Market sidesteps April showers

E*TRADE from Morgan Stanley

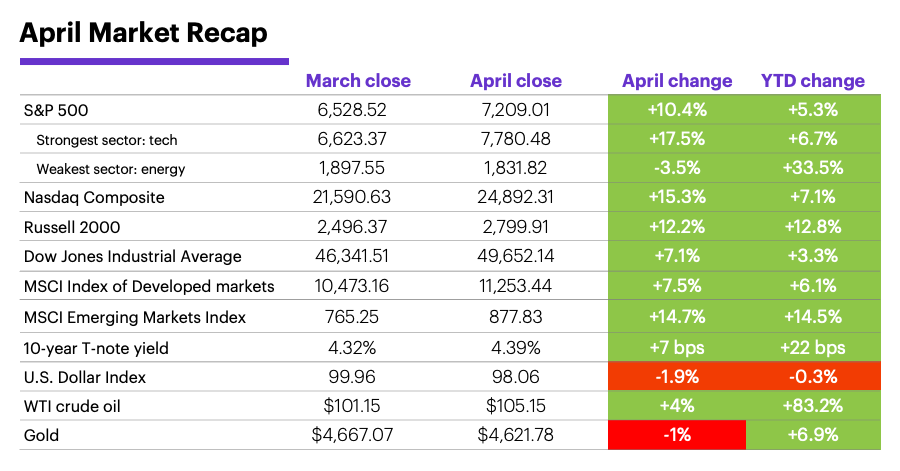

An unresolved conflict in the Middle East, the highest oil prices in nearly four years, and slim odds for lower interest rates in the near future failed to halt the US stock market’s return to record highs in April, as investors chose to focus on earnings and potential market tailwinds—especially AI-driven spending and productivity gains.

The S&P 500 (SPX) logged its biggest monthly return since November 2020, returning to record territory in the process. The market barely paused in the final days of April as US crude oil prices jumped back above $100, ending the month at an all-time high:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.)

Despite the renewed oil surge, the futures market continued to imply lower prices later this year. At the end of April, US crude oil futures for delivery in December were trading around $80, which was 24% below the price of oil for delivery in June ($105).

Tech was—by far—the strongest S&P 500 sector last month, energy was the weakest. The market’s risk-on mood was reflected in the tech sector’s 17.5% rally, led by gains in the semiconductor space. Energy stocks retreated even though oil prices ended the month near their highest level since June 2022. Health care was the only other sector to lose ground in April.

The US stock market lagged emerging markets, but led developed markets. The S&P 500 outperformed the MSCE Developed Markets Index last month, but trailed the MSCI Emerging Markets Index by slightly wider margin. Within the emerging equity space, Morgan Stanley Wealth Management strategists continued to favor Latin America over Asia.1

Bond prices were little changed as yields moved mostly sideways. The 10-year Treasury yield climbed modestly, while the US Dollar Index lost ground, ending April in negative territory for the year:

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment). Past performance is not indicative of future results.

Last month’s “stunning” upside reversal may have two sides, according to Morgan Stanley Wealth Management strategists. While the move was arguably a constructive a reminder of the market’s ability look past potentially transitory events, record index levels and “unforgiving” valuations may have also raised the bar for further gains. But the strategists add that some areas of the market (e.g., software, health care, consumer sectors, and financials) are “on sale,” while others—most notably, semiconductors—may be overbought. “Meeting and beating” earnings forecasts remains critical, they note.2

AI productivity re-emerged as a dominant market theme. Despite continued geopolitical uncertainty in the Middle East and a lingering “AI disruption” hangover, the market appeared to lean into AI’s potential tailwinds. In January, Morgan Stanley & Co. laid out 10 thematic predictions for the year. Nearly three months later, they highlighted the key roles some of the them are playing in the markets, especially the explosion in AI large language model (LLM) capabilities and the resulting demand for computing resources.3

Tech earnings appeared to support the AI story. The mostly better-than-expected earnings reports from Alphabet, Amazon, Meta, Microsoft, and Apple highlighted the massive resources the key “AI hyperscalers” continue to commit to AI datacenter buildout. Aso, the intense demand for computer memory and storage has played out in strong rallies in stocks such as Sandisk (SNDK), Micron (MU), Seagate Technology (STX), and Western Digital (WDC).

There are signs that AI is driving higher productivity—but not necessarily at the expense of jobs. Productivity is rising faster in industries Morgan Stanley & Co. defines as “high-AI exposure” relative to those classified as median- or low-AI industries. Thie enhanced productivity reflected faster output growth and “capital deepening,” rather than job displacement.4

As consumers take health into their own hands, home diagnostics is quickly expanding into a multi-billion-dollar US market.

Insight of the month: The Rise of Self-Care Health Care. Morgan Stanley & Co. analysts say consumer-driven diagnostics is rapidly expanding into a roughly $4 billion US market, supported by lab partnerships and the growing popularity of voluntary testing and wearable devices. This trend could drive $200-$800 billion in gross health care savings by 2050 as consumers “take health into their own hands.”5

The Fed delivered a surprise in late April, but it wasn’t a rate cut. Solid economic growth and sticky inflation—with continued upside risk because of geopolitical uncertainty—compelled the Fed to leave interest rates unchanged in late April, as expected. But Jerome Powell announced he intended to serve as a Fed Governor after his term as Chairman ends on May 15—a decision, he said, to help protect the Fed’s independence.

A new Fed chief probably won’t alter the Fed’s “wait-and-see” posture. According to Ellen Zentner, Chief Economic Strategist for Morgan Stanley Wealth Management, a changing of the guard at the top of the Fed isn’t going to change the central bank’s calculus. Aside from the fact that incoming Chair Kevin Warsh hasn’t indicated he’ll push for aggressive easing, any policy shift would require a consensus from the FOMC—and its most recent announcement highlighted the wide range of opinions on the committee. Morgan Stanley & Co. economists expect the Fed to cut rates in January and March 2027.6

May market history. May’s reputation as a month for investors to “go away” has been greatly exaggerated, especially over the past three or so decades. While May was a positive month for the S&P 500 in just 53% of years between 1957 and 1990, since then it’s been up month 71% of the time—just as often as November and December, and second only to April.7

Important May dates: Employment Report (5/8), CPI (5/11), PPI (5/12), Retail Sales (5/14), FOMC minutes (5/20), US markets closed for Memorial Day (5/25), PCE Price Index (5/28), GDP (5/30).

1,2 MorganStanley.com. The GIC Weekly: “Meeting and Beating” Versus Revisions. 4/27/26.

3 MorganStanley.com. Revisiting Our 10 Thematic Predictions. 4/6/26.

4 MorganStanley.com. Industries with high AI exposure are seeing labor productivity from faster output growth, not labor replacement. 4/20/26.

5 MorganStanley.com. Testing Longevity. 4/20/26.

6 MorganStanley.com.April FOMC Reaction Later Cuts and a Longer Hold. 4/30/26.

7 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2025. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.