Pivot softens tech pullback

- Dow hits milestone, mid-cap stocks surge

- Software and megacaps weigh on tech

- This week: jobs, inflation (CPI), retail sales

Another bout of tech volatility made for an eventful first week of February, as concerns about AI disruption in the software industry dragged down the tech sector.

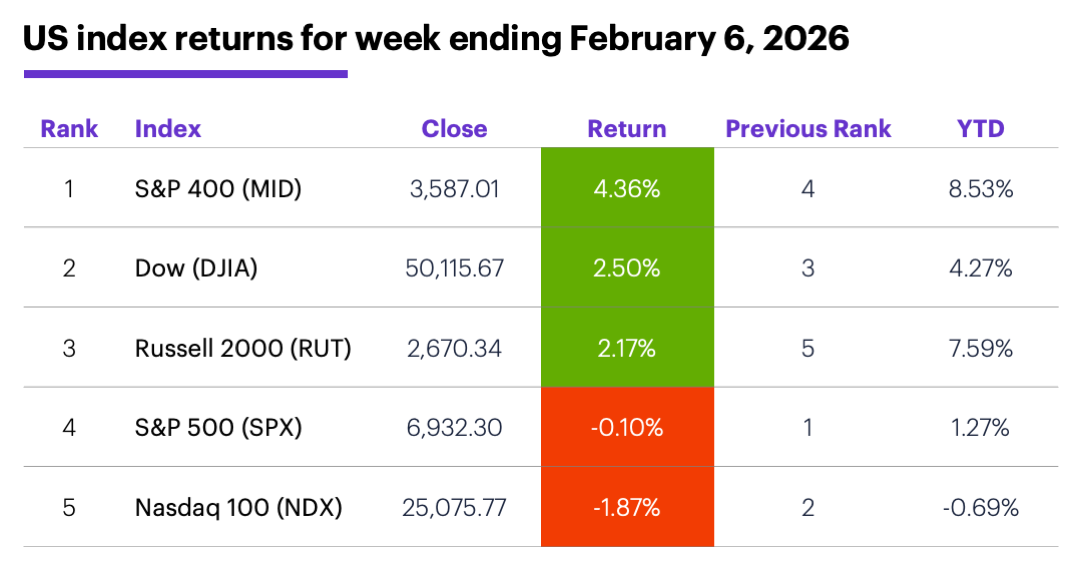

But even though the S&P 500 (SPX) and Nasdaq 100 (NDX) tech index slipped for the week, both indexes recouped the bulk of their losses with massive Friday rallies. And while the Dow made headlines with its new high, mid-cap stocks were the biggest gainers last week.

After closing in negative territory for the year last Thursday as the software sell-off accelerated, the S&P 500 (SPX) posted its biggest up day since last May on Friday. Although it wasn’t quite enough to erase the week’s loss, it did get the index back into the black for the year:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: AI concerns trip up tech sector.

The fine print: While software stocks were the biggest drag on the tech sector last week, megacap AI leaders Microsoft (MSFT) and Amazon (AMZN) both sold off after releasing earnings, partly because of concerns about the magnitude of their AI spending.

The move: AMZN’s 12% sell-off—its biggest down week in a decade—played a big role in the consumer discretionary sector’s weakness. However, Morgan Stanley & Co. analysts reiterated their Overweight rating on the stock on Friday.1

The number: 50,000. The Dow closed above this long-anticipated threshold for the first time on Friday.

The scorecard: The Russell 2000 (RUT) small-cap index reasserted its relative strength last week—but not as much as the S&P 400 (MID) mid-cap index did. The Nasdaq 100 (NDX) tech index ended the week in negative territory for the year:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were consumer staples (+6%), industrials (+4.7%), and energy (+4.3%). The weakest sectors were consumer discretionary (-4.6%), communication services (-4.4%), and information technology (-1.4%).

Stock moves: Silicon Laboratories (SLAB) +49% to $203.41 and Enphase Energy (ENPH) +39% to $51.67, both on Wednesday. Ralliant (RAL) -32% to $38.39 and Fluence Energy (FLNC) -35% to $18.95, both on Thursday.

Yields and the dollar: The 10-year US Treasury yield fell 0.06% to 4.2% last week. The US Dollar Index (DXY) climbed 0.63 to 97.62.

Futures: April gold (GCG6) fell to a one-month intraday low last Monday, but rebounded to end the week up $234.70 at $4,979.80. March silver (SIH6) closed the week down $1.63 at $76.90. March WTI crude oil (CLH6) pulled back $1.66 to $63.55. Biggest gains: March nonfat dry milk (DCH6) +10.8%, April gold (GCJ6) +5%. Biggest declines: March orange juice (OJH6) -24.8%, February ether (ETHG6) -23.2%.

Coming this week

This week’s economic calendar features the monthly jobs report (delayed from last week), CPI, and retail sales (delayed December data):

●Monday: NY Fed Consumer Inflation Expectations

●Tuesday: NFIB Business Optimism Index, Retail Sales, Employment Cost Index, Import and Export Prices

●Wednesday: Employment Report

●Thursday: Existing Home Sales

●Friday: Consumer Price Index (CPI)

This week’s earnings include:

●Monday: AstraZeneca (AZN), BP (BP), McDonald's (MCD), Medpace (MEDP), Monday.com (MNDY), ON Semiconductor (ON), Southern Copper (SCCO)

●Tuesday: Astera Labs (ALAB), Cisco (CSCO), CVS (CVS), Datadog (DDOG), Quest Diagnostics (DGX), Ford (F), Coca Cola (KO), Lattice Semiconductor (LSCC), Lyft (LYFT), Marriott International (MAR), Mattel (MAT), Spotify (SPOT), Teradata (TDC)

●Wednesday: Airbnb (ABNB), Albemarle (ALB), AppLovin (APP), GoDaddy (GDDY), Humana (HUM), Kraft Heinz (KHC), Shopify (SHOP), T-Mobile (TMUS)

●Thursday: Arista Networks (ANET), Baxter International (BAX), Check Point Software (CHKP), Coinbase (COIN), Hyatt Hotels (H), Public Storage (PSA), Wynn Resorts (WYNN)

●Friday: Advance Auto Parts (AAP), Moderna (MRNA), Tower Semiconductor (TSEM)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Other slow starts to February

Friday’s stock surge may have felt like a momentum shift—and it could be—but based on nearly seven decades of history, it may not be the final word on February’s market performance.

First, a non-seasonal perspective on last week’s SPX move. The SPX fell more than 2% intraweek, hit its lowest low in more than six weeks, and rebounded to close in the upper half of the week’s range. It’s done that 63 other times since 1957, and three weeks later it was higher in 43 cases (67% of the time).

Now, a seasonal perspective. Before last week, the SPX posted a net loss for the first five trading days of February in 26 of the past 69 years. It closed the month with a positive return in only four of those cases (15%). By comparison, after the 43 times the SPX climbed the first five days of February, it ended the month with a gain 32 times (70%).2

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Investing Behind Strength; Maintain OW. 2/6/26.

2 All figures reflect S&P 500 (SPX) daily closing prices, 1957-2025. Supporting document available upon request.