Inflection point for health care?

- Health care was second-strongest sector last month

- Sector still in negative territory for year

- Additional tailwinds for biotech/pharma?

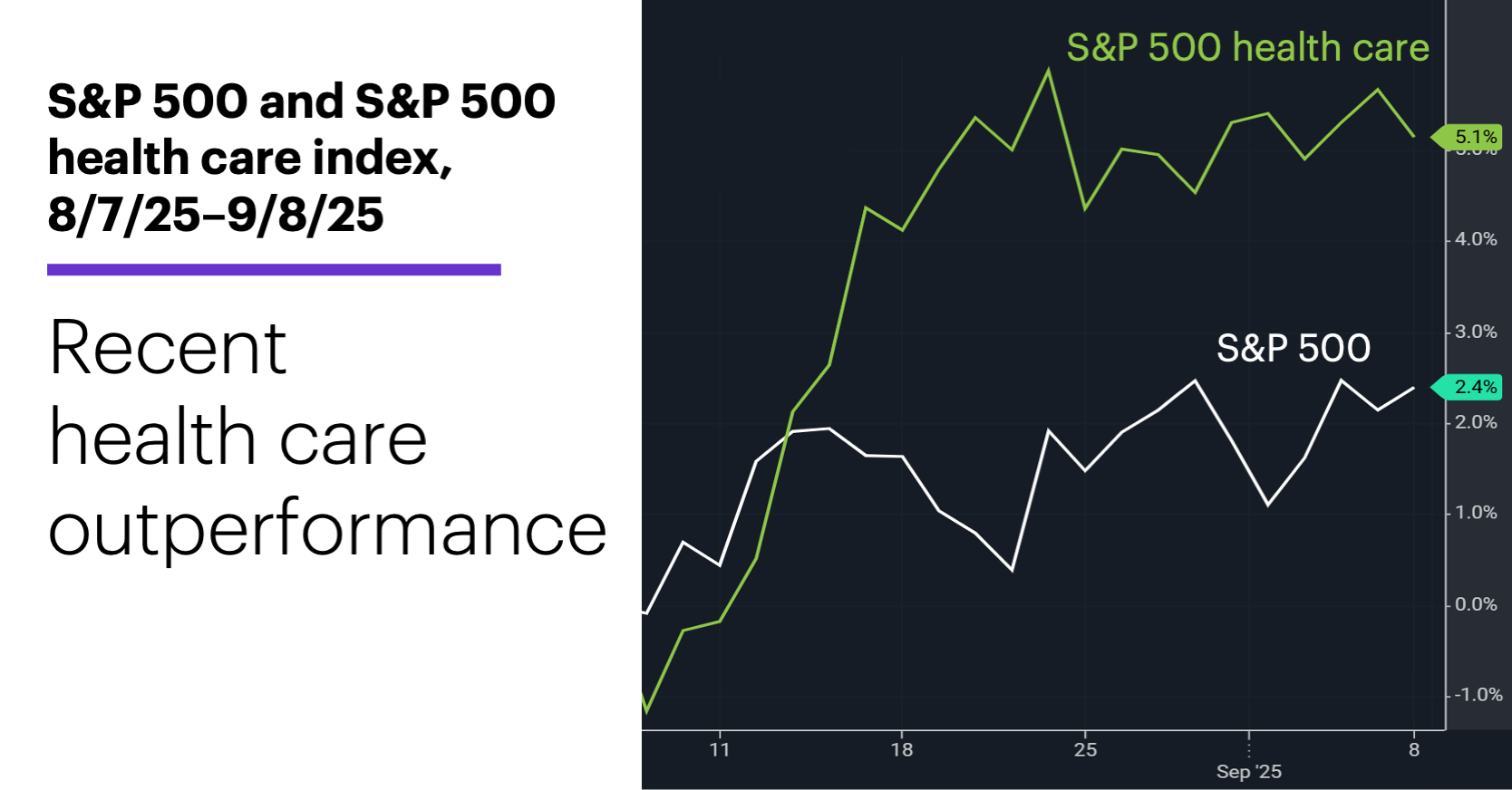

It’s safe to say few people saw one recent under-the-radar market development coming. Since early August, the health care sector has gained roughly twice as much as the S&P 500 (SPX):

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index.)

Of course, this performance stands in stark contrast to health care’s longer-term performance. It was the weakest sector last year and is still the weakest so far in 2025—the only one that, as of Monday, was still in the red for the year.

Not everyone was ignoring the sector, though. Daniel Skelly, Head of Morgan Stanley's Wealth Management Market Research & Strategy Team, noted last month the potential attractiveness of the health care sector, given its valuation was near its historical lows and it had its lowest weighting in the S&P 500 since 1994.

Morgan Stanley & Co strategists sounded a related theme on Monday, highlighting large-cap health care as their preferred pick among defensive sectors.1 In addition to a trend of strengthening earnings revisions for pharma/biotech and healthcare equipment/services, they also note biotech has shown relative strength around rate-cutting cycles—a factor worth noting with a cycle expected to begin in a little more than two weeks.

The following chart of Health Care Select Sector SPDR Fund (XLV) puts the sector’s recent performance in better perspective. While it hit its lowest level since November 2023 in mid-May, it’s been in a choppy trading range—roughly $130-$140—since bouncing off the early-April tariff sell-off lows:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

The current short-term consolidation has formed toward the top of that range. In the near-term, the direction of the breakout from the smaller range may determine whether the August rally was just the latest swing within the larger range, or a sign of potentially longer-lasting momentum.

Market Mover Update: Satellites were very much in orbit on Monday. EchoStar (SATS) rallied 20% on news of a “spectrum sale” (selling its satellite licensing rights) to SpaceX. The stock was also prominent on LiveAction scans for heavy options volume, along with two other satellite stocks that staged large rallies on Monday, Globalstar (GSAT) and Gilat Satellite (GILT). Viasat (VSAT) also logged heavy options volume, despite a smaller gain for its stock. AST SpaceMobile (ASTS) went the other direction, falling 3.8%.

Rapport Therapeutics (RAPP) made what could very well turn out to be the week’s biggest move by a stock trading above $10/share. RAPP gained 119%—and rallied more than 190% intraday—after news of successful clinical trials of its anti-seizure drug.

Today’s earnings include: AeroVironment (AVAV), Rubrik (RBRK), SailPoint (SAIL), Synopsys (SNPS).

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Weekly Warm-up: Payroll Data Supports Our Thesis on Rolling Recession and Recovery. 9/8/25.