Market digests jobs data

- S&P 500 grinds out gain in first week of September

- Jobs data comes up short, gold sets more records

- This week: inflation (CPI and PPI), consumer sentiment

Last week began and ended like a poster child for seasonal stock-market weakness. In between, it looked like the market traders and investors have become familiar with in recent months—one that has often pushed past obstacles to record highs.

Despite a steady stream of weaker-than-expected employment data—including Friday’s jobs report miss—the broad market gained ground for the week. The S&P 500 (SPX) closed at a record high on Thursday and hit an intraday record high early Friday before closing lower on the day:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Stocks grind higher even as labor-market cracks widen.

The fine print: Away from the economic data, the market received a couple of high-profile boosts from tech last week. Alphabet (GOOGL) jumped more than 9% last Wednesday after prevailing in an antitrust lawsuit, while Broadcom (AVGO) rallied a similar amount on Friday after a positive earnings report.

The number: 4. September marks the fourth month in a row that the SPX has hit a new record high.

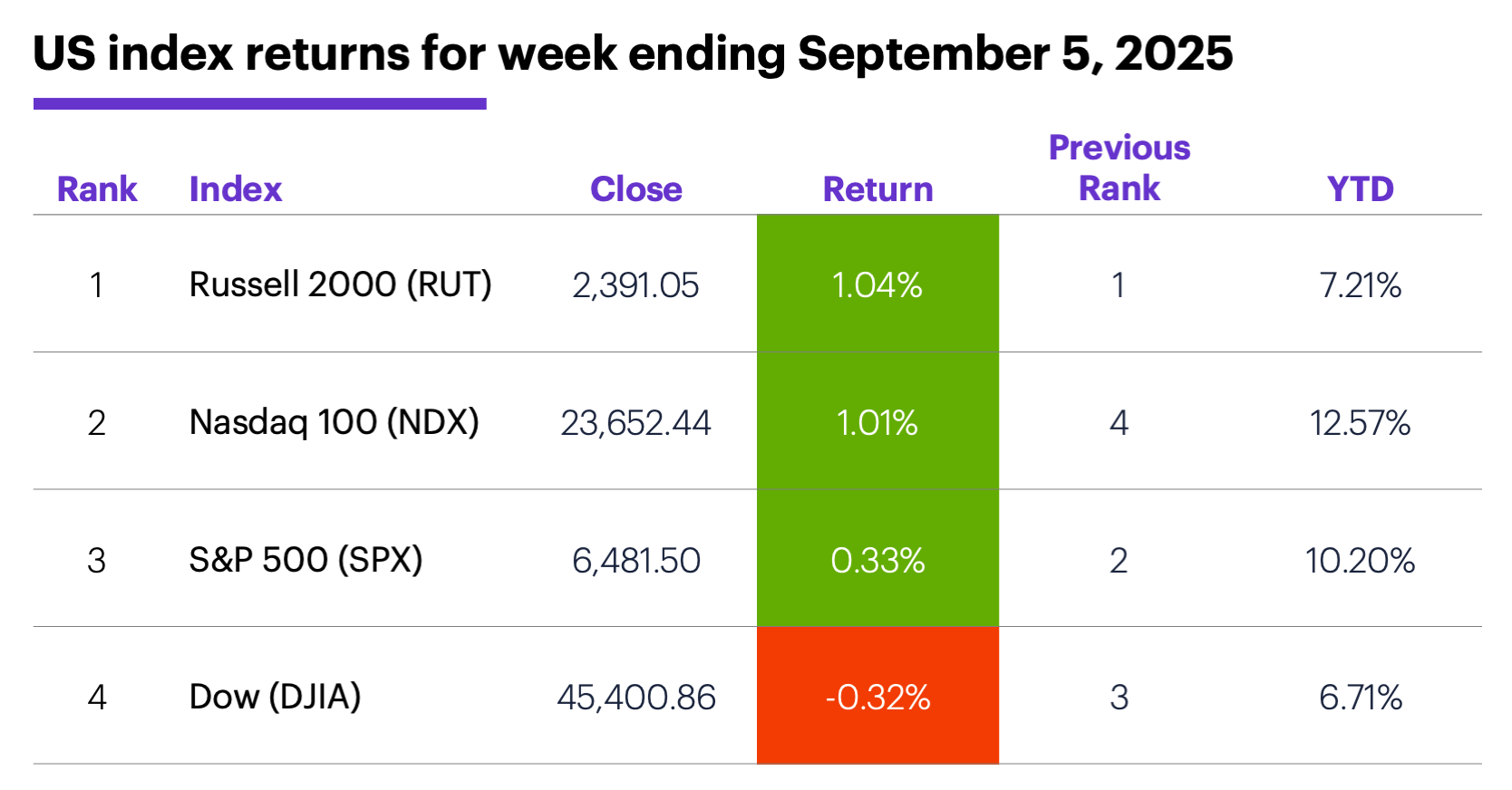

The scorecard: The Russell 2000 (RUT) small-cap index extended its relative strength streak for a rare fourth week. The Dow was the only major index to lose ground:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were communication services (+4.7%), health care (+1.1%), and consumer staples (+1%). The weakest sectors were energy (-3%), industrials (-1.8%), and financials (-1.5%).

Stock moves: Mineralys Therapeutics (MLYS) +86% to $28.86 on Tuesday, American Eagle Outfitters (AEO) +38% to $18.79 on Thursday. On the downside, Newegg (NEGG) -20% to $30.97 on Wednesday (then +30% to $40.25 on Thursday), Bullish (BLSH) -13% to $54.26 on Wednesday.

Yields: The 10-year US Treasury yield fell 0.13% to a five-month low of 4.09% last week.

US dollar: The US Dollar Index (DXY) was unchanged for the week at 97.77.

