Focus on earnings?

- Earnings recovery intact, says Morgan Stanley & Co.

- Early metrics highlight positive S&P 500 trends

- Crypto tests upper boundary of trading range

While stocks have experienced repeated setbacks from events in the Middle East, last week’s push to record highs highlighted the market’s inclination to look past conflict in Iran and focus on potential market tailwinds.

Despite ongoing geopolitical risks, earnings could be a source of bull-friendly breezes. In a recent note on the unfolding reporting season, Morgan Stanley & Co. strategists argue that the market’s earnings recovery remains intact, and that a broadening in price and earnings leadership this year is likely. Some of their observations:

1. Trailing and forward S&P 500 earnings per share (EPS) growth are accelerating (currently +15% and +22%, respectively).

2. Q1 and Q2 S&P 500 EPS estimates are up since the Iran conflict started (+1% and +4%, respectively).

3. Early Q1 results are strong, with the S&P 500 collectively posting an 8.2% EPS surprise and +2% sales surprise.

The strategists also point out that first-quarter EPS estimates have not been lowered into the reporting season, which is contrary to the seasonal trend. When a similar dynamic played out in Q4 (when estimates held steady into the quarter), the S&P 500 printed a strong (+7%) surprise.1

While this week brings a fair number of tech earnings, it’s not overly heavy on software—a group that was a key component to last week’s push back to record highs after being the highest-profile casualty of the AI disruption theme that swept the market in recent months.

New research from Morgan Stanley & Co. analysts suggests industries with high AI exposure are seeing labor productivity, not labor replacement2—a finding that dovetails with observations from a week earlier (noted in this space yesterday) that, rather than displacing software workers and potentially rendering the industry obsolete, AI is shifting work toward senior employees and increasing productivity.3

These analysts cited JFrog (FROG)—a software stock that wasn’t a major contributor to last week’s rally—as “the clearest direct beneficiary of AI-driven software output:”

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

As on Monday, the stock was still roughly 35% below its December record close of $68.98, despite having climbed nearly 30% off of the nine-month low of $34.75 it closed at in February.

Note: JFrog is currently scheduled to release earnings on May 7.

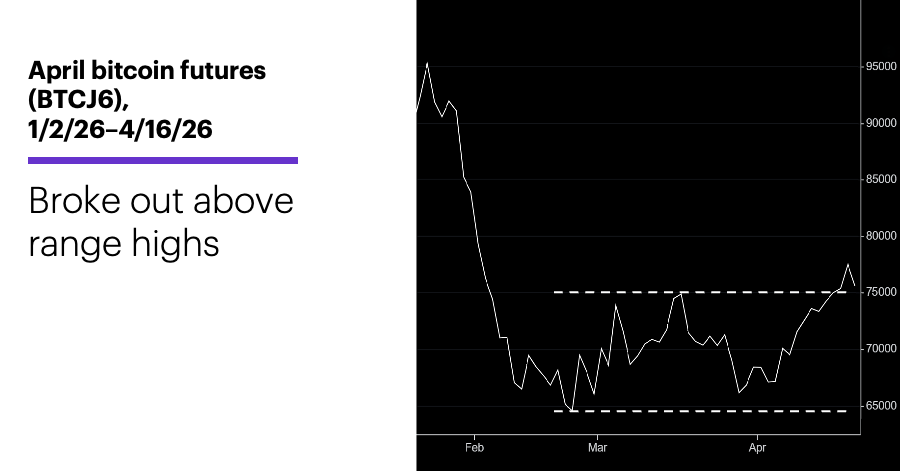

Market Mover Update: Bitcoin and Ethereum futures tracked the stock market in trading to the downside on Monday, but that followed (small) upside breakouts of longstanding trading ranges last week. April Bitcoin futures (BCJ6) traded to their highest level since early February:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Bitcoin is up roughly 15% since March 27, when it swung toward its February lows, confirming the trading range’s lower boundary.

Today’s numbers include (all times ET): Retail Sales (8:30 a.m.), Pending Home Sales (10 a.m.).

Today’s earnings include: Capital One (COF), Quest Diagnostics (DGX), Danaher (DHR), GE Aerospace (GE), Halliburton (HAL), 3M (MMM), Northrop Grumman (NOC), United Airlines (UAL).

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Earnings Season Chartbook. 4/20/26.

2 MorganStanley.com. Industries with high AI exposure are seeing labor productivity from faster output growth, not labor replacement. 4/20/26.

3 MorganStanley.com. More Software and More Developers…Revisited. 4/16/24.