Market up as government shuts down

E*TRADE from Morgan Stanley

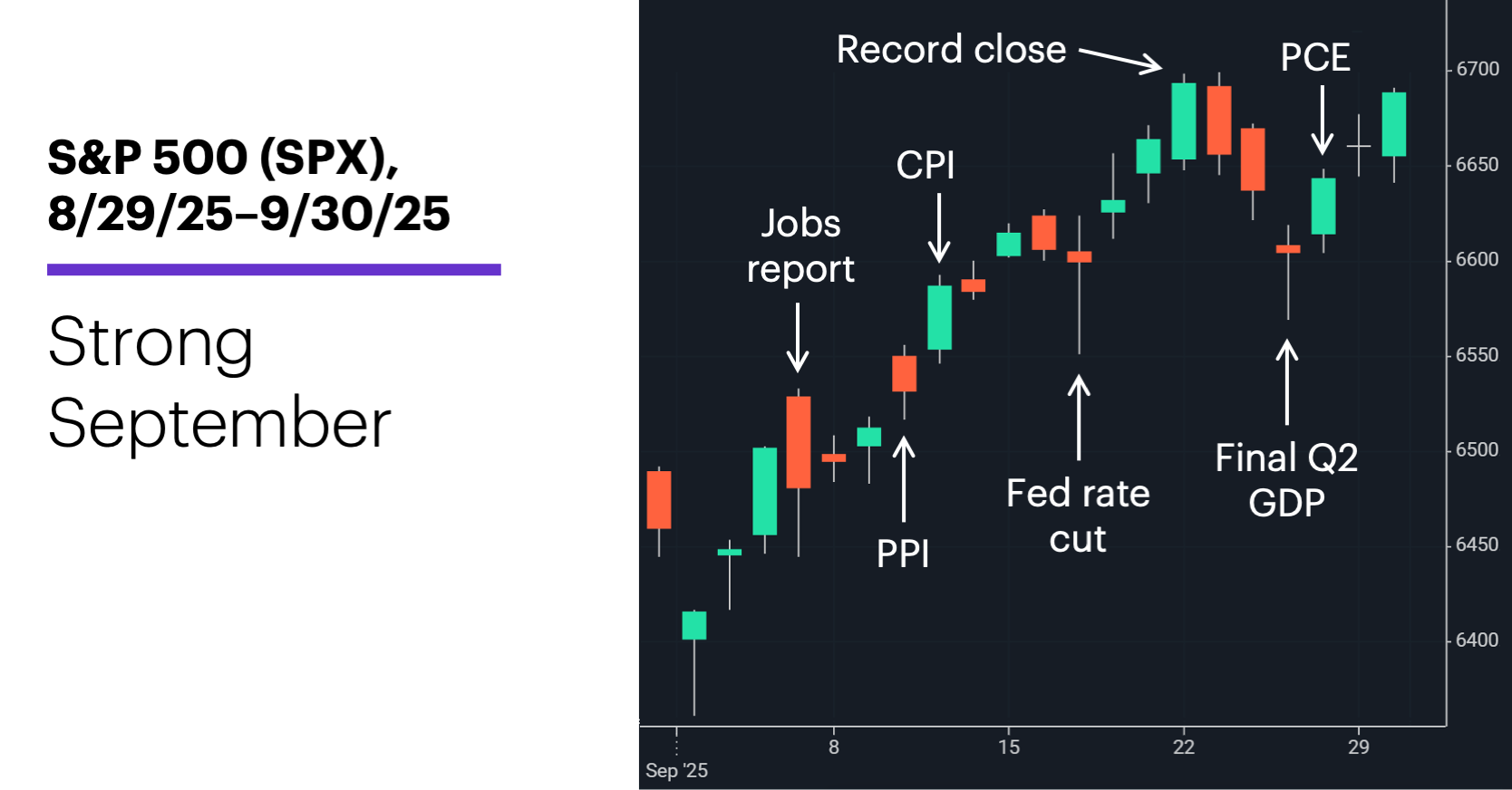

Other than a stumble at the beginning of the month and a minor slowdown toward the end of it, September marked another victory for stock market bulls. It was the S&P 500’s fifth up month in a row, its strongest September since 2010, and capped its sixth-strongest five-month run (+20.1%) since the same year.