Futures: Gold prices hit record highs every day last week except Thursday. December gold (GCZ5) rallied $137.20 to $3,653.30 for the week. October WTI crude oil (CLV5) fell $2.10 last week, closing Friday at a three-month low of $61.87. Biggest rallies: December gold (GCZ5) +5.2%, October ethanol (ZKV5) +5.1%. Biggest declines: October sugar (SBV5) -5.6%, November orange juice (OJX5) -5.5%.

Coming this week

The markets move on to the final inflation numbers before next week’s Fed meeting:

●Monday: New York Fed consumer inflation expectations, consumer credit

●Tuesday: NFIB Business Optimism Index

●Wednesday: producer price index (PPI), wholesale inventories

●Thursday: consumer price index (CPI)

●Friday: consumer sentiment (preliminary)

This week’s earnings include:

●Monday: Casey’s General Stores (CASY), Oracle (ORCL), Dave & Buster's (PLAY)

●Tuesday: AeroVironment (AVAV), Rubrik (RBRK), SailPoint (SAIL), Synopsys (SNPS)

●Wednesday: Oxford Industries (OXM), RH (RH)

●Thursday: Adobe (ADBE), Kroger (KR)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Jobs, interest rates, and the markets

The SPX’s downside pivot on Friday may suggest investors were, at least for the moment, reconsidering the potential benefit of a weak labor market (rate cuts) against its possible downside (a too-slow economy).

Ellen Zentner, Chief Economic Strategist for Morgan Stanley Wealth Management, believes labor-market weakness is “easily explained by shifting policies on trade, immigration, and government downsizing plus the first signs of AI disruption,” and that leading indicators point to further weakening. But she also notes that while the jobs market isn’t necessarily healthy, it isn’t falling off a cliff, either.

According to Zentner, the stock market’s recent “bad news is good news” pattern will work only if the Fed lowers rates—which she thinks it will later this month, and again in December. She also believes rate cuts have the potential to directly help the jobs picture by lowering short-term borrowing costs—which, among other benefits, may make companies more confident about growing payrolls.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.