Stocks weather geopolitical disruption

- Stocks and bonds fall, oil surges, dollar climbs

- March rate cut still unlikely despite jobs report miss

- This week: Inflation data, GDP, housing starts

Last week started with a geopolitical surprise and ended with an economic one. The result was a volatile stock market, but one that was perhaps not as negative as some may have expected, given the nature of the week’s headlines.

US-Israeli attacks on Iran pushed AI disruption concerns to the back burner and sent oil prices to their highest level since September 2023, reigniting inflation concerns and prompting debate about the economic impact of a potentially prolonged conflict.

While the S&P 500 (SPX) lost ground for the week and fell to new year-to-date lows, it nonetheless remained within its nearly five-month trading range. The market also displayed a certain measure of resilience by repeatedly trimming intraday losses by the close—including on Friday, when the monthly jobs report showed the second-biggest drop in payrolls in more than five years:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Market tests range lows amid geopolitical, energy uncertainty.

The fine print: The fine print: Given the overwhelming focus on geopolitics and oil prices, the fact that the battered tech sector had a relatively solid week may have slipped under the radar. Tech was the second-strongest S&P 500 sector (even though it posted a small loss), and the Nasdaq 100 (NDX) tech index had the smallest loss of any major US stock gauge.

The number: 92,000, the decline in US jobs in January. Over the past five years, only the October 2025 drop of 140,000—stemming from the government shutdown—was larger.

The move: 2%, the increase in the odds (to 4.5%) of a Fed rate cut later this month. While the soft jobs report may have, in other circumstances, increased the probability of a cut, the potential inflation risk posed by surging oil prices will likely keep the Fed on hold.

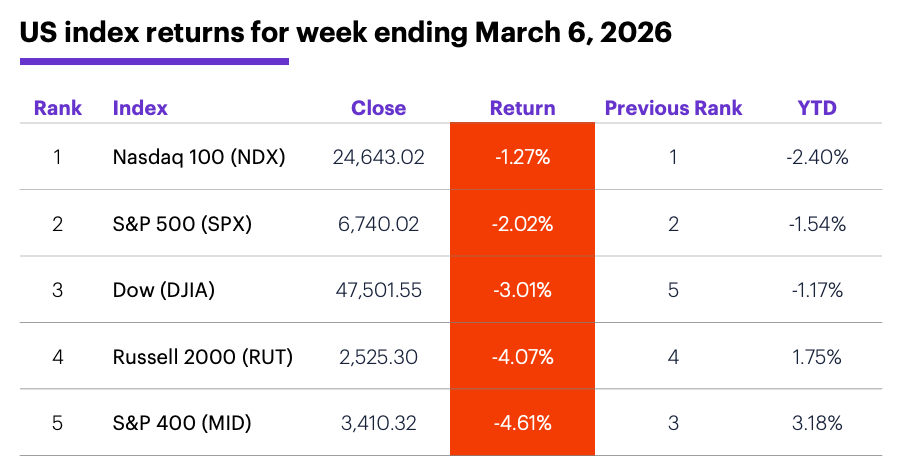

The scorecard: The Russell 2000 (RUT) small-cap and S&P 400 (MID) mid-cap indexes were the only major indexes that weren’t in the red for the year as of Friday, but they also posted the biggest losses last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were energy (+0.6%), information technology (-0.3%), and consumer discretionary (-1.3%). The weakest sectors were materials (-7.2%), consumer staples (-4.9%), and health care (-4.6%).

Stock moves: Arcellx (ACLX) +77% to $113.75 on Monday, Clear Secure (YOU) +39% to $46.51 on Wednesday. Oddity Tech (ODD) -49% to $14.74 on Wednesday, UniQure (QURE) -31% to $17.12 on Thursday.

Yields and the dollar: The 10-year US Treasury climbed 0.19% to 4.15%. The US Dollar Index (DXY) rallied 1.38 to 99.99.

Futures: Crude oil jumped more than it has in any week in more than four decades. April WTI crude oil (CLJ6) surged $23.88 to $90.90—a 35.6% increase. April gold (GCJ6) surprised many traders by declining (along with other precious metals) during a turbulent week, falling $89.20 to $5,158.70. Biggest gains: April heating oil (HOJ6) +39.5%, April WTI crude oil (CLJ6) +35.6%. Biggest declines: June Lithium (LTHM6) -10%, April platinum (PLJ6) -9.8%.

Coming this week

Inflation data and revised GDP are among the highlights of a busier-than-usual week after the monthly jobs report:

●Monday: New York Fed Consumer Inflation Expectations

●Tuesday: NFIB Business Optimism Index, Existing Home Sales

●Wednesday: Consumer Price Index (CPI)

●Thursday: Housing Starts and Building Permits, Trade Balance

●Friday: PCE Price Index, Personal Income and Spending, Durable Goods Orders, GDP (Q4, second estimate), Job Openings and Labor Turnover Survey (JOLTS), Consumer Sentiment (prelim)

More retail earnings are on tap this week, but Oracle (ORCL) and Adobe (ADBE) represent the tech contingent:

●Monday: BJ's Wholesale Club (BJ), Casey’s General Stores (CASY), Hewlett Packard Enterprise (HPE), Korn Ferry (KFY), Oracle (ORCL)

●Tuesday: BioNTech (BNTX), Duluth Holdings (DLTH), Groupon (GRPN), Kohl’s (KSS), Limoneira (LMNR), United Natural Foods (UNFI)

●Wednesday: Campbell's (CPB), Descartes Systems Group Inc (DSGX), G-III Apparel (GIII), UiPath (PATH), Stitch Fix (SFIX)

●Thursday: Adobe (ADBE), Buckle (BKE), Dollar General (DG), Dick's Sporting Goods (DKS), Ulta Beauty (ULTA)

●Friday: One Group Hospitality (STKS), Volkswagen AG (VWAGY)

The oil factor

A new report from Morgan Stanley & Co. reviews the economic and market implications across oil (and natural gas) prices ranging from $65-$130, and over periods lasting less than a month to multiple months.

The strategists note that even if geopolitical risks fade in the medium term, a supply-driven energy shock could lead markets to price for persistent inflation, reminiscent of 2022-2023 when bond-stock correlations broke down and cash was king.

They note that if the disruption is short-lived, history shows stock-market volatility tends to ease quickly “and the market returns to pre-event trades, with market leadership returning to cyclicals in the US and the AI supply chain internationally.” In an extended disruption scenario, they add, non-US equity markets move to their bear cases, with the greatest risk in “energy-deficit markets that will face supply-chain stress.”

For all scenarios, they prefer US assets (except investment-grade corporate bonds), given their more “defensive nature and better fundamentals.”1

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Energy Shocks in the Economy & Markets. 3/6/26.