Sticky oil

- Oil prices turned higher again this week

- Futures implying less price easing vs. a few weeks ago

- Some supply challenges will linger after Strait reopens

As noted in “Bulls extend push,” in April the S&P 500 (SPX) began to respond less to the daily oil price spikes that clearly weighed on the stock market in March. For the most part, that dynamic has persisted, with Monday providing the most recent example—the SPX closed higher even though the July WTI crude oil futures jumped 8% intraday and close up more than 5%:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

While the SPX did close lower on Wednesday, it was unclear how much of that modest bearishness was the result of a continued rise in oil prices vs. climbing Treasury yields, technical fatigue after nine-straight up weeks, or other factors.

Even though the oil has eased from its April and May highs, more than four months after the US and Israel initially launched military strikes against Iran, US prices have, for most part, stubbornly held above $90.

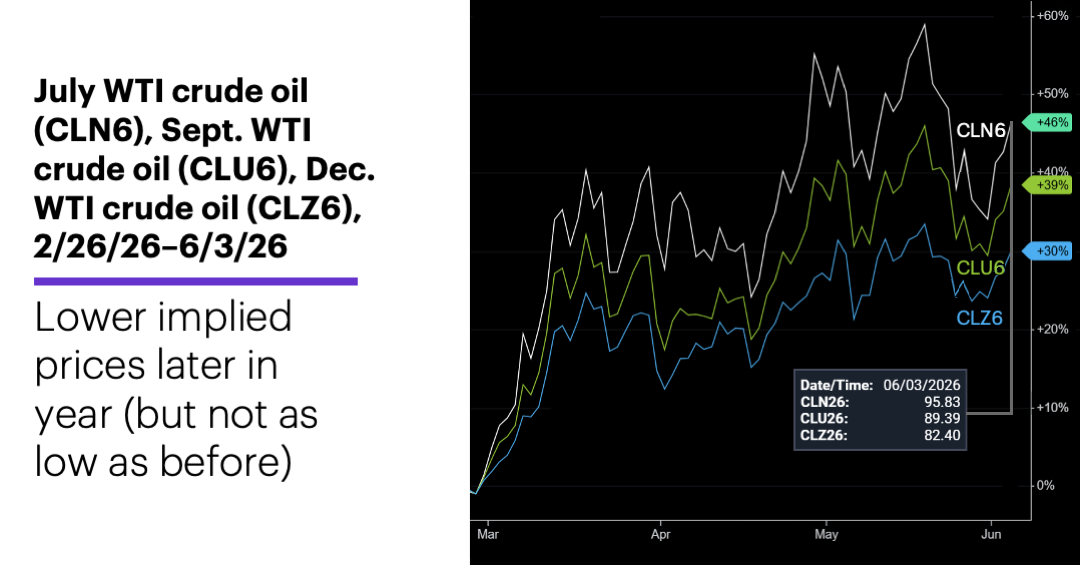

But as noted in this space on April 27, the oil futures market has consistently implied lower prices later in the year. At that time, the September WTI oil contract (CLU6) was trading around $83 and the December contract (CLZ6) was around $77.50—both well below the roughly $94.50 spot crude oil price.

Flash forward to midday Wednesday, and although the September and December oil futures prices were still notably below current levels (represented below by the July futures price), they weren’t as low as they were before. The September futures price had climbed above $89.39, while the December futures price was $82.40—more than 6% higher than it was in late April:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

The message from the futures market—that oil prices may continue to ease from current levels, but not as much as previously expected—is worth noting in the context of research from Morgan Stanley & Co. that considers the realities of resuming “normal” production and transport of oil upon the re-opening of the Strait of Hormuz.

First, the analysts have pushed back their estimate for the re-opening to late June. But because they expect “mine clearing, confidence building, and other issues” to require another few weeks, they target late July as the point at which oil exports will start to inflect higher.1 That’s nearly two months from now, and effectively six months after the beginning of the conflict.

Their base case—for global Brent crude oil, which are currently trading roughly $2 above US WTI oil prices—forecasts a “tight” third quarter “with further inventory draws ahead.” Prices may have fallen, they note, but “we stick to our 2Q/3Q Brent forecasts and raise our 4Q/1Q estimates modestly.”

In other words, a reopening of the Strait of Hormuz—whenever that may occur—doesn’t mean the global oil market will instantaneously return to its pre-conflict operational status. That suggests “stickier for longer” oil prices, with all its implications.

Foremost among those is inflation, which in turn has implications for the broader economic and financial markets. As Morgan Stanley Wealth Management strategists note, the extended Strait of Hormuz closure has increased concerns that inflationary pressures have broadened beyond oil prices. Higher energy costs, they explain, have begun to filter into core inflation through transportation and services, as well as energy-intensive industries like chemicals, lumber, and metals.2

Today’s numbers include: Challenger Job Cut Report (5:30 a.m.), Weekly Jobless Claims (8:30 a.m.), Productivity and Labor Costs (8:30 a.m.), EIA Natural Gas Report (10:30 a.m.).

Today’s earnings include: ABM Industries (ABM), Chewy (CHWY), Ciena (CIEN), Docusign (DOCU), G-III Apparel (GIII), Ollie's Bargain Outlet Holdings (OLLI), Planet Labs (PL), Rubrik (RBRK).

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. How Fast Can Middle East Production Return? 6/1/26.

2 MorganStanley.com. Fixed Income Insights: Higher-for-Longer Outlook for US Rates: Inflation and Fed Repricing. 6/2/26.