Along the way, the Federal Reserve lowered interest rates for the first time this year—what many market participants are hoping will be the first in a series of cuts extending into 2026. The Fed was prompted by soft labor-market data: The monthly jobs report missed estimates for a second month in a row in early September, while inflation data (the CPI, PPI, and PCE Price Index) painted a picture of stickiness rather than reacceleration.

The month ended on an uncertain note, however, as the White House and congressional democrats failed to come to a funding agreement by midnight on September 30, resulting in the first federal government shutdown since December 2018–January 2019.

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.)

There have been 20 federal government shutdowns since 1976, lasting eight days, on average. Morgan Stanley & Co. analysts note the S&P 500’s average gain during shutdowns was 4.4%, suggesting “other macroeconomic factors play a larger role in market outcomes.”1 They add that opportunities could develop in sectors with high exposure to government contracts, such as defense and health care. For example, defense tends to underperform during full shutdowns, which could represent an opportunity given the sector’s longer-term tailwinds.

Unlike the last shutdown, the Bureau of Labor Statistics (BLS) announced it would not release the monthly jobs report on October 3—key data for markets, especially given its heightened importance in determining Fed policy. An extended shutdown could delay or cancel the release of other data.

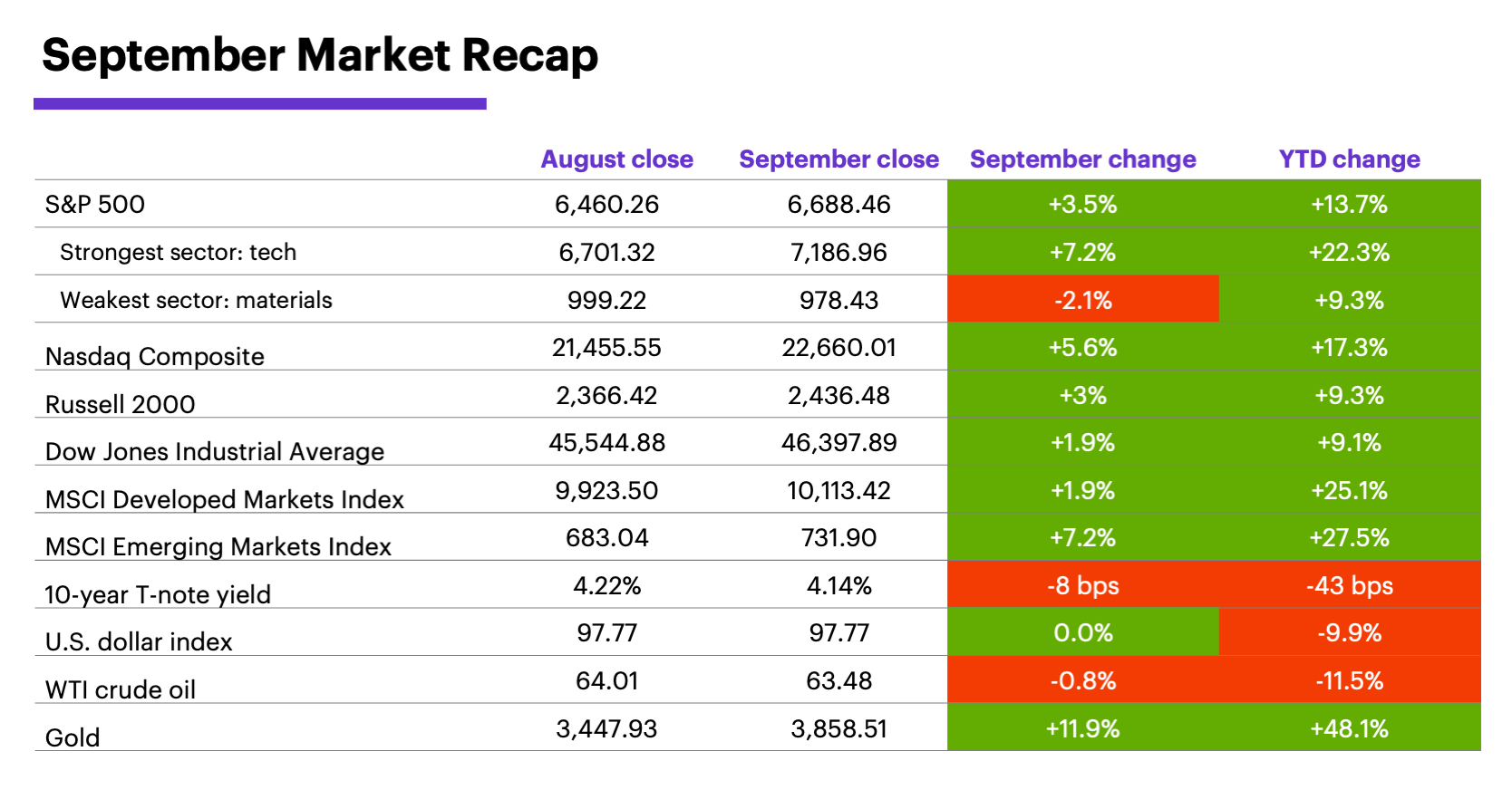

Tech and megacap stocks fueled the September rally. Tech and communication services were the strongest sectors last month, with sizable rallies in stocks like Alphabet (GOOGL) and Oracle (ORCL) contributing to the tech-heavy Nasdaq Composite index’s substantial gain. The small-cap Russell 2000 hit its first record high in nearly three years.

Globally, the S&P 500 outperformed other developed markets, but lagged emerging markets, which enjoyed a standout month. The MSCI developed and emerging market indexes both lead the S&P 500 by a wide margin for the year.

Long-term yields dipped while the US dollar rose. After tumbling in the early part of September, bond yields rebounded to end the month only modestly lower. The US Dollar Index closed September flat after slipping to its lowest level since February 2022 in the middle of the month.

Gold continued to glitter. Gold rallied more than $400 to new record highs above $3,800 in September, ending the month more than 34 percentage points ahead of the S&P 500 for the year.

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment). Past performance is not indicative of future results.

