley.com. Quantified Thematics: AI Infrastructure Best Positioned vs. Service Disruption. 2/13/26.

6 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2025. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.