Tech strengthens ahead of key earnings

- Stocks extend gains even as oil prices swing higher

- Semiconductors key tech sector strength

- This week: Megacap earnings, Fed meeting, PCE inflation, GDP

Entering what is arguably the most important stretch of earnings season, the US stock market is coming off a fourth-straight up week—despite continued geopolitical uncertainty and elevated oil prices. And while last week didn’t come close to matching the returns of the previous three, it marked the S&P 500’s (SPX) first four-week win streak since 2024.

After edging to an all-time high last Wednesday, the SPX slipped on Thursday as US oil prices jumped more than 4%. But the index regained its footing on Friday as oil pulled back and strong earnings from Intel (INTC) amplified bullish momentum in the tech sector:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Market extends record run.

The fine print: Despite the release of GDP and inflation data, this week is all about earnings. Daniel Skelly, Head of Morgan Stanley's Wealth Management Market Research & Strategy Team, notes positive results from the Mag-7 could drive the market’s next leg to the upside. Meanwhile, Morgan Stanley & Co. strategists note that Q1 and Q2 earnings estimates for the S&P 500 are up +1% and 4%, respectively, since the Iran conflict started, and that the numbers that have come out so far have been strong. The strategists identified a dozen stocks they believe could “move meaningfully” on higher earnings.1

The move: Avis-Budget (CAR) sold off 68% last Wednesday-Thursday, a stunning reversal of the massive “short squeeze” that had propelled the stock from $99.90 to $847.70—a nearly 750% rally—over the preceding month.2

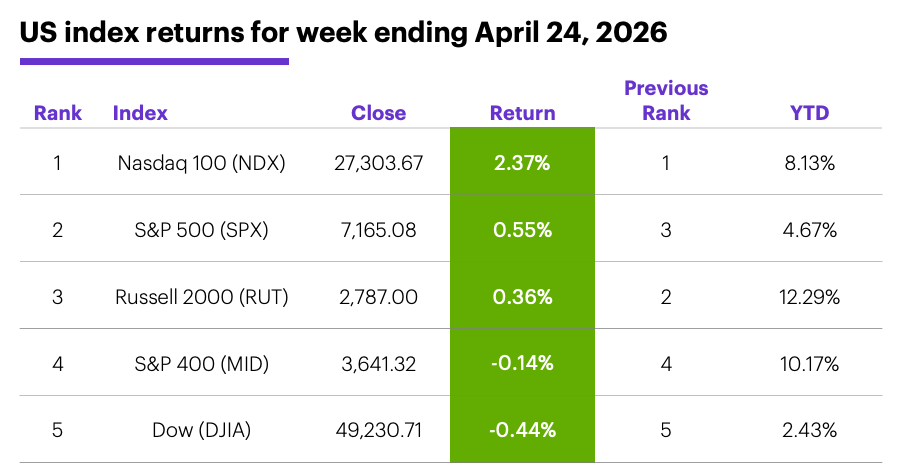

The scorecard: Index returns were mixed last week, but tech strength pushed the Nasdaq 100 (NDX) to a second-straight week of outperformance:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were energy (+3.2%), tech (+3.1%), and consumer staples (+1.2%). The weakest sectors were health care (-3.1%), financials (-1.9%), and real estate (-1.5%).

S&P 500 movers: Last week's strongest stocks were Advanced Micro Devices (AMD) +25% to $347.80, United Rentals (URI) +22% to $974.41, and Texas Instruments (TXN) +21% to $277.17. The weakest were Charter Communications (CHTR) -24% to $180.13, Tractor Supply (TSCO) -18% to $36.72, and Lululemon (LULU) -14% to $143.80. Other moves: Xanadu Quantum (XNDU) +52% to $34.75 on Wednesday, MaxLinear (MXL) +76% to $60.32 on Friday, ASGN (ASGN) -52% to $19.53 on Thursday.

Yields and the dollar: The 10-year US Treasury yield climbed 0.05% to 4.30% last week. The US Dollar Index (DXY) rallied 0.43 to 98.53.

Commodity futures: June WTI crude oil (CLM6) ended the week up $11.81 at $94.40. June gold (GCM6) fell $138.70 to $4,740.90. Biggest gains: June Brent crude oil (BM6) +16.3%, June heating oil (HOM6) +15.5%. Biggest declines: July orange juice (OJN6) -13.9%, May silver (SIK6) -6.7%.

Crypto: Bitcoin edged higher last week, rallying 0.4% to $77,455.31. Ethereum fell 4.4% to $2,315.69.