Fed Chair Jerome Powell described lowering rates by 0.25% last month as a “risk-management” cut—reflecting the central bank’s view that a soft labor market posed a greater risk to the economy than inflation.

That means “we shouldn’t assume the Fed is on a pre-set course,” says Ellen Zentner, Chief Economic Strategist for Morgan Stanley Wealth Management. She expects the Fed to continue cutting rates into Q1 2026 before pausing. But she also says the Fed could leave rates unchanged later this month if jobs data is unusually strong and inflation jumps. At the other end of the spectrum, the Fed could cut by 0.5% in the event of a sharper hiring drop-off and increased layoffs.2

Morgan Stanley & Co. strategists think the stock market may shift its focus from labor-market data (and the Fed's response to it) to the idea that the Fed will likely be more tolerant of stickier inflation in 2026. Noting that inflation tends to correlate closely with revenue growth over time, they argue that if the administration’s intention to let run the economy “hot” plays out next year while the Fed cuts rates, revenue and earnings growth could be much stronger than expected.3

Reduced policy uncertainty, strong corporate balance sheets, and the need for investment is a recipe for more IPO and M&A activity.

Insight of the month: More deals on the horizon? As of late September, IPOs were up roughly 68% year-over-year, while M&A was up 35%. Morgan Stanley & Co analysts believe strong corporate balance sheets and—especially—reduced policy uncertainty has made companies more confident about making big decisions. Add the need for investment driven by AI and technology upgrades, “and you get a recipe for more deals.”4

October market history. Despite its high-profile volatility events over the years, October has, historically, been a solid month for US stocks, especially in recent decades. Over the past 30 years, October had the third-highest average S&P 500 return of any month, with gains in 18 years and losses in 12.5

Key October dates (subject to cancellation or delay because of government shutdown): Employment Report (10/3), FOMC minutes (10/8), CPI (10/15), PPI (10/16), retail sales (10/16), Fed interest rate decision (10/29), Q3 GDP, initial estimate (10/30), PCE Price Index (10/31).

1 MorganStanley.com. Do Government Shutdowns Matter to Markets? 9/29/25.

2 MorganStanley.com. Ellen Zentner: Macro Update. 9/18/25.

3 MorganStanley.com. Weekly Warm-up: Will the Fed Catch-Up to the Markets' Demands Fast Enough? 9/22/25.

4 MorganStanley.com. Capital Markets Pick Up as U.S. Policy Settles. 9/24/25.

5 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2024. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.