Stocks extend September “surprise”

- Fed cuts rates, stocks climb to new highs

- Tech leads. small caps close behind

- This week: Fed inflation, durable goods

If September is going to exhibit “seasonal weakness,” it has a little over a week to do it.

Aside from a stumble at the outset, September has so far been a breakout month for US stocks, and the S&P 500 (SPX) padded its gains last week, rallying to fresh highs as the Federal Reserve delivered its first rate cut since December 2024:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Lower rates, higher stocks.

The fine print: Away from the spotlight of the Fed’s rate cut, most of last week’s economic data suggested the economy was still on solid ground. Retail sales were stronger than expected, while jobless claims came in below estimates after hitting a multi-year high a week earlier.

The number: 3. Ellen Zentner, Chief Economic Strategist for Morgan Stanley Wealth Management, expects the Fed to cut rates three more times (into the first quarter of 2026) before pausing.1

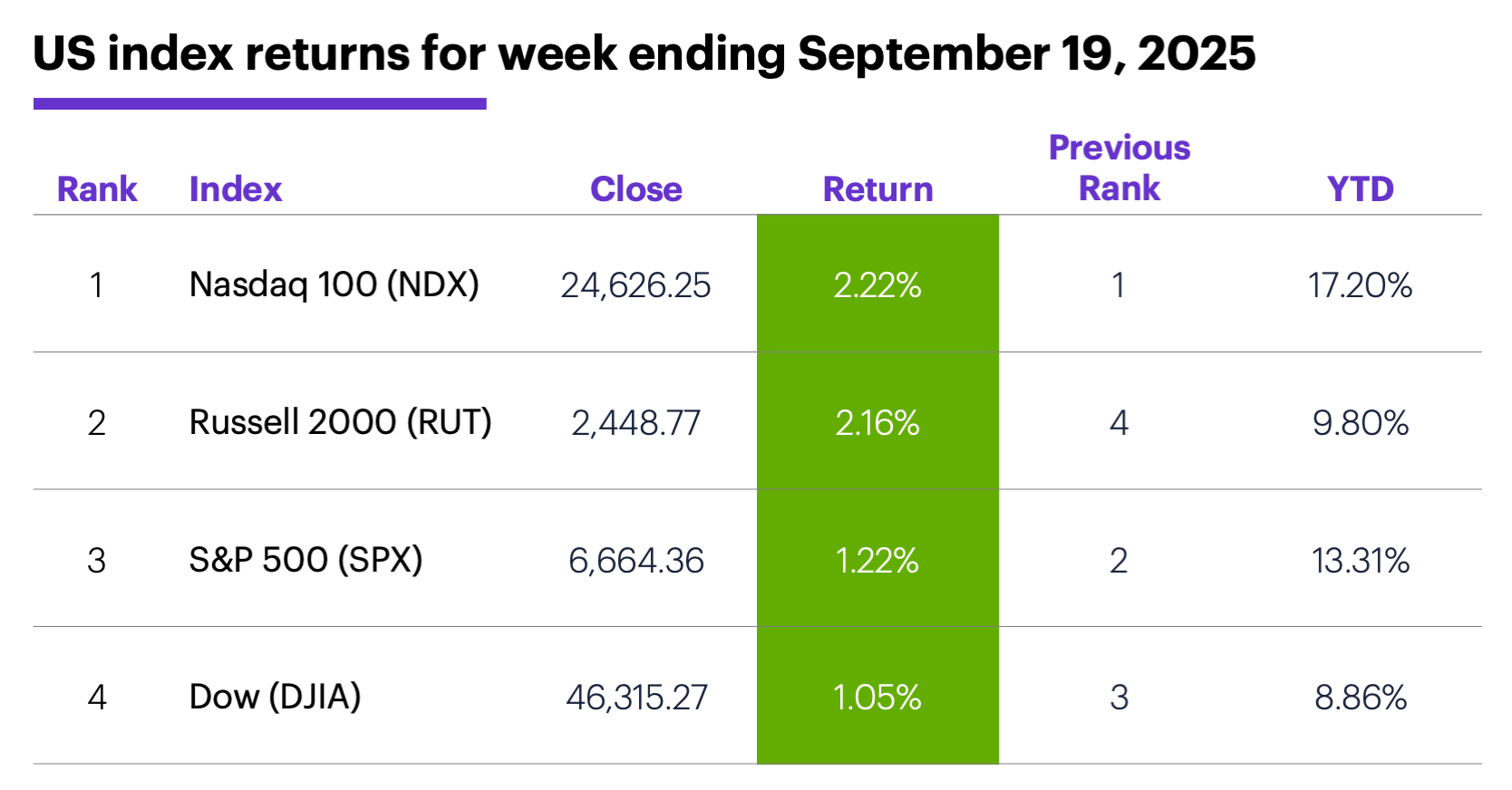

The scorecard: The Nasdaq 100 (NDX) tech index led the market for a second week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were communication services (+3.4%), information technology (+2.1%), and consumer discretionary (+1.5%). The weakest sectors were real estate (-1.4%), consumer staples (-1.3%), and materials (-0.9%).

Stock moves: Webtoon Entertainment (WBTN) +39% to $20.80 on Tuesday, Intellia Therapeutics (NTLA) +30% to $16.11 on Thursday. On the downside, Dave & Buster's (PLAY) -17% to $20.14 on Tuesday, CEA Industries (BNC) -24% to $10.90 on Thursday.

Yields: Last week the 10-year US Treasury yield climbed 0.07% to a two-week high of 4.13%.

US dollar: Despite dropping to a year-to-date intraday low last Wednesday, the US Dollar Index (DXY) ended the week up 0.09 to 97.64.

Futures: December gold (GCZ5) pulled back after hitting record highs last Monday and Tuesday, but rebounded Friday to end the week up $19.40 at $3,705.80. November WTI crude oil (CLX5) ended an up-and-down week $0.02 lower at $62.40. Biggest rallies: October milk (DCV5) +5.3%, December whey (DYZ5) +4.1%. Biggest declines: December coffee (KCZ5) -7.7%, December palladium (PAZ5) -6.5%.

Coming this week

This week’s numbers include the Fed’s preferred inflation gauge (PCE Price Index) and the final reading on Q2 GDP:

●Monday: Chicago Fed National Activity Index

●Tuesday: Q2 current account, S&P Manufacturing and Services PMI (flash), existing home sales

●Wednesday: new home sales

●Thursday: Q2 GDP (final estimate), durable goods orders, trade balance in goods (advance), retail and wholesale inventories

●Friday: PCE Price Index, personal income and spending, consumer sentiment (final)

This week’s earnings include:

●Monday: Progress Software (PRGS)

●Tuesday: AutoZone (AZO), Micron (MU)

●Wednesday: Cintas (CTAS), KB Home (KBH), Thor Industries (THO)

●Thursday: Accenture (ACN), Concentrix (CNXC), Costco (COST), Jabil (JBL), CarMax (KMX), TD SYNNEX (SNX)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Currently the most magnificent

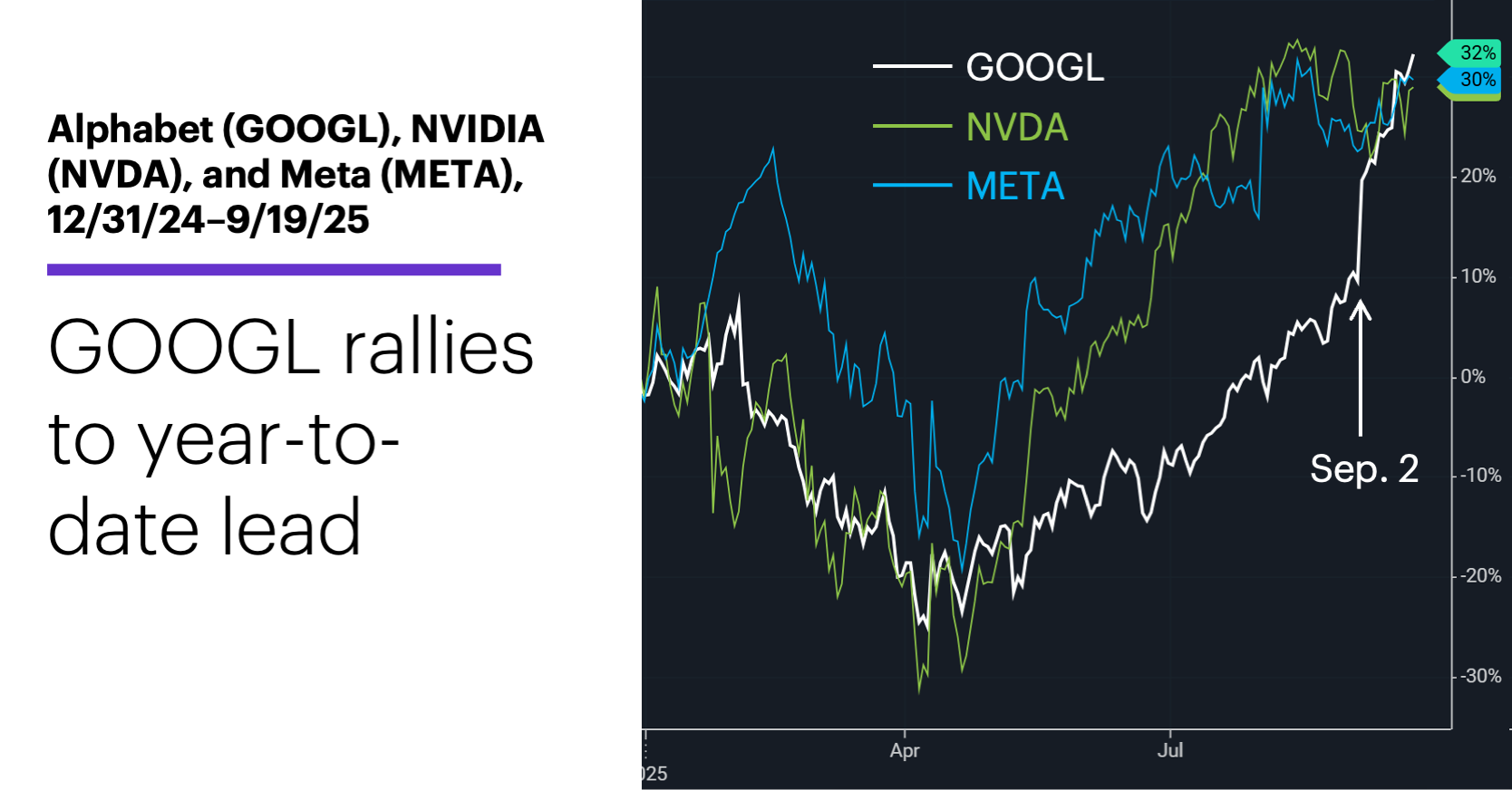

If it wasn’t exactly the omega of the Magnificent 7 stocks last year, at the end of last week Alphabet (GOOGL) could certainly claim the alpha title for this year.

After posting the third-lowest returns of the Mag-7 cohort in both 2023 and 2024, GOOGL finds itself with 2025’s highest year-to-date return, thanks mostly to a 20.5% surge since September 2 driven by a favorable federal court ruling in the antitrust case against the company:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

To be clear, GOOGL’s performance the past two years could be described as sub-par only relative to its Mag-7 companions—it gained 35.5% in 2024 and 58.3% in 2023. And although it is only incrementally outperforming its nearest competitors this year—NVDIA (NVDA) and Meta (META)—the fact that it was trailing both stocks by a wide margin at the end of August highlights how strong this month’s rally has been.

Alphabet’s surge also explains much of the recent strength in the communications services sector (META is also a component), which was the S&P 500’s strongest sector last week, for the past month, and year to date.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 Morgan Stanley.com. Macro Update. 9/18/25.