Tech stumbles, but market well-positioned for 2026

E*TRADE from Morgan Stanley

Given US stocks cruised through the often-volatile months of September and October, their challenges during the historically bullish month of November could simply be viewed as the latest seasonal twist in a year that has had several of them.

The pullback didn’t materialize out of thin air, however. The engine that drove the rally off the April lows—tech, specifically AI—throttled back amid concerns about the level of corporate investment in AI, especially in light of the apparently “circular” nature of some of the financing.1

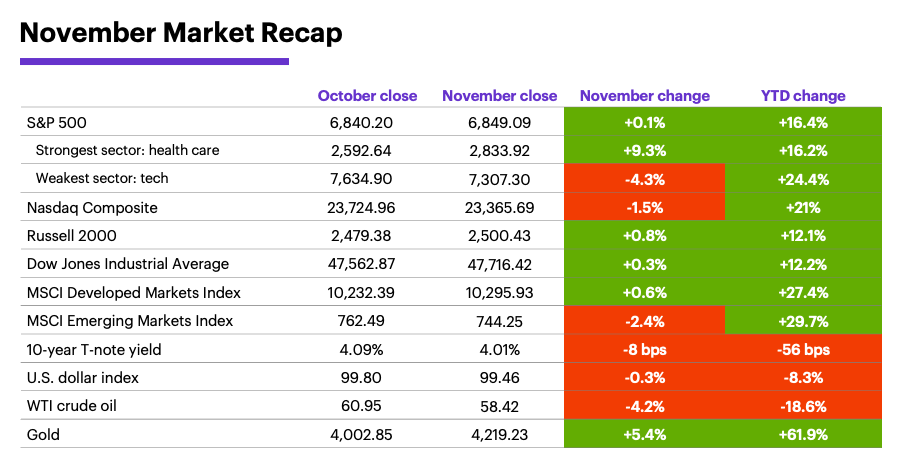

Nonetheless, by the end of the month the damage for the broad market was limited. Despite closing at a 10-week low on November 20—at which point it was down 4.4% for the month—the S&P 500 (SPX) rebounded to end November with a marginal gain:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.)

The level of anxiety about the market’s relatively modest retreat may have reflected how accustomed investors had become to a market, and especially a tech sector, that had rallied almost without pause since April. The Nasdaq 100’s (NDX) 48.6% gain between April 4 and October 31 was the tech index’s strongest 31-week rally since 2020, and its fifth-strongest of the past 25 years.

As usual, NVIDIA was at the center of the AI discussion. Tech stocks were already in pullback mode by the time flagship AI chipmaker NVIDIA released earnings on November 20. But healthy Q3 numbers and bullish forward guidance didn’t prevent the stock from losing ground, further undermining AI-trade sentiment—at least briefly.

Health care’s vital signs continued to improve. The long-dormant health care sector led the US market last month, building on its second-half turnaround. At the end of July, health care was down more than 4% for the year. At the end of November, it was the year’s fifth-strongest sector, and lagged tech by just a little more than eight percentage points.

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment). Past performance is not indicative of future results.

The debate surrounding the AI trade is “necessary and healthy,” according to Morgan Stanley Wealth Management. That said, they continue to see opportunities to “buy winners among the Mag 7 and add to quality AI adopters in financials, health care, and energy.”2 Daniel Skelly, Head of Morgan Stanley's Wealth Management Market Research & Strategy Team, noted that “while some market voices continue to obsess over an AI crash, what we saw recently was no more than a fender bender.”

Longer term, Morgan Stanley & Co. strategists believe we’re in a new bull market and earnings cycle, especially for many of the lagging areas of the S&P 500. While they acknowledge risks to this outlook (e.g., a too-hawkish Fed in the short term and possible inflation in the longer term), they upped their 2026 S&P 500 price target to 7,800. They also expect market leadership to broaden, resulting in small caps outperforming large caps and cyclicals outperforming defensives.3

Markets may also benefit from a more settled US policy landscape. After a turbulent 2025, the economy should emerge from public policy uncertainty next year and in 2027, argue Morgan Stanley & Co. economists. Fluidity surrounding trade, immigration, deregulation, and fiscal policy—all of which contributed to market uncertainty—has given way “discernible set pieces,” resulting in a base-case forecast for modest growth, decelerating inflation, and more Fed rate cuts.4

That’s just one of the factors that could be setting up a US-led “risk reboot” in 2026, according to Morgan Stanley & Co. analysts. Against a backdrop of increased global risk appetite, the strategists favor equities over credit and government bonds, and they expect US stocks to outperform their international counterparts. Among the latter, they highlight Japanese stocks, where “the positive narrative resembles the US story.”5

A strong first half of 2026 for EM fixed-income investments could give way to a bumpy landing in the second half.

Insight of the month: The time window for emerging-market (EM) bonds. As a great year for EM fixed-income investors winds down, Morgan Stanley & Co. analysts see the bull market continuing in the first half of 2026, supported by lower yields, tight spreads, and stronger EM currencies. But noting that “all good things must come to an end,” they suspect a reaccelerating US economy and the end of easing cycles will lead to a “bumpy EM landing” sometime in the second half of the year.6

December market history. Between 1957 and 1990, December was a positive month for the S&P 500 more often than any other (70.6% of the time), and had the third-largest median return (1.5%). Since then, it’s been an up month 73.5% of the time (second-highest of all months), while it’s median return slipped to 1.1%.7

Key December dates: ADP Private Employment (12/3), ISM Services Index (12/3), PCE Price Index (12/5), Fed interest rate decision (12/10), PPI (12/11), housing starts (12/16), retail sales (12/17), CPI (12/18), Q3 GDP (12/23), Christmas, US markets closed (12/25), FOMC minutes (12/30).

1 MorganStanley.com. AI: Mapping Circularity. 10/8/25.

2 MorganStanley.com. CIO Update from Lisa Shalett. 11/24/25.

3 MorganStanley.com. 2026 US Equities Outlook: The Rolling Recovery Is Here. 11/17/25.

4 MorganStanley.com. Emerging from Policy Uncertainty. 11/16/25.

5 MorganStanley.com. The Year of Risk Reboot. 11/16/25.

6 MorganStanley.com. Good Times Roll On. 11/17/25.

7 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2024. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.