Market weathers “disruptive” week

- Tech still soft as stocks retreat from highs

- Financial sector latest victim of AI concerns

- This week: Fed inflation, GDP, possible tariff decision

Tech weakness, concerns about AI disruption, and possible seasonal sluggishness conspired to pull stocks lower last week, extending the market’s multi-month search for sustained momentum.

Although rotation out of tech continued, financials led the S&P 500 (SPX) to the downside amid concerns that new GenAI apps and platforms could challenge some of the sector’s established businesses.

Unlike a week earlier, a strong Friday rally fizzled late the day, leaving the SPX in the red for the year at the end of the week. The pullback reaffirmed levels a little below 6,800 as short-term support—the lower boundary of the index’s ongoing trading range:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Stocks slip amid AI disruptions and continued tech rotation.

The fine print: Last week may have appeared to be simply an extension of the 2026 “tech rotation” story, but there was an important twist. While software had previously been the biggest drag on tech so far this year, that wasn’t the case last week. Instead, IT Services (-9.7%), Computers & Peripherals (-7.4%), and Communications Equipment (-3.3%) were the weakest industries in the S&P 500 tech sector. Software ended the week with a small gain (+0.1%).

The number: 130,000, the January payrolls increase from last Wednesday’s monthly jobs report—nearly double the estimate. Friday’s Consumer Price Index (CPI) was slightly cooler than expected, although higher shelter (housing) prices remained a fly in the ointment.

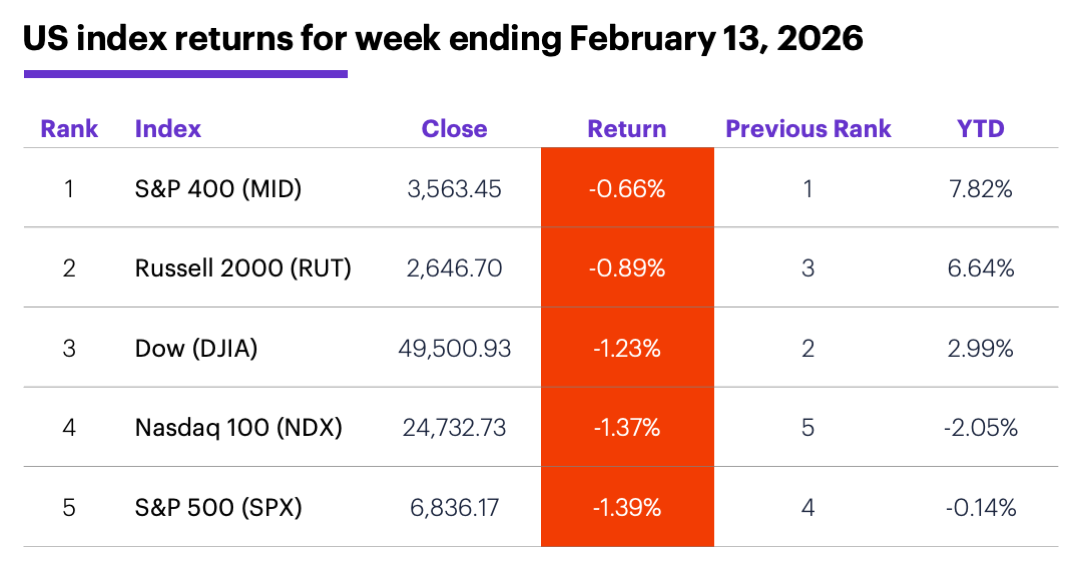

The scorecard: The Russell 2000 (RUT) small-cap index and the S&P 400 (MID) mid-cap index slipped the least last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were utilities (+6.8%), real estate (+3.5%), and materials (+3.4%). The weakest sectors were financials (-5.1%), communication services (-3.7%), and consumer discretionary (-2.3%).

Stock moves: Valaris (VAL) +34% to $83.82 on Monday, Nektar Therapeutics (NKTR) +51% to $56 on Tuesday. Kyndryl (KD) -55% to $10.59 on Monday, Upstream (UPB) -47% to $14.69 on Wednesday.

Yields and the dollar: The 10-year US Treasury yield fell 0.14% to a nine-week low of 4.06% last week—it’s biggest weekly decline since September. The US Dollar Index (DXY) fell 0.72 to 96.91.

Futures: April gold (GCJ6) ended an up-and-down week up $66.50 at $5,046.30. After rallying close to $66 last Wednesday, March WTI crude oil (CLH6) pulled back to end the week down $0.66 at $62.89. Biggest rallies: May orange juice (OJK6) +9.7%, March Lithium (LTHH6) +8.7%. Biggest declines: May cocoa (CCK6) -14.3%, April hogs (HEJ6) -6.8%.

Coming this week

The economic calendar is crowded, but there’s a possibility the week’s biggest development will be an unscheduled one—the Supreme Court’s ruling on the legality of tariffs, which could come on Friday:

●Tuesday: Empire State Manufacturing Index, NAHB Housing Market Index

●Wednesday: Housing Starts and Building Permits (delayed), Durable Goods Orders (delayed), Industrial Production and Capacity Utilization, FOMC minutes

●Thursday: Goods Trade Balance, Imports and Exports, Philadelphia Fed Manufacturing Survey, Pending Home Sales

●Friday: GDP (Q4, second estimate), Personal Income and Spending, PCE Price Index , Consumer Sentiment, New Home Sales, possible Supreme Court tariff ruling

This week’s earnings include:

●Tuesday: Constellation Energy (CEG), Shift4 Payments (FOUR), Penumbra (PEN), Energy Transfer (ET), Genuine Parts (GPC), KenVue (KVUE), LGI Homes (LGIH), Medtronic (MDT), Palo Alto Networks (PANW), Sunoco (SUN), Toll Brothers (TOL), Vulcan Materials (VMC)

●Wednesday: Analog Devices (ADI), First Majestic Silver (AG), Alibaba (BABA), Booking Holdings (BKNG), Copart (CPRT), Charles River Laboratories (CRL), Carvana (CVNA), DoorDash (DASH), Global Payments (GPN), Occidental Petroleum (OXY), Royal Gold (RGLD), SolarEdge Technologies (SEDG), Molson Coors (TAP), Verisk Analytics (VRSK)

●Thursday: Deere & Co. (DE), Lemonade (LMND), Newmont (NEM), Walmart (WMT),

●Friday: Halozyme Therapeutics (HALO), PPL (PPL)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Market Mover Update: Most of GlobalFoundries’ (GFS) heavy call options volume last Thursday turned out to be traders getting out of positions. The open interest (OI) in all but two of the most actively traded contracts was lower on Friday. The exceptions: the April $45 and $55 calls, which had steady and slightly higher OI, respectively (see “Chips on or off the table?”).

Disruption carousel

The concerns about AI disruption that have made software the S&P 500’s weakest industry so far this year made themselves felt in other areas of the market last week—if, perhaps, only temporarily.

Many insurance stocks sold off early last week after reports of a new GenAI insurance app, followed by similar pullbacks in brokerage and wealth-management names. Morgan Stanley & Co. strategists described the latter sell-off as “outsized and overdone,” noting that many of the firms were, in fact, positioned to benefit from AI-driven productivity gains.1

The fact that many of these moves moderated or partially reversed by the end of week suggests they may have been driven more by emotion than objective analysis. But that doesn’t mean similar moves won’t occur in other industries or sectors as new AI technologies emerge.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Thoughts on AI Disruption Fears Driving Sell-Off. 2/11/26.