Coming this week

It’s the “big” week of earnings season—a loaded calendar of big tech (including five of the Magnificent 7) big oil, big pharma, and big consumer names. The following list scratches the surface:

●Monday: Bed Bath & Beyond (BBBY), Shift4 Payments (FOUR), Qorvo (QRVO), Repligen (RGEN), Rambus (RMBS), Sanmina (SANM), Verizon (VZ)

●Tuesday: Bloom Energy (BE), eBay (EBAY), Enphase Energy (ENPH), Corning (GLW), General Motors (GM), Kimberly Clark (KMB), Coca Cola (KO), Novartis (NVS), Pentair (PNR), Starbucks (SBUX), Silicon Motion Technology (SIMO), Spotify (SPOT), Seagate (STX), Teradyne (TER), T-Mobile (TMUS), Ultra Clean Holdings (UCTT), Visa (V)

●Wednesday: Chipotle (CMG), Ford (F), General Dynamics (GD), Alphabet (GOOGL), Kellogg (K), Lemonade (LMND), Mattel (MAT), McDonald's (MCD), Meta (META), Microsoft (MSFT), Phillips 66 (PSX), Regeneron (REGN), Yum Brands (YUM), Amazon (AMZN)

●Thursday: Baxter (BAX), Bristol Myers Squibb (BMY), Caterpillar (CAT), ConocoPhillips (COP), First Solar (FSLR), Hershey (HSY), Eli Lilly (LLY), Merck (MRK), Roblox (RBLX), Atlassian (TEAM), Valero Energy (VLO), Wayfair (W), Willis Towers Watson (WTW), Apple (AAPL)

●Friday: Aon (AON), Cboe Global Markets (CBOE), Colgate Palmolive (CL), Chevron (CVX), Estee Lauder Companies (EL), Exxon Mobil (XOM)

A Fed meeting—the final one chaired by Jerome Powell—shares this week’s economic calendar with the first estimate of Q1 GDP and the Fed’s inflation gauge (PCE Price Index):

●Tuesday: S&P Case-Shiller Home Price Index, FHFA House Price Index, Consumer Confidence

●Wednesday: Housing Starts and Building Permits, Durable Goods Orders, Trade Balance, Fed Interest Rate Decision

●Thursday: Q1 GDP (initial estimate), Personal Income and Spending, PCE Price Index, Chicago PMI

●Friday: S&P Global Manufacturing PMI, ISM Manufacturing Index

Insights from the oil futures market

Even though stocks climbed overall last week as crude oil edged higher, the market is still clearly concerned about high oil prices—it was no coincidence that the SPX’s two biggest down days (Tuesday and Thursday) were the two biggest up days for oil.

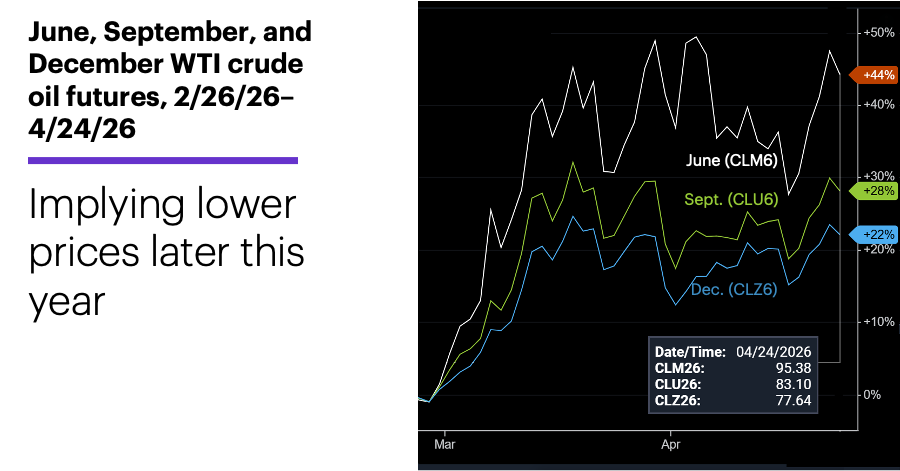

But how “concerned” is the oil market about higher oil prices? One way to possibly answer that question is to compare the prices of different crude oil futures contracts—for example, the June WTI oil futures (CLM6), the September futures (CLU6), and the December futures (CLZ6):

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

While the September and December contracts (green and blue lines, respectively) surged along with the June contract (white line) last month, they jumped much less—and were also less volatile.

But the price levels of the different contracts may be the most important takeaway. While the contract closest to expiration, June, closed above $95 on Friday, the September contract closed just above $83 and the December contract closed below $78—suggesting the futures market was expecting oil prices to be approximately $12 lower in September than they are now, and nearly $18 lower by December.

These expectations could certainly change based on events in the Middle East, but an oil market anticipating significantly lower prices by the end of the year may explain the stock market’s apparent inclination to look past the recent energy market volatility.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Conviction into Earnings. 4/21/24.

2 Barron’s. Avis Stock Falls 38% as Short Squeeze Shows Signs of Easing. 4/22/26.