Mixed messages, mixed markets

- S&P 500 slips as politics take center stage

- Tech rotation continues, precious metals climb

- This week: SCOTUS rulings, Davos, earnings

Wall Street ran through Washington D.C. last week, as the focus on the first week of earnings season was challenged by various events emanating from the capitol—another challenge to Fed independence, new questions about who the next Fed chairmain will be, continued “geopolitical swirl,” a proposed cap on credit card interest rates, and a possible plan to allow investors to tap their 401(k) plans to fund home purchases.

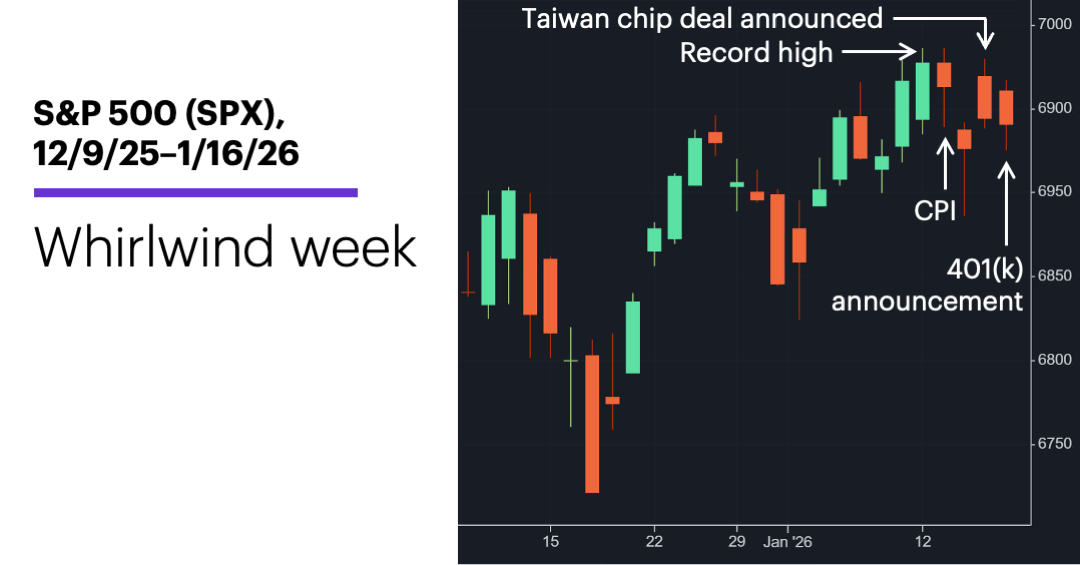

The net result was choppy trading that left the S&P 500 (SPX) little changed for the week, although small- and mid-cap stocks extended their recent burst of relative strength. After falling to its lowest intraday level since the first day of the year last Wednesday, the SPX bounced enough on Thursday to end the week with a small loss:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Broad market flat, but small- and mid-cap stocks continue climb.

The fine print: Like last week, this week may revolve around politics. In addition to Greenland, the Supreme Court is expected to rule on the legality of tariffs, as well as hear arguments in the Trump vs. Cook “Fed independence” case (stemming from the White House’s attempt to remove Federal Reserve Governor Lisa Cook). President Trump is also scheduled to speak at the World Economic Forum in Davos, Switzerland, and possibly offer details about the plan to allow US investors to fund home purchases with 401(k) assets.

The number: 4. Of the six big banks that reported their Q4 numbers last week, four sold off despite beating their headline earnings numbers—possibly because of the negative sentiment surrounding the White House’s proposed 10% cap on credit card interest rates.

The move: In an otherwise lackluster week for tech, the PHLX Semiconductor Index (SOX) rallied 3.8%, buoyed in part by the announcement of a $250 billion US-Taiwan deal to build chips on American soil.

