Bulls extend push

- Stocks ride fresh records into May

- Big tech, energy, financials bolster gains

- This week: jobs, 1,500-plus earnings announcements

The US stock market stepped into a new month riding a five-week win streak, buoyed by strong earnings and tech bullishness—and a continued inclination to look past high energy prices and geopolitical uncertainty.

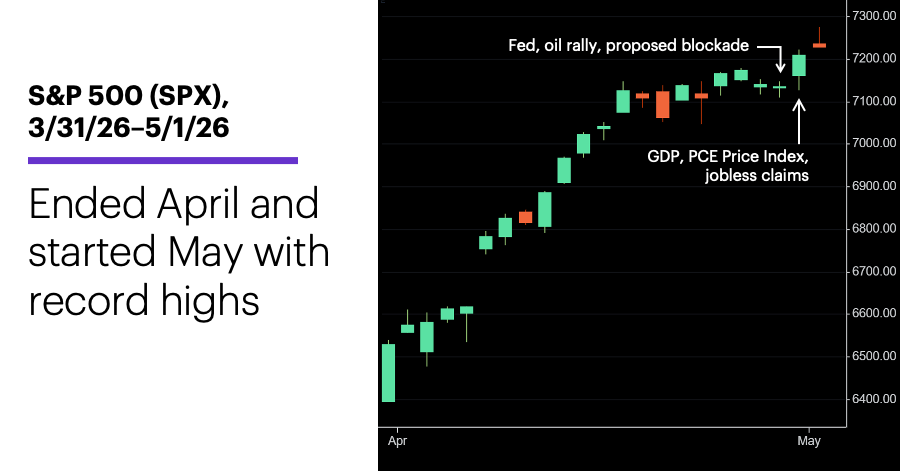

If there was a key day last week, it was Wednesday. The S&P 500 (SPX) closed only marginally lower even though US crude oil prices jumped 7% (topping $108), President Trump threatened to blockade Iran indefinitely if it didn’t agree to a nuclear deal, and the Federal Reserve made clear that rate cuts were still on a distant horizon.

A strong rally on the final day of the strongest April since 2022 spilled over to the first day of May as oil prices eased, with the SPX hitting yet another all-time high:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: New highs for stocks as earnings season powers on.

The fine print: All five of the five megacap stocks that released earnings last week topped their headline numbers, but only Alphabet (GOOGL) and Apple (AAPL) enjoyed solid post-announcement rallies. Overall, earnings season has been strong. As of Friday, the percentage of SPX companies reporting positive earnings surprises was above average, as was the size of typical surprise: 84% had topped earnings estimates (vs. a five-year average of 78%), while the average “beat” margin was 21%, nearly three times the five-year average of 7.3%.1

The numbers: 2% and 3.2%—the Q1 GDP growth rate and PCE Price Index year-over-year increase, respectively, reported last Thursday. Along with a (much) lower-than-expected weekly jobless claims total, the data presented a picture of solid economic growth, sticky inflation, and a stable labor market—a recipe for the Fed to remain on hold. Morgan Stanley & Co. economists expect the central bank to cut rates again in Q1 2027.2

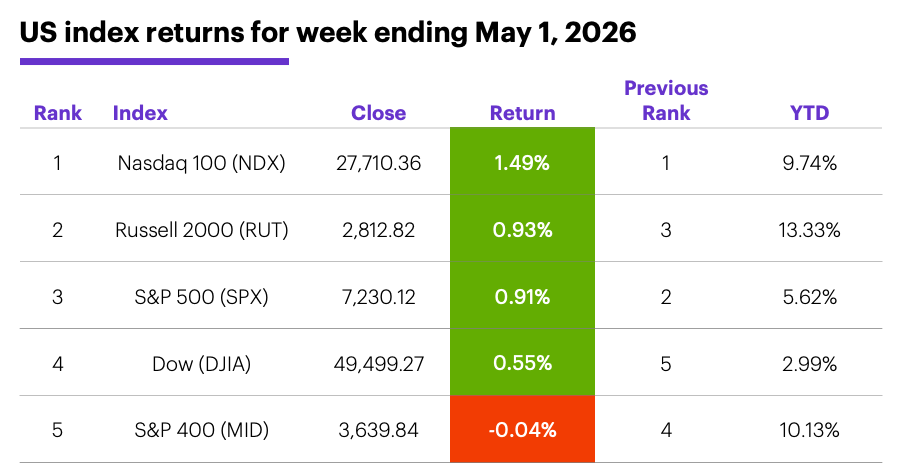

The scorecard: The Nasdaq 100 (NDX) tech index led the market for a third week. The Russell 2000 (RUT) small-cap index still leads for the year:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were communication services (+4.6%), energy (+3.5%), and consumer staples (+1.3%). The weakest sectors were materials (-1.8%), tech (+0.1%), and industrials (+0.3%).

S&P 500 movers: Last week’s biggest gains were Centene (CNC) +28% to $53.34, Seagate (STX) +24% to $726.93, and NXP Semiconductors (NXPI) +21% to $295.24. The biggest losses were Teradyne (TER) -17% to $345.42, Builders FirstSource (BLDR) -16% to $75.72, and Pentair (PNR) -14% to $79.10. Other moves: Veradermics (MANE) +48% to $100.10 on Monday, Vistance Networks (VISN) -49% to $9.90 on Wednesday.

Yields and the dollar: The 10-year US Treasury yield climbed 0.08% to 4.38% last week. The US Dollar Index (DXY) fell 0.37 to 98.16.

