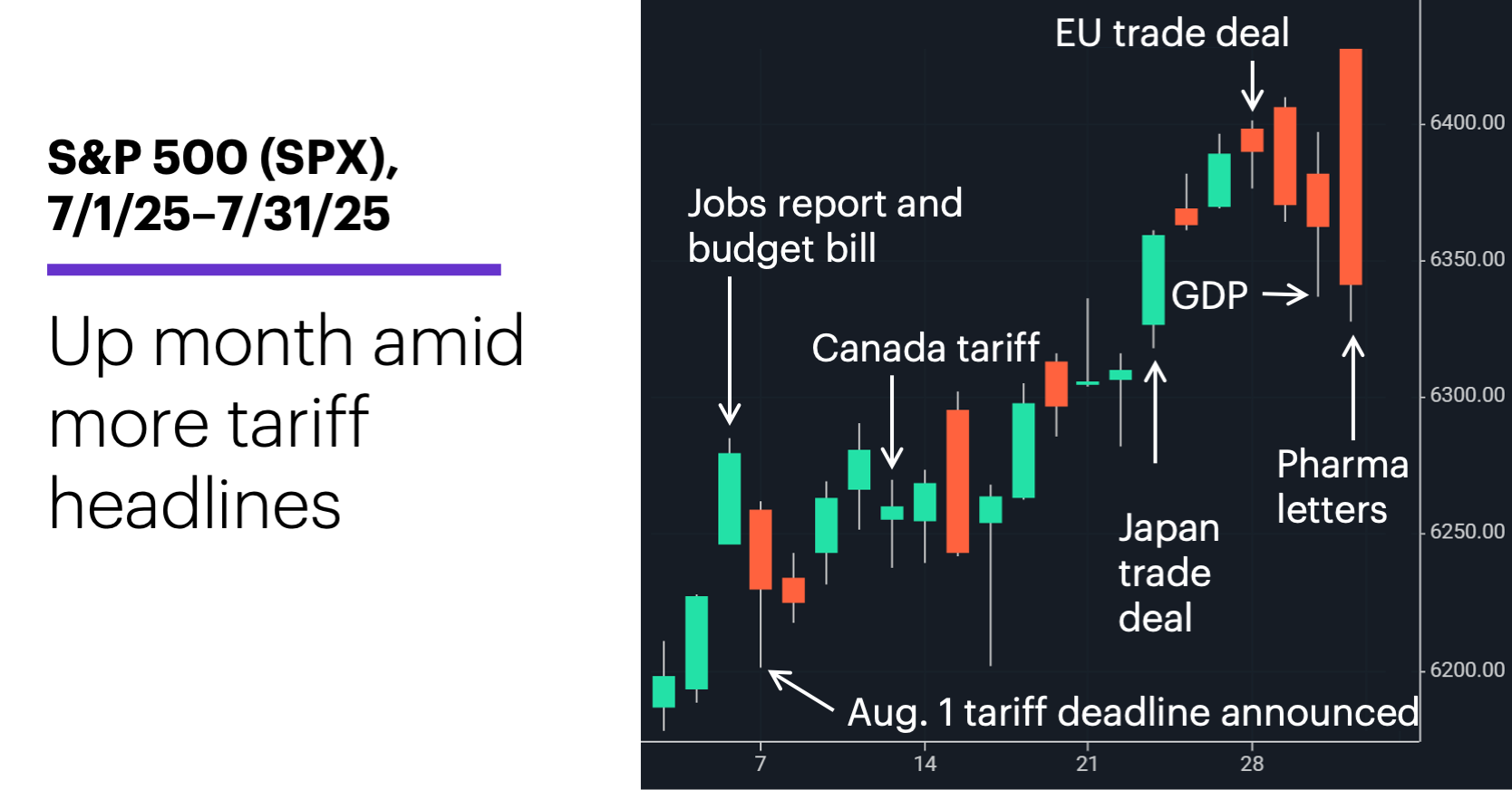

New highs in July as US inks trade deals

E*TRADE from Morgan Stanley

The S&P 500 followed up on its biggest two-month gain since December 2023 with a solid July, the first half of which featured the passage of the budget bill and an assortment of new tariff threats, and the second half highlighted by a few high-profile trade deals, along with a few end-of-month wrinkles in the tariff story:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.)