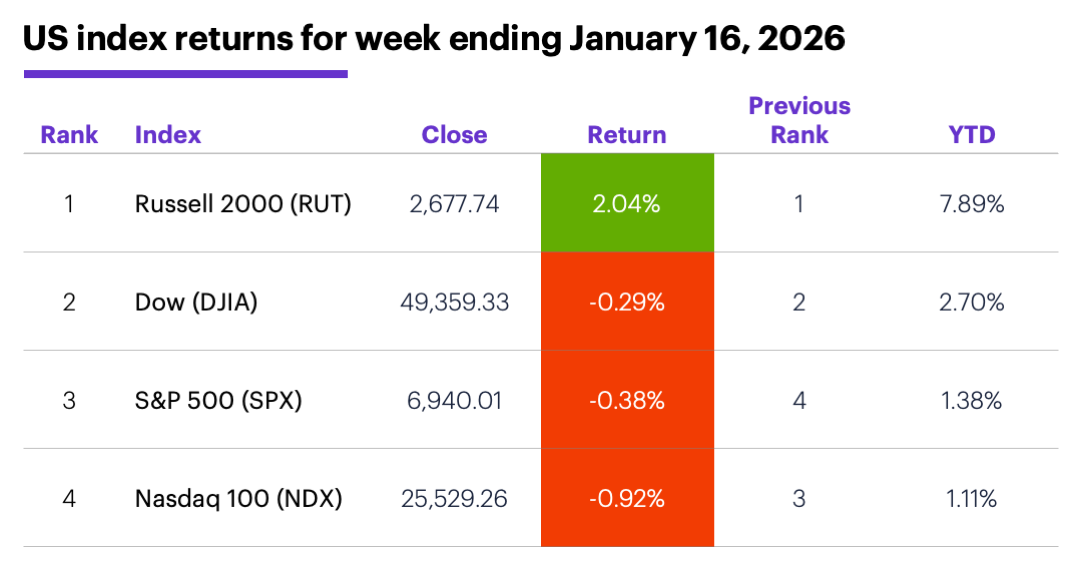

The scorecard: Although it’s not listed, the S&P 400 mid-cap index (MID) gained 1.3% last week, second only to the Russell 2000 (RUT) small-cap index. Friday marked the 10th day in a row that the RUT outperformed the SPX:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were real estate (+3.9%), consumer staples (+3.3%), and industrials (+2.9%). The weakest sectors were financials (-2.4%), consumer discretionary (-2%), and communication services (-1.5%).

Stock moves: BioAge Labs (BIOA) +27% to $17.85, Forte Biosciences (FBRX) +24% to $29.66, both on Monday. Alphatec (ATEC) -22% to $17.59 on Monday, Regencell Bioscience (RGC) -26% to $32.54 on Tuesday.

Yields and the dollar: The 10-year US Treasury climbed 0.06% to 4.23% last week, thanks to a big jump on Friday. The US Dollar Index (DXY) rallied 0.26 to a nearly seven-week high of 99.39.

Futures: March gold (GCH6) hit multiple record highs, closing Friday up $82.70 at $4,601.10. March WTI crude oil (CLH6) hit a three-and-a-half month high of $62.20 last Wednesday amid rising US-Iran tensions, then pulled back to end the week up just $0.60 at $59.22 as those tensions eased. Biggest rallies: March silver (SIH6) +11.6%, March lumber (LBSH6) +7.9%. Biggest declines: March cocoa (CCH6) -5%, March corn (ZCH6) -4.7%.

Coming this week

This week’s numbers include:

●Wednesday: Pending Home Sales, Construction Spending

●Thursday: Q3 GDP (final), PCE Price Index, Personal Income and Spending

●Friday: S&P Global Manufacturing and Services PMIs (flash), Consumer Sentiment

The second week of earnings season has a bit of everything, including big airlines, big pharma, big consumer names, and Netflix (NFLX):

●Tuesday: Alaska Air Group (ALK), D.R. Horton (DHI), Fastenal (FAST), Fifth Third Bancorp (FITB), KeyCorp (KEY), Kinder Morgan (KMI), 3M (MMM), Netflix (NFLX), United Airlines (UAL), US Bancorp (USB), Wintrust (WTFC)

●Wednesday: American Airlines (AAL), Freeport McMoRan (FCX), Halliburton (HAL), Johnson & Johnson (JNJ), Travelers (TRV)

●Thursday: Alcoa (AA), Abbott Laboratories (ABT), CSX (CSX), General Electric (GE), Intuitive Surgical (ISRG), McCormick & Company (MKC), NovaGold (NG), Procter & Gamble (PG)

●Friday: Booz Allen Hamilton (BAH), Comerica (CMA), SLB (SLB)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Deconcentration and the Magnificent…2?

Two weeks doesn’t prove anything, but so far, the 2026 performance of the Magnificent-7 stocks has been more or less in line with 2025—that is, mostly underperforming the S&P 500 (SPX).

Last year only two of the long-time megacap market leaders—Alphabet (GOOGL) and NVIDIA (NVDA)—outperformed the SPX. This year, the number is still two, with Amazon (AMZN) replacing NVDA (which barely missed making the cut):

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

MorganStanley Wealth Management believes the longstanding dominance of the SPX’s top 10 components could be peaking, resulting in a “deconcentration” that results in new market leadership—a shift that could limit gains at the index level, but would also potentially offer opportunities for active stock selection. While the strategists consider rotation away from a handful of megacap leaders a healthy development, they also point out it requires investor diligence and a focus on “maximum strategic diversification.”1

So, while two weeks doesn’t prove anything, a year and two weeks may represent a trend worthy of further consideration.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. The GIC Weekly: Deconcentrating. 1/12/26.