Stocks surge to fresh highs

- Oil slid, stocks jumped after Iran briefly opened Strait of Hormuz

- Tech rally helped propel multiple indexes to record highs

- This week: retail sales, aerospace and defense earnings

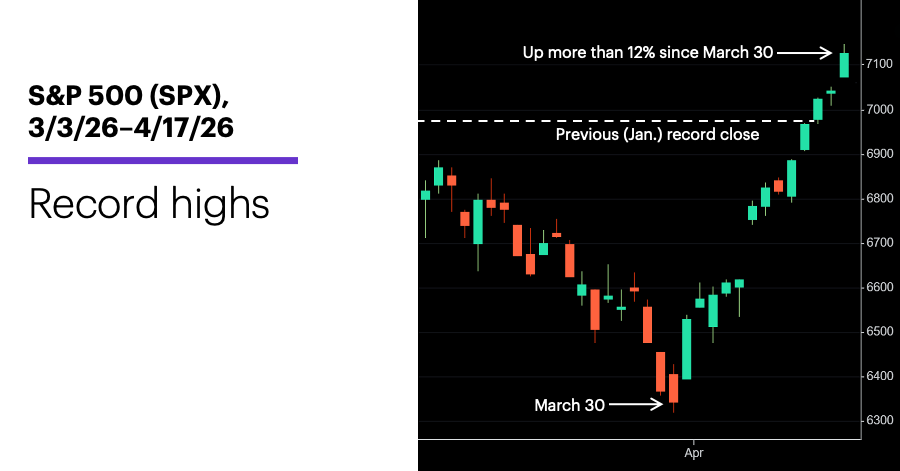

If last week had ended on Thursday, the S&P 500 (SPX) would have marked the start of earnings season with a well-above-average 3.3% return and return to record-high territory.

But a 10%-plus drop in crude oil prices after news early Friday that Iran would open the Strait of Hormuz for the duration of the 10-day Israeli-Lebanon ceasefire (rescinded less than 24 hours later) turned a good week for the SPX into its best one in nearly a year, capping the index’s biggest three-week return since June 2020.

The SPX closed higher every day last week, hit new records on the final three, and climbed more than 1% on Friday:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Indexes erase Iran war losses.

The fine print: The market went into “risk-on” mode last week, with tech, consumer discretionary, and communications services stocks leading the charge, while traders and investors unloaded traditionally-defensive utilities, along with energy.

The number: 3. For the third time since 1957, the SPX rallied more than 3% for three weeks in a row.

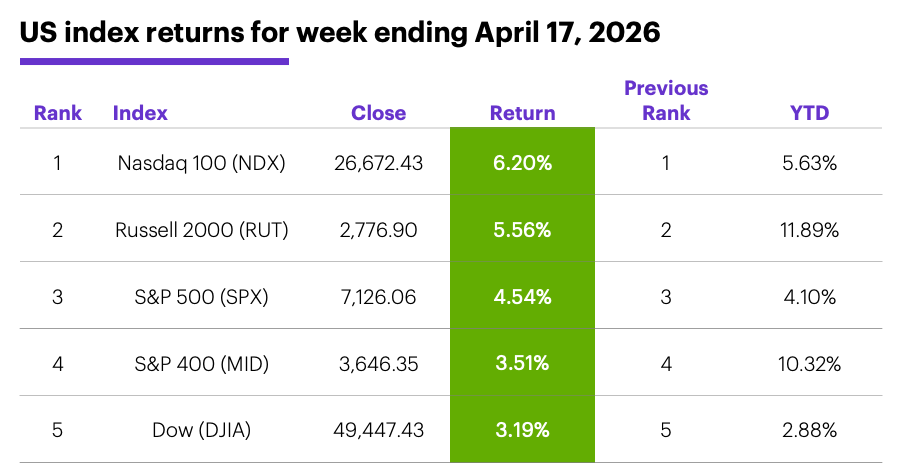

The scorecard: The Nasdaq 100 (NDX) tech index led the US market last week, joining the SPX and the Russell 2000 (RUT) small-cap index in hitting fresh record highs last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were tech (+8.1%), consumer discretionary (+6.6%), and communication services (+6.3%). The weakest sectors were energy (-3.5%), utilities (-1.7%), and materials (-0.4%).