The White House announced trade agreements with Japan, the European Union, and South Korea before the end of July. While the deals resulted in lower tariffs than those previously proposed to go into effect on August 1, they also resulted in rates that were much higher than pre-Trump administration levels. On July 31, the White House also announced higher tariffs on “transshipped” goods, and issued letters to US pharma companies demanding lower US drug prices.

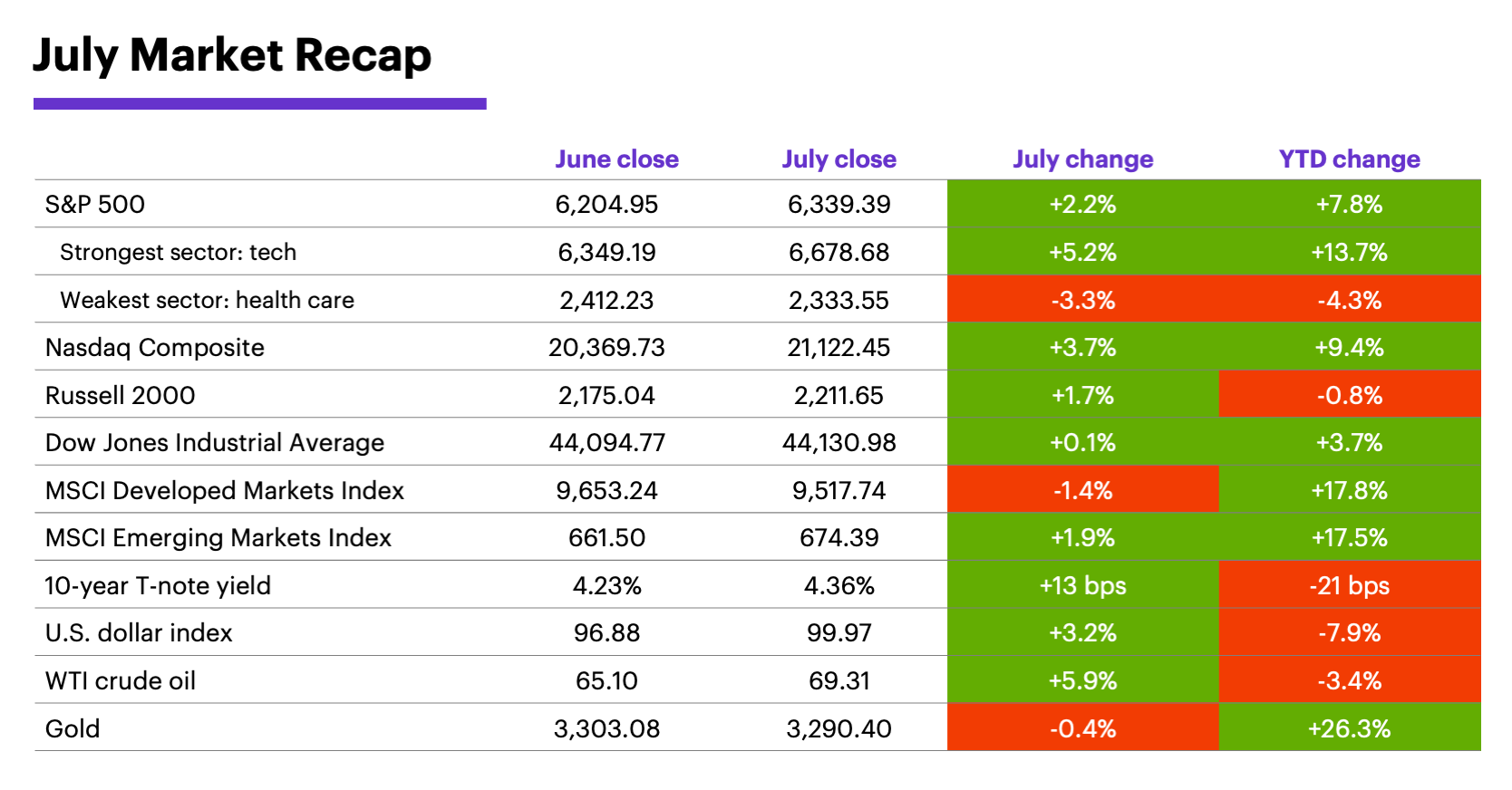

The S&P 500 outperformed both developed and emerging markets last month. Domestically, the tech-heavy Nasdaq Composite led at the index level, and tech was the strongest S&P 500 sector. Consumer staples was the only negative sector.

