Tech continues to carry the torch

E*TRADE from Morgan Stanley

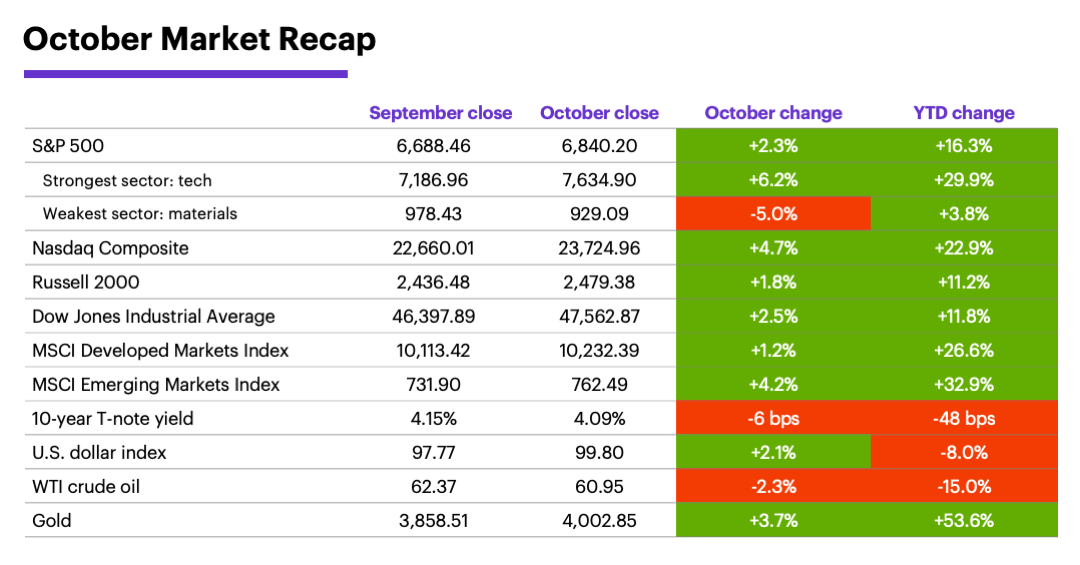

The US stock market’s recovery from its turbulent spring extended into the fourth quarter, as the major indexes hit new highs in October against the backdrop of strong corporate earnings and continued AI enthusiasm.

While the S&P 500 posted its sixth-straight up month and extended its rally off the April lows to 37%, the month was not without its bumps. On April 10, the S&P 500 experienced its biggest down day since April when President Trump proposed renewed tariffs on China because of their restriction on exports of “rare earths.” (In a late-month trade deal, China agreed to postpone its restrictions for a year, while the US agreed to give Chinese companies access to its tech.)

Also, while the Fed lowered interest rates by 0.25% late in the month, Chairman Jerome Powell appeared to catch the market off guard by casting a measure of doubt on a December cut.

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.)

Stocks looked past the government shutdown and the partial “data vacuum” it created. The closure canceled the release of the monthly jobs report and the initial Q3 GDP reading, among other data. Ellen Zentner, Chief Economic Strategist & Global Head of Thematic Investing for Morgan Stanley Wealth Management, noted that the private data that has been available hasn’t indicated the labor market is falling off a cliff or inflation is surging. The delayed Consumer Price Index (CPI) came in cooler than expected.

AI continued to drive tech, and tech continued to drive the market. Tech strength—the sector gained nearly twice as much as any other in October—fueled the Nasdaq Composite index’s market-leading October gain, while the materials sector lost the most ground.

Gold hit new heights before losing some of its shine. Although gold extended its record-setting rally, it also experienced its first significant setback in months. Gold climbed nearly $500 intramonth to its October 20 record close of $4,356.40, then retreated more than $350 by the end of the month.

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment). Past performance is not indicative of future results.

The October Fed meeting wasn’t as cut-and-dried as expected. Along with two dissenting votes, the Fed Chair stressed a December rate cut was “not a foregone conclusion.” Morgan Stanley & Co. analysts see the Fed shifting back to a data-dependent stance, but “the key question is what data the Fed will have before December.”1 A prolonged government shutdown, they note, poses a risk to expectations for cuts at the next two meetings.

Megacap post-earnings stock performance was mixed. As of October 31, 64% of the S&P 500 had released their Q3 numbers, with 83% reporting positive EPS surprises and 79% reporting positive revenue surprises.2 Although four of the five “Magnificent 7” stocks that reported in the final week of the month topped their headline estimates, only two (Alphabet, Amazon) rallied after releasing their numbers, while three (Meta, Microsoft, Apple) initially declined.

The near-term performance of these stocks bears watching, according to Morgan Stanley strategists. They argued the post-earnings stock performance of the “AI hyperscalers”—Alphabet, Amazon, Microsoft, and Meta—could indicate whether earnings revision breadth was likely to rebound for the broader market. The analysts are currently bullish on US stocks, based on expectation for better and broader earnings growth next year.3

Talk of an AI capital expenditures bubble may be exaggerated. While acknowledging the risk that some companies in the AI space may “build too much,” resulting in lower returns or losses, Morgan Stanley & Co. points out that AI datacenters are still seeing strong underlying demand, and are often backed by companies (e.g., the AI hyperscalers) with exceptionally good resources.4

With electricity demand growing faster than the utility industry can manage, renewables and gas turbines could be key to powering AI in the near future.

Insight of the month: energy “growth enablers.” With AI electricity demand outpacing the utility industry’s ability to supply it, Morgan Stanley & Co. strategists recently identified companies positioned to benefit from “a long runway in demand” for renewables and gas turbines to power AI over the next decade. They also highlight opportunities in existing power plants and small-scale energy solutions they believe will become increasingly valuable as data centers stretch the energy grid’s capacity.5

November market history. November has been one of the strongest months for US stocks over the past seven decades, and especially over the past 30 years. Since 1995, the S&P 500 (SPX) gained ground in November 24 out of 30 times (80%, the highest winning percentage of any month) with a median return of 3.1% (larger than any other month).6

Key October dates (subject to cancellation or delay because of government shutdown): JOLTS (11/4), ADP Private Employment (11/5), CPI (11/13), PPI (11/14), retail sales (11/14), FOMC minutes (11/19), Q3 GDP (11/26), PCE Price Index (11/26), Thanksgiving, US markets closed (11/27).

1 MorganStanley.com. October FOMC Reaction: Back to Data Dependence. 10/30/25.

2 FactSet. Earnings Insight. 10/31/25.

3 MorganStanley.com. Will the Stock Market’s Rally Continue? 10/27/25.

4 MorganStanley.com. Should AI Spending Worry Investors? 10/23/25.

5MorganStanley.com. The Future of Energy in the Data Era. 10/28/25.

6 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2024. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.