Stock moves: Monday Aeluma (LMU) +43% to $15.35 on Monday, Avanos (AVNS) +70% to $24.63 on Tuesday. BRP (DOO) -35% to $50.93 on Wednesday, Badger Meter (BMI) -24% to $115.54 on Friday.

Yields and the dollar: The 10-year US Treasury yield fell 0.07% to a one-month low of 4.25% last week. The US Dollar Index (DXY) dropped 0.55 to 98.10.

Commodity futures: June WTI crude oil (CLM6) approached $97 last Monday, but closed Friday at $82.59, down $6.99 for the week. June gold (GCM6) climbed $110.50 to $4,879.60. Biggest gains: July Lithium (LTHN6) +11%, July hard red wheat (KWN6) +7.4%,. Biggest declines: June WTI crude oil (CLM6) -7.8%, June heating oil (HOM6) -7.6%.

Crypto: Bitcoin rallied 3.7% to $75,726.21 last week, while Ethereum climbed 2.9% to $2,351.10—the highest levels for both in more than two months.

Coming this week

One Mag-7 name reports this week, but airlines, aerospace, and defense names—including a few on Morgan Stanley & Co.’s Space 60 list—dominate the earnings calendar. Here’s a sample:

●Monday: Alaska Air (ALK), Pentair (PNR), Steel Dynamics (STLD)

●Tuesday: Capital One (COF), Quest Diagnostics (DGX), Danaher (DHR), GE Aerospace (GE), Halliburton (HAL), 3M (MMM), Northrop Grumman (NOC), United Airlines (UAL)

●Wednesday: Boeing (BA), CME Group (CME), GE Vernova (GEV), Lam Research (LRCX), Medpace (MEDP), ServiceNow (NOW), Otis Worldwide (OTIS), Boston Beer Company (SAM), Southwest Airlines (LUV), Teledyne (TDY), Tesla (TSLA), Texas Instruments (TXN), Vertiv (VRT), Whirlpool (WHR)

●Thursday: American Airlines (AAL), American Express (AXP), Dow (DOW), Freeport McMoRan (FCX), Hasbro (HAS), Honeywell (HON), Intel (INTC), Keurig Dr. Pepper (KDP), Lockheed Martin (LMT), Newmont (NEM), Southern Copper (SCCO), Teck Resources (TECK), Union Pacific (UNP), Verisign (VRSN)

●Friday: Apogee (APOG), Norfolk Southern (NSC), Procter & Gamble (PG), SLB (SLB)

US-Iran negotiations are tentatively scheduled to resume this week, while a relatively light economic calendar features retail sales and consumer sentiment data:

●Tuesday: Retail Sales, Business Inventories, Leading Economic Indicators Index, Pending Home Sales

●Thursday: Chicago Fed National Activity Index

●Friday: S&P Global Manufacturing and Services PMI (flash), Consumer Sentiment

Not-so-soft software

If tech was the engine that drove the US stock market rally last week, its fuel came from a surprising source.

Of the nine S&P 500 sectors with positive year-to-date returns as of Friday, tech had the second-smallest gain (4.7%). That tepid performance was in no small part the result of weakness in software stocks, which were down 16% for the year—one of only two tech industry groups that were in the red (IT services was the other).

The softness in software, of course, was the most prominent example of the AI disruption phenomenon—the concern that generative AI will upend a traditional business model and replace many of the jobs within it—that has impacted different areas of the market over the past several months.

As is often the case, though, there’s reason to believe the initial market reaction may have been overdone. Yes, AI accelerates software creation, but according to Morgan Stanley & Co. analysts, that isn’t translating into in a broad-based contraction in developers. The cheaper developments costs resulting from AI is actually driving more software creation, and rather than eliminating developers, it is shifting demand away from entry-level employees to senior engineers who are better equipped to effectively manage the entire production lifecycle.1

This story is far from over, of course. But over the past month, while software was still the tech sector’s second-weakest industry, it posted a net gain of 2.7%. And last week it led the sector with a 14.26% gain.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. More Software and More Developers…Revisited. 4/16/24.