Commodity futures: June WTI crude oil (CLM6) jumped 7% to $106.88 last Wednesday, then pulled back to end the week up $7.54 at $101.94. June gold (GCM6) fell $96.40 to $4,4644.50. Biggest gains: July orange juice (OJN6) +16.9%, July Brent crude oil (BN6) +9.1%. Biggest declines: July butter (CBN6) -6%, June whey (DYM6) -5.5%.

Crypto: After pulling back early last week, Bitcoin rallied on Friday to end the week up 0.9% to $78,179.00. Ethereum followed a similar path but lost ground, falling 0.9% to $2,295.09.

Coming this week

The busiest week or earnings so far is heavy on tech and consumer names. Here are a few highlights:

●Monday: BP (BP), Duolingo (DUOL), Lattice Semiconductor (LSCC), ON Semiconductor (ON), Palantir (PLTR), Qiagen (QGEN), SolarEdge Technologies (SEDG), Shell (SHEL), Tyson Foods (TSN), UBS (UBS), Williams Companies (WMB)

●Tuesday: Advanced Micro Devices (AMD), BioNTech (BNTX), DigitalOcean (DOCN), Amdocs (DOX), Electronic Arts (EA), Grail (GRAL), Hinge Health (HNGE), Match Group (MTCH), Navitas Semiconductor (NVTS), Occidental Petroleum (OXY), Pfizer (PFE), PayPal (PYPL), Qorvo (QRVO), Rockwell Automation (ROK), Shopify (SHOP), Workiva Inc (WK)

●Wednesday: Albemarle (ALB), AppLovin (APP), Arm Holdings (ARM), CVS Health (CVS), DoorDash (DASH), Walt Disney (DIS), Global Payments (GPN), Grindr (GRND), Globalstar (GSAT), Johnson Controls International (JCI), Marriott International (MAR), Murphy Oil (MUR), Royal Gold (RGLD), Uber Technologies (UBER), Whirlpool (WHR)

●Thursday: Airbnb (ABNB), Bill Holdings (BILL), Coinbase (COIN), CoreWeave (CRWV), Dropbox (DBX), Shift4 Payments (FOUR), JFrog (FROG), Howard Hughes (HHH), Lyft (LYFT), McDonald’s (MCD), Rocket Lab (RKLB), NuScale Power (SMR), Tapestry (TPR) Wynn Resorts (WYNN)

●Friday: PPL (PPL)

An employment-dominated week of economic data concludes with the monthly jobs report:

●Monday: Factory Orders, vehicle sales

●Tuesday: Trade Balance, ISM Services Index, Job Openings and Labor Turnover Survey (JOLTS), New Home Sales (delayed Feb. data)

●Wednesday: ADP Private Employment Report

●Thursday: Job Cuts, Productivity and Labor Costs (prelim), Construction Spending, NY Fed Consumer Inflation Expectations

●Friday: Employment Report, Consumer Sentiment (prelim)

Daily oil shocks losing their impact?

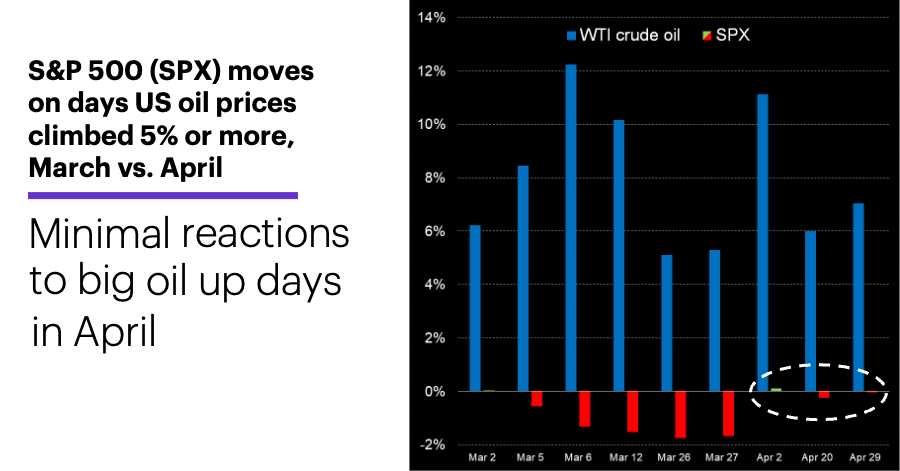

It’s difficult to argue that the SPX’s 5.1% decline in March—it’s biggest monthly loss in a year—was unrelated to the 55% jump in crude oil prices that month. The stock market, understandably, took a cautious view of the potential economic impact of energy prices remaining at multi-year highs for an unforeseeable period of time.

While US crude oil’s 4% April rally paled in comparison to March’s surge, it was still an increase—one that pushed spot prices above $108 near the end of the month. But the SPX not only didn’t drop in April, it posted its best monthly return since 2022. And just as stock traders and investors appeared to look past geopolitics last month, the oil futures market itself was implying lower prices later in the year.

Looking at the relationship at a more granular level shows a stark difference in the way the stock market reacted to big up days in the oil market in March vs. April. Of the six days in March that spot oil prices climbed at least 5%, the SPX closed lower on all but the first, and it fell more than 1.3% on four of them:

Source (data): EIA.gov and Power E*TRADE Pro. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index.)

Last month was a different story. On the three days that crude oil rallied 5% or more (most recently on April 29), the SPX posted two small losses and a small gain, suggesting the oil market was losing some of its psychological grip on the stock market.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 FactSet.com: S&P 500 Earnings Season Update: May 1, 2026.

2 MorganStanley.com. April FOMC Reaction Later Cuts and a Longer Hold. 4/30/26.