Markets look for geopolitical clarity

- S&P 500 falls for fifth week, other indexes enter corrections

- Oil ends week near $100, bond yields jump, gold steadies

- This week: jobs data, retail sales, markets closed Good Friday

With the end of March approaching, a still-murky geopolitical picture and elevated oil prices were weighing on financial markets as the Iran war extended to a fourth week.

Last Monday crude oil prices tumbled 10% and the S&P 500 (SPX) rallied more than 1% after the White House announced it would postpone attacks on Iranian energy facilities. But oil rebounded—and stocks sagged—the rest of week amid conflicting messages about US-Iran peace negotiations and warnings of future strikes.

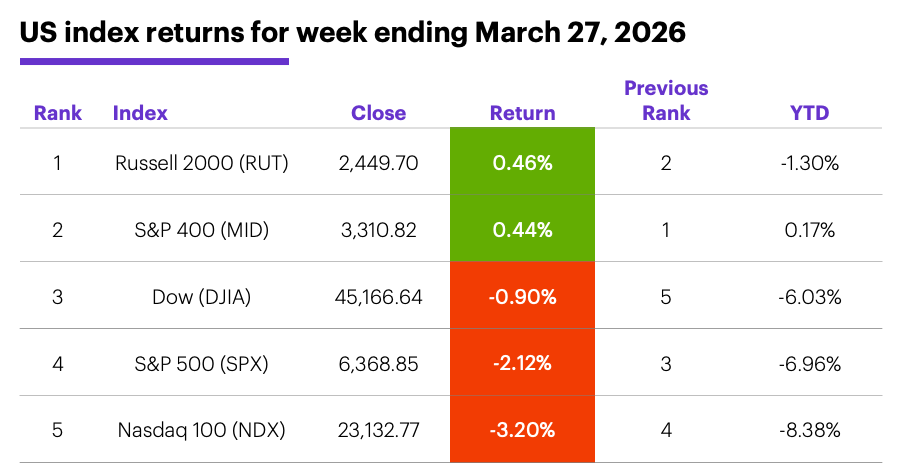

The Nasdaq 100 (NDX) tech index, Nasdaq Composite (COMP), and Dow Jones Industrial Average (DJIA) joined the Russell 2000 (RUT) small-cap index in correction territory last week by closing at least 10% below a previous close. The SPX didn’t cross that threshold, but it still ended last week at fresh lows for the year—despite the White House’s late-Thursday announcement that it would extend the airstrike pause until April 6:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: S&P 500 posts fifth-straight down week.

The fine print: Last week’s decline was in line with the SPX’s historical tendencies after four-week losing streaks, as well as after back-to-back weeks of lower SPX and Cboe Volatility Index (VIX) closes. The SPX also closed lower more often than higher one week after five-consecutive down weeks—15 out of 27 times since 1957.1

The number(s): $80-$90, the likely price range Morgan Stanley & Co. strategists believe Brent (global) crude oil will trade in the remainder of the year. That forecast reflects a near-term de-escalation of hostilities in the Middle East that results in normal oil tanker traffic through the Strait of Hormuz.2

The scorecard: Tech and large caps took the biggest hits last week, while small- and mid-caps posted small gains:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were energy (+6.1%), materials (+4.1%), and utilities (+2.7%). The weakest sectors were communication services (-7.1%), tech (-3.5%), and financials (-2.3%).

Stock moves: Kodiak Sciences (KOD) +75% to $39.76 on Thursday, Argan (AGX) +38% to $566.62 on Friday. Maze Therapeutics (MAZE) -35% to $31.73 on Wednesday, MillerKnoll (MLKN) -22% to $15.03 on Thursday.

Yields and the dollar: The 10-year US Treasury yield climbed 0.04% to 4.43% last week. The US Dollar Index (DXY) rallied 0.50 to 100.15.

Commodity futures: May WTI crude oil (CLK6) dropped 10% last Monday, but rebounded to end the week up $1.41 at $99.64. In another soft week for metals, June gold (GCM6) closed Friday at $4,524.30, down $85.30 for the week. Biggest gains: May orange juice (OJK6) +9.3%, May red wheat (KWK6) +4.4%. Biggest declines: July platinum (PLN6) -5.4%, May oats (ZOK6) -4.6%.

Crypto: Bitcoin ended the week down 3.5% at $66,319.70. Ethereum fell 4% to $1,992.69.

Coming this week

This week’s economic calendar revolves around labor-market data, but February’s shutdown-delayed retail sales data should get a fair amount of attention. The monthly jobs report will be released on Friday, even though markets will be closed for Good Friday:

●Tuesday: S&P Case-Shiller Home Price Index, FHFA House Price Index, Chicago PMI, Job Openings and Labor Turnover Survey (JOLTS), Consumer Confidence

●Wednesday: ADP Private Employment, Retail Sales (delayed, for February), S&P Global Manufacturing PMI, ISM Manufacturing Index, Business Inventories (delayed, for January)

●Thursday: job cuts, balance of trade

●Friday: Good Friday (US stock exchanges closed), Employment Report, S&P Global Services PMI, ISM Services Index

This week’s earnings include:

●Monday: Progress Software (PRGS), USA Rare Earth (USAR)

●Tuesday: FactSet (FDS), McCormick & Company (MKC), Nike (NKE), PVH (PVH), RH (RH), TD Synnex (SNX), Unifirst (UNF)

●Wednesday: Conagra (CAG), Cal-Maine Foods (CALM), Lamb Weston (LW), MSC Industrial Direct (MSM)

●Thursday: Acuity (AYI), nCino (NCNO)

Market performance after negative Q1s

Although one concrete positive development out of the Middle East could change things, barring a 7.5% rally over the next two days, the SPX will end the first quarter in negative territory for the year. If the quarter had ended on Friday, the 7% decline would have been the eighth-biggest Q1 loss of the past seven decades.3

First-quarter declines aren’t common, but they’re far from rare. The SPX has had a negative Q1 return 27 other times since 1957, ranging from -0.06% (2002) to -20% (2020)—most recently in 2025, when it closed the quarter down 4.6% but rallied 22% over the next nine months to end the year with a better-than-average 16.4% gain.

More often than not, though, negative Q1s have been part of weaker-than-average years for the SPX. After a negative Q1, the index posted a net gain for the remainder of the year (April-December) in 14 of 27 cases, but its full-year return was negative in 15 cases.

In years with positive Q1s, the SPX’s average April-December return was 8.8% and its average full-year return was 16.4%. But in years with negative Q1s, the average April-December return was 3.3% and the average full-year return was -3%.

This year’s x-factor, though, may be its geopolitical component. March’s pullback unfolded against the backdrop of an unexpected war with Iran and a 50% increase in crude oil prices. A clear resolution to the conflict—and one that occurs sooner rather than later—would arguably have the potential to clear the path to potential upside the remainder of the year.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 All figures reflect S&P 500 (SPX) weekly closing prices, 1957-2026. Pattern refers to five-straight down weeks preceded by an up week. Supporting document available upon request.

2 MorganStanley.com. Energy Shocks in the Economy & Markets II. 3/24/26.

3 All figures reflect S&P 500 (SPX) monthly closing prices, 1957-2026. Supporting document available upon request.