Politics, commodities star early in 2026

E*TRADE from Morgan Stanley

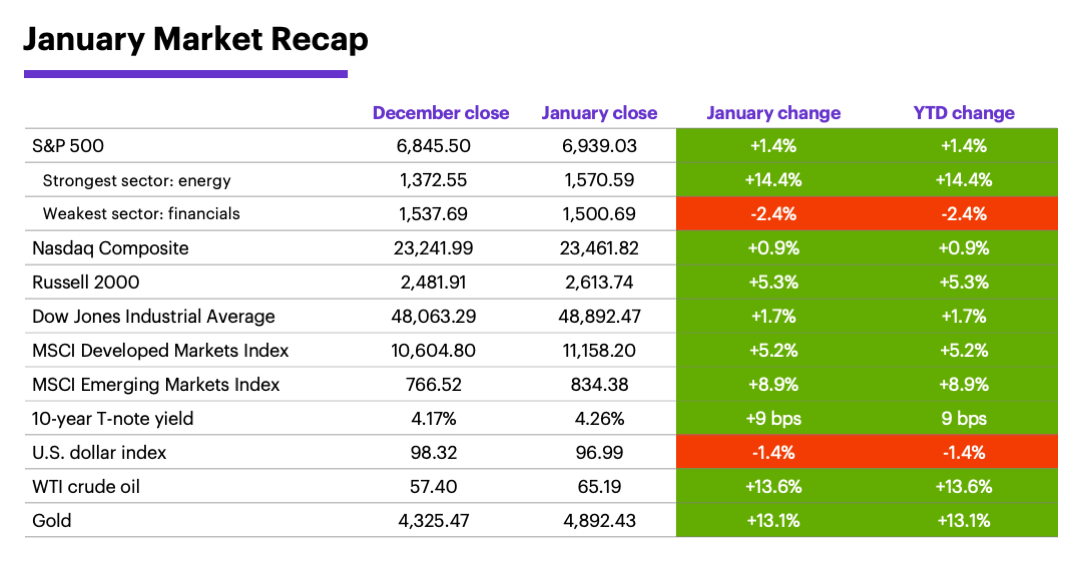

US stocks climbed the first month of the New Year, but continued to search for sustained momentum—leaving commodities as January’s most-compelling market story.

Despite the beginning of a new earnings season last month, day-to-day equity market action often appeared to take its cues from political and policy headlines: a US military operation in Venezuela, White House proposals to cap credit card interest rates at 10% and allow investors to use 401(k) funds to make home purchases, and renewed challenges to Fed independence.

However, geopolitics proved to be the most significant source of volatility in January. The White House’s pursuit of Greenland became a growing source of tension with Europe. The S&P 500 tumbled to a one-month low as the rhetoric escalated, but reversed after President Trump announced the US would not use force to acquire the arctic territory:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.)

The Russell 2000 small-cap index was the strongest US stock index in January, despite losing some momentum late in the month. The S&P 400 mid-cap index also outperformed the S&P 500.

But US stocks underperformed global markets. The S&P 500 trailed both developed and emerging-markets last month (especially the latter)—a 2025 trend that extended into in the first month of 2026.

The Fed hit the pause button, and a new Chair emerged. The Fed left rates unchanged last month as the labor market showed few signs of further weakening and inflation remained elevated but stable. On January 30, President Trump tapped Kevin Warsh to replace Fed Chair Jerome Powell—a move some interpreted as a positive sign for Fed independence, and a possible catalyst for the reversal of “safe-haven” buying in precious metals. The nomination did not change Morgan Stanley & Co. strategists' expectation for two further rate cuts in the second half of the year.

Precious metals weren’t the only commodity story. Gold prices rallied nearly $1,300 (+29%) intramonth in late January (approaching $5,600), while silver surged as much as $50 (70%) to $121.60—before both markets crumbled on January 30, giving back more than half of the month’s gains. US crude oil posted its first monthly gain since last July, jumping more than 13%, while natural gas jumped nearly 18%.

Last month’s moves in the metals and energy markets rippled well beyond the commodities arena.

Commodities impacted stock sector performance. Materials, which had been one of the month’s strongest S&P 500 sectors on January 29, ended the month as one of its weakest. Meanwhile, the crude oil and natural gas rallies helped make energy the month’s strongest sector.

US dollar weakness may have helped the metals rally. The US dollar Index fell to its lowest level in nearly four years before bouncing in the final days of the month. The benchmark 10-year Treasury yield jumped to its highest level since last August during the Greenland dispute, then retreated to end the month only modestly higher.

Chip stocks stood out in a tepid month for tech. Some semiconductor companies specializing in computer memory enjoyed strong rallies amid concerns about a potential “memory bottleneck” driven by AI datacenter growth.1

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment). Past performance is not indicative of future results.

Despite shrinking odds for Fed rate cuts this year, Morgan Stanley & Co. strategists saw the potential for additional upside in small caps. Earnings growth for these stocks, they note, is at its strongest level since 2022, and relative earnings revisions breadth vs. large caps recently accelerated.2

Morgan Stanley Wealth Management was more cautious about the long-term small-cap outlook. While “the procyclical playbook might support them,” the strategists describe earnings forecasts of 25%–30% for profitable small caps as “ambitious.” They favor large-cap core and quality names, “broadening to GenAI productivity beneficiaries in financials, health care and energy,” as well as adding to holdings in non-US stocks, with a focus on emerging markets.3

Key AI players may attempt to gain greater control of energy infrastructure in 2026.

Insight of the month: AI leaders embed more deeply in energy. In sharing their four key themes for 2026—Tech Diffusion, The Future of Energy, The Multipolar World, and Societal Shifts—Morgan Stanley & Co. strategists argue that key AI players will likely attempt to gain greater control of energy infrastructure, with implications for natural gas, nuclear, and other energy stocks.4

February market history. February has never been consistently positive for the S&P 500. Since 1957, it was an up month 52% of the time (second lowest), with a 0.2% median return (third lowest). The S&P lost ground in six of the past 10 Februaries.5

Key February dates: Employment Report (2/6), retail sales (2/10), CPI (2/11), Presidents’ Day, US markets closed (2/16), housing starts (2/18), FOMC minutes (2/18), GDP (2/20), PCE Price Index (2/20), PPI (2/27).

1 MorganStanley.com. Memory—How to Play the New AI Bottleneck. 1/15/26.

2 MorganStanley.com. Weekly Warm-up: Key Debates & Earnings Season Chartbook. 1/20/26.

3 MorganStanley.com.MorganStanley.com. The GIC Weekly: Small-Cap Trade. 1/26/26.

4 MorganStanley.com. The World Through a Thematic Lens: Predictions, Debates and Structural Change. 1/18/26.

5 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2025. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.