“Buy now, pay later”: Banking on global financial innovation

Morgan Stanley Research

11/23/21Summary: The new credit payment is the latest Fintech disruptor. Can established legacy banks adapt to keep up with the increased e-commerce demand and the red-hot tech services?

The latest Fintech sounds simple enough: Buy a product, take it home, set up payments after. However, the changes this innovation may bring to the financial sector are anything but. In fact, “buy now, pay later” (BNPL) platforms—adopted, so far, mainly by app-loving Millennials and Gen Z—are changing how people shop and spurring financial institutions to keep up.

BNPL is one of the fastest-growing e-commerce segments in Europe and Australia, and it is expanding across the US. That means potential disruption for legacy financial services companies, which must compete to offer similar services to existing customers, while adapting to (and adopting) this type of retail-financing Fintech to grow their customer base.

Not to be defeated in the tech space, some incumbents have formed notable partnerships and acquisitions with BNPL providers, while offering installment plans and other similar offerings to consumers.

Why is “buy now, pay later” popular?

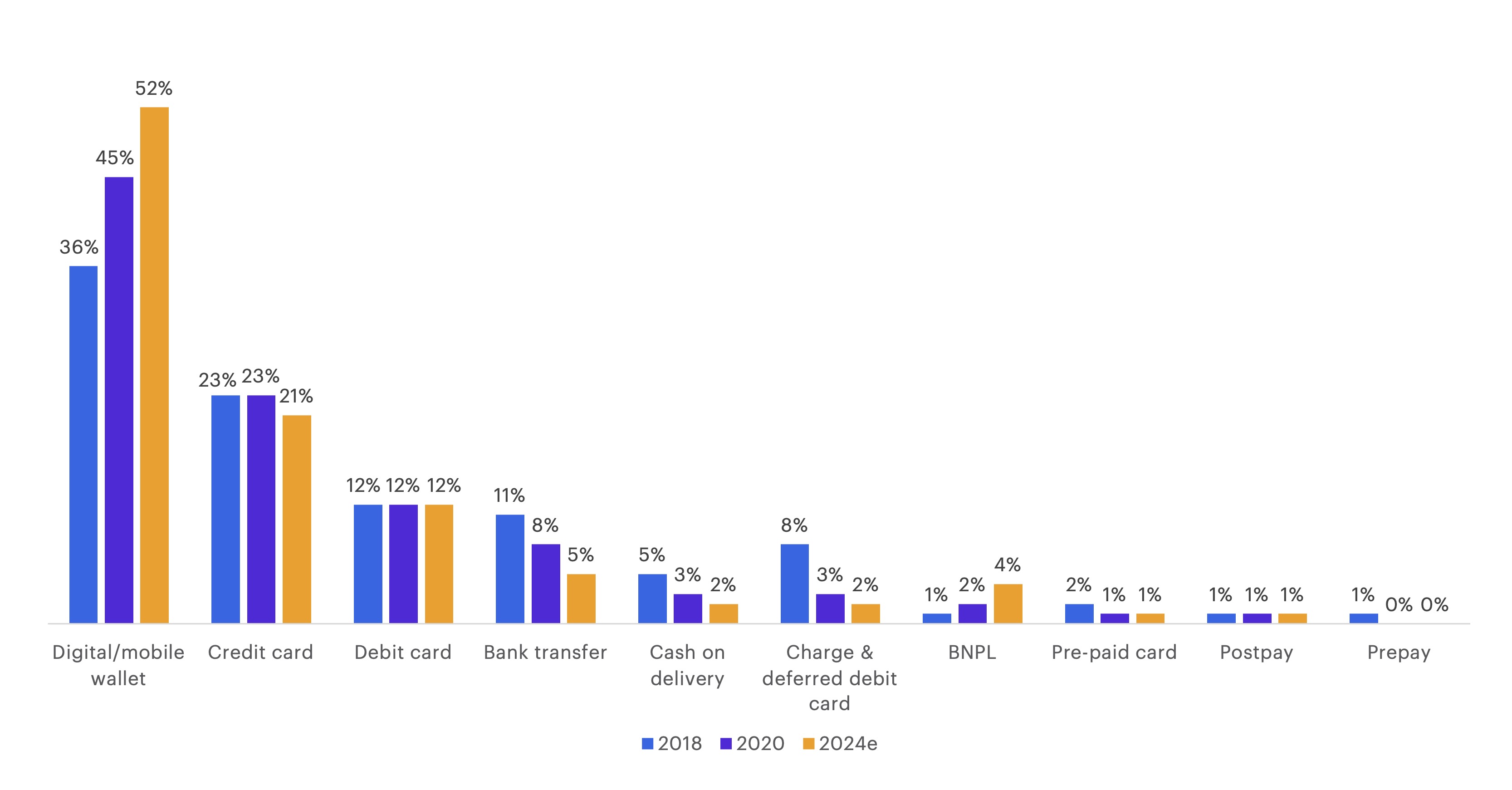

BNPL currently represents only a portion of overall global online purchases—2% in the US, 7% in Europe, 10% in Australia—but it’s growing. And Morgan Stanley Research analysts say that the potential growth from the generational shift to this innovation cannot be underestimated.

BNPL currently only represents 2% of all global online purchases…

Source: Worldpay global payments report

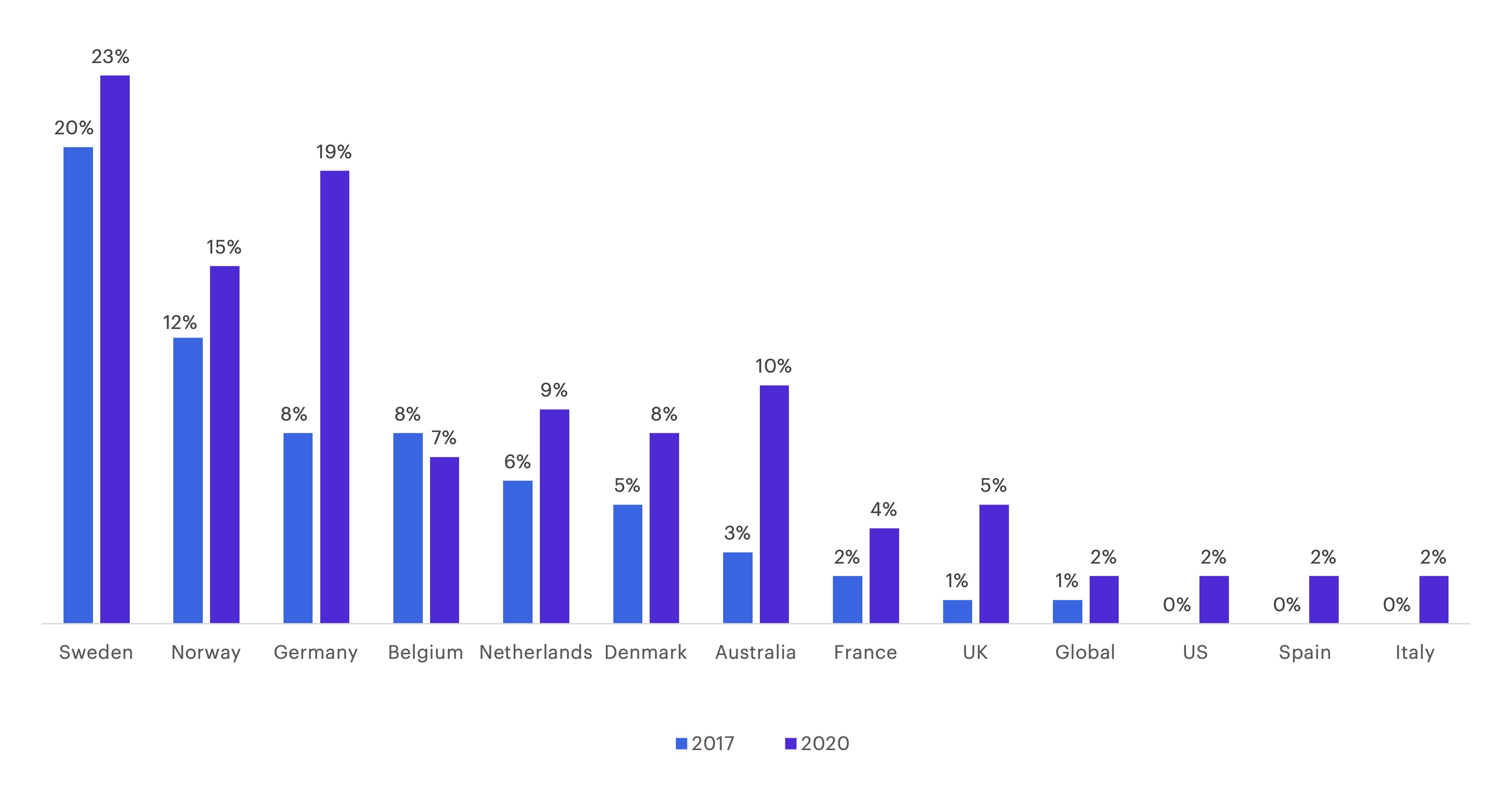

… But it’s the fastest-growing payment method globally, and some markets in Europe see the highest adoption (Sweden, Germany)

Source: Worldpay global payments report

In a previous report, “How a ‘Youth Boom’ Could Shake Up Spending Trends,” Morgan Stanley noted that 73 million Millennials and 78 million Gen Z in the US could be the “pillars of GDP growth,” even amid the ongoing pandemic. This points to significant implications for retailers in several categories, including the food and beverage industries, electronics, and travel—and Fintech.

Many young, digitally minded shoppers have long-used peer-to-peer payments, and the overall share of retail spending by Millennials and Gen Z is expected to be as high as that of Gen X and older cohorts by 2030 across the UK, Australia, and the US.

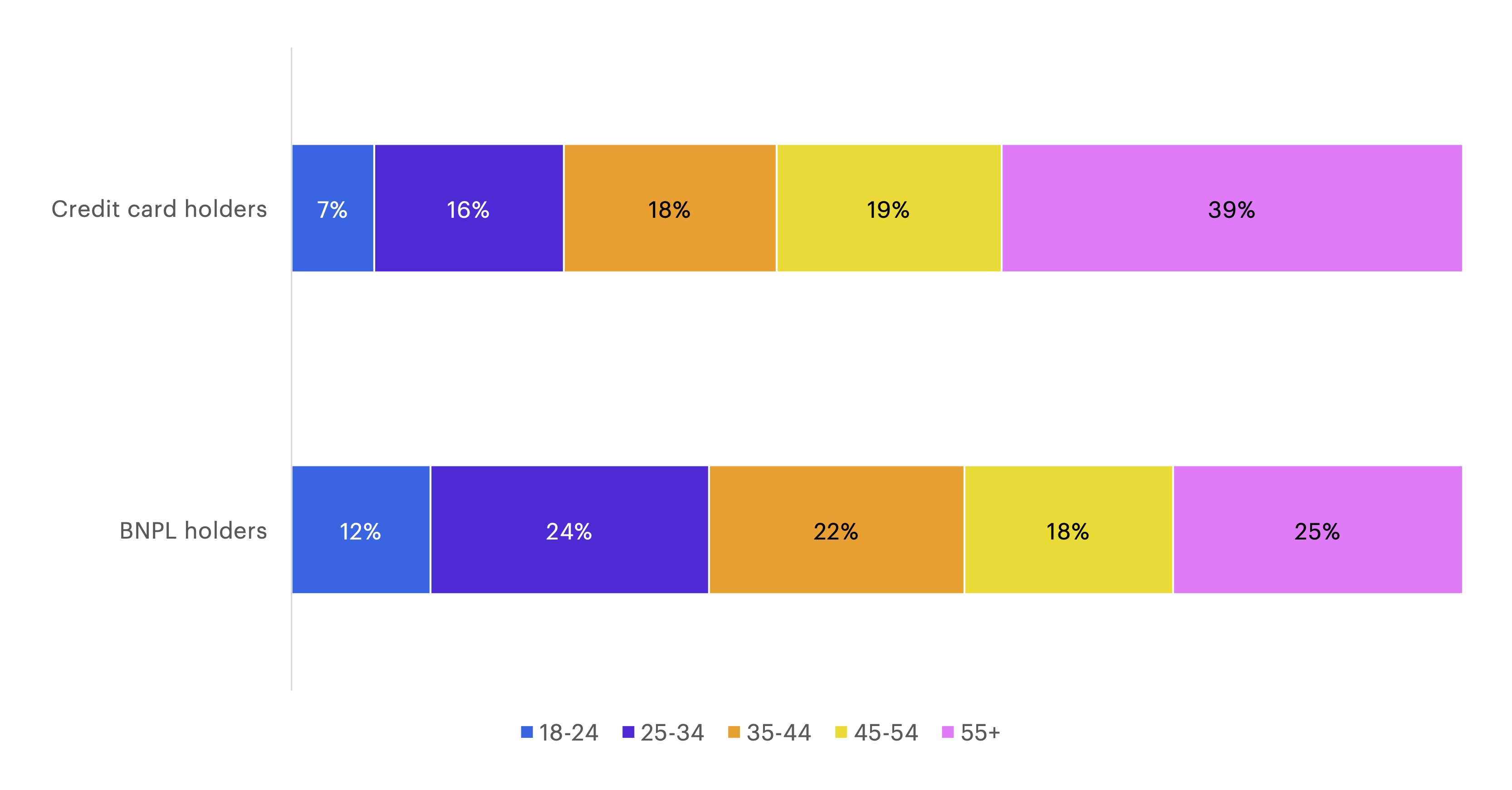

Age distribution of all adults that have used BNPL services in 2020 vs. distribution of credit-card holders in the UK 2020

Source: Capital Economics analysis, YouGov January 2021, ONS analysis, FCA: "Understanding the financial lives of UK adults," Morgan Stanley Research

Here’s why BNPL brands and marketing resonate with Millennials and Gen Z:

- Simplicity and cost (they don’t charge interest, and late fees apply only if customers miss payments)

- Engaging apps that provide multiple features like wish lists, targeted offers, and budgeting tools

- Products are merchant subsidized, and providers take on the credit risk

High growth, big disruption?

Fintechs have raised more than $80 billion globally and $19 billion in Europe alone year to date, outpacing total fund inflows into the sector compared to the same period last year; and BNPL has raised $2.95 billion year to date in Europe, according to Pitchbook/Morgan Stanley Research.

Already there are big changes in the retail segment, where gross merchandise volume growth (i.e., the retailers’ sales to which BNPL companies charge a margin) reached 90% year-over-year in the last 12 months for the BNPL platforms Morgan Stanley tracks globally. The results