Stocks close out Q1

E*TRADE from Morgan Stanley

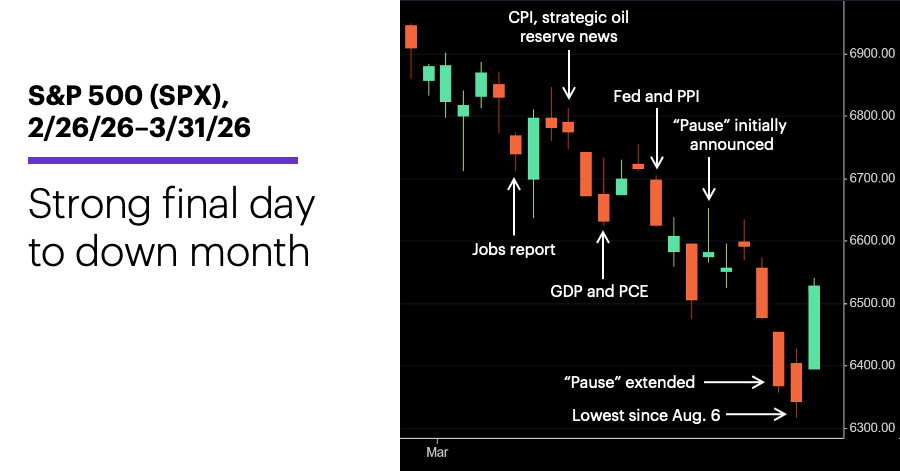

The first quarter of 2026 ended with US stocks attempting to rebound from their deepest downturn in a year, as geopolitics and oil prices dominated market sentiment and sent the S&P 500 (SPX) to a second-straight down month.

February’s AI disruption theme was swept aside by the US and Israeli military strikes on Iran, which were followed by the biggest one-month increase in crude oil prices in more than four decades—fueling inflation concerns and sending most major US stock indexes into corrections (10% or more below a previous close).

The SPX didn’t quite cross the correction threshold in March, but it did fall to its lowest level since last August. The index also registered its biggest monthly decline (-5.1%) since May 2025, despite a large rally on the final day of the month amid new reports that President Trump was seeking to end the war. After the close, the president said he expected US military forces will leave Iran in two or three weeks, and the White House announced he would deliver an address on the situation at 9 p.m. ET on April 1:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.)

Despite conflicting reports of progress on US-Iran negotiations, the March decline was fairly orderly. The markets rode a rollercoaster of positive and negative headlines about the war and energy markets throughout the month, including the release of strategic oil reserves, warnings of increased military action, and a “pause” on airstrikes of Iranian infrastructure. Meanwhile, weaker-than-expected economic data (monthly jobs report and GDP) and mostly higher-than-expected inflation readings (PPI and PCE Price Index) may have added to negative sentiment, but they didn’t result in exaggerated “panic” selling.

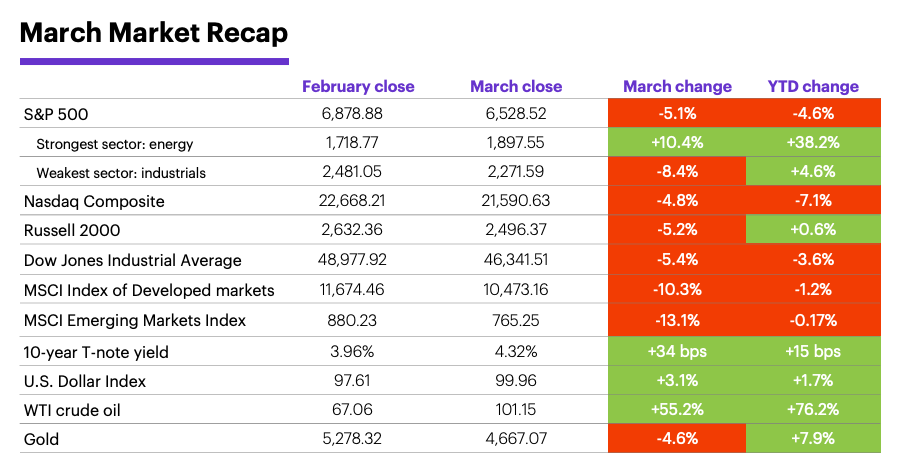

Energy was the only positive S&P 500 sector last month, while industrials was the weakest. The jump in US petroleum prices—spot crude oil’s 55.2% March rally was the market’s second-biggest monthly increase of the past 40 years—lifted energy stocks.

The US stock market fell less than most of its global counterparts. In a reversal of the prevailing trend, the MSCI developed and emerging markets indexes both declined more than twice as much as the S&P 500 in March on a percentage basis. In part, energy independence helped buffer US stocks from concerns about the oil price surge.

Bonds fell as yields jumped along with the dollar. Despite retreating in the final two days of March, the benchmark 10-year Treasury yield posted its biggest one-month increase since last September, while the US Dollar Index hit its highest level since last May late in the month:

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment). Past performance is not indicative of future results.

Oil prices may remain elevated even if the war ends soon. Morgan Stanley & Co. strategists think energy market disruption has moved “beyond logistics to production,” implying higher-for-longer energy prices even if hostilities de-escalate. They see the $80-$90 range as a likely 2026 range for global Brent crude oil in a de-escalation scenario, with continued constraints likely driving prices near $100-$110 for at least two to three months.1 (At the end of March, US WTI crude oil was trading roughly $2.70 below the Brent price.)

But the oil spike won’t necessarily derail the business cycle, according to Morgan Stanley & Co. analysts. Unlike past oil shocks that triggered economic contractions or recessions, earnings growth is currently accelerating and positive (instead of decelerating and negative), and this oil surge is actually much smaller in year-over-year terms. Assuming a recession is avoided, the analysts still see 7,800 as an achievable S&P 500 price target this year, although it could take slightly longer to reach if oil prices “remain elevated/around current levels in the near-term.”2 They also note rising interest rates and a hawkish pivot by central banks—including the Fed—poses a potential risk to this outlook.3

The Fed left interest rates unchanged last month, citing the uncertain economic impact of high oil prices. However, in a speech toward the end of the month, Fed Chair Jerome Powell pointed out the Fed’s inclination would be to “look through” this type of supply shock (implying no need to hike rates).

Morgan Stanley & Co. economists still expect the Fed to cut rates in 2026. While they updated their 2026 outlook in light of the Iran war to reflect less growth, more inflation, and higher unemployment, they also believe recent concerns about possible rate hikes are unfounded. They see the Fed cutting rates twice later this year, in September and December.4

The market is unprepared for the huge jump in AI large language model (LLM) capabilities over the next few months.

Insight of the month: The Return of AI. Geopolitics may have temporarily pushed AI out of the spotlight, but the theme is alive and well—and it could be entering a key phase. One of the messages coming out of Morgan Stanley’s annual Technology, Media and Telecom (TMT) conference last month: The market is unprepared for the “non-linear increase in AI large language model (LLM) capabilities.”5 To Morgan Stanley & Co. analysts, that means the companies positioned to service AI infrastructure “bottlenecks”—e.g., providing critical power, labor, and AI hardware—will continue to benefit.6

Persistently high oil prices could have a real impact on consumer spending. Morgan Stanley & Co. analysts lowered their consumption forecasts by 30 basis points because of the oil shock, noting that “higher prices and slower labor income growth mean further pressures on low- and middle-income consumers.”

April market history. Since 1957, April has been a positive month for the S&P 500 71% of the time (40 out of 69 years)—only November and December have been up months as often. Over the past three decades April had a positive return 73% of the time (second place) and median return of 1.3% (fifth place).7

Important April dates: Employment Report (4/3), Markets closed for Good Friday (4/3), PCE Price Index (4/9), CPI (4/10), PPI (4/14), retail sales (4/21), Fed interest rate decision (4/29), GDP (4/30).

1 MorganStanley.com. Energy Shocks in the Economy & Markets II. 3/24/26.

2 MorganStanley.com. Weekly Warm-up: Iran Impact, Rates and Investor Feedback. 3/30/26.

3 MorganStanley.com. Weekly Warm-up: Taking Stock on Valuation, Iran/Oil and Central Banks. 3/24/26.

4 MorganStanley.com. Fears of Rate Hikes Overdone. 3/20/26.

5 MorganStanley.com. Our 10 Thematic Predictions + Our TMT Conference: Implications and Key Debate. 3/10/26.

6 MorganStanley.com. Powering AI in the US: Our Latest Thoughts. 3/10/26.

7 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2025. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.