A solid, but mixed, first phase of earnings season. As of July 25, although the percentage of S&P 500 companies reporting positive earnings surprises was above average, the index was still reporting its lowest year-over-year earnings growth rate (5.8%) since Q1 2024. Also, six sectors had reported year-over-year earnings declines vs. five reporting earnings growth.1

Long-term yields rose modestly in July, while the US dollar posted its first positive month of the year. Bond prices mostly dipped as the benchmark 10-year Treasury yield climbed 13 basis points (0.13%) to 4.36%. The US Dollar Index started July by falling to its lowest level since February 2022, but rebounded to end the month up 3.2% at 99.97.

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment).

The Fed continued to play the waiting game. The Federal Reserve left interest rates unchanged after its July meeting, but Chairman Jerome Powell suggested the Fed was still concerned about tariff-fueled inflation. Although two committee members dissented in favor of cutting rates, Morgan Stanley & Co. economists still expect the next cut to occur in 2026, although they also acknowledge there’s a path for the Fed to cut this year.2 (The weaker-than-expected jobs report on August 1 may have improved the odds of a September rate cut.)

Last month’s headline inflation numbers were moderate, but there were signs of tariff impact in the accelerating prices of many core goods, according to Morgan Stanley & Co. analysts. Their baseline outlook remains one of slow economic growth and firm inflation, with the strongest inflation push from tariffs potentially coming in August. As they note, the data reported last month marked the “end of the beginning, not the beginning of the end.”3

Despite continued challenges, we may be in a dip-buying period for US stock investors, say Morgan Stanley & Co. strategists. While acknowledging risks, including higher long-term interest rates and seasonal weakness, they argue factors such as positive earnings revisions, AI adoption, and a high probability of rate cuts by Q1 2026 support a more bullish outlook. The strategists were leaning toward their bull-case 12-month S&P 500 target of 7,200, describing the environment as one in which dips are meant to be bought.4

Opportunities in new market leaders may emerge as the reality of a “haves and haves-not” economy comes into focus.

But the environment also continues to favor stock picking, notes Morgan Stanley Wealth Management. This is a time for “proactive diligence and stock selection, not for the passivity of the past,” focusing on opportunities in new market leaders as the reality of a “haves and haves-not” economy emerges. The strategists suggest adding stocks with earnings and cash-flow upside-surprise potential in select tech hardware and services names, industrials, financials, energy, and parts of health care that are “policy beneficiaries amid higher structural volatility and real rates, and a weak US dollar.”5

Insight of the month: The currency factor. A Morgan Stanley & Co. “Quant Matters” report explains that, in an environment characterized by rising currency volatility and elevated macroeconomic uncertainty, companies with significant currency exposure are more vulnerable than those with lower exposure. Specifically, companies with low currency-risk exposure tend to be more insulated from “global macro shocks.”6 Their report includes US, European, and Japanese stocks with the lowest currency exposure.

August market history. Morgan Stanley & Co. notes that seasonal softness has, historically, tended to emerge around this time of the year.7 August has never been a consistently stronger-than-average month for US stocks, and it’s been weaker than average over the past 34 years. Since 1991, August was a positive month less often (19 of 34 years) than any other month but September. The S&P 500’s 0.4% median August return was the third-lowest of all months during that period.8

Important dates: Employment Report (8/1), ISM Services Index (8/5), CPI (8/12), PPI (8/14), retail sales (8/15), housing starts (8/19), FOMC minutes (8/20), Q2 GDP, second estimate (8/28), PCE Price Index (8/29).

1 FactSet. Earnings Insight. S&P 500 Earnings Season Update: July 25, 2025.

2 MorganStanley.com. Paths to September Rate Cuts. 7/28/25.

3 MorganStanley.com. US outlook update: Still weighted to the downside. 7/16/25.

4,7 MorganStanley.com. Weekly Warm-up: No Ordinary Cycle. 7/28/25.

5 MorganStanley.com. The GIC Weekly: Wash, Rinse, Repeat? 7/28/25.

6 MorganStanley.com. Quant Matters—Introducing Low FX Sensitivity Factor Amid USD Weakness. 7/11/25.

8 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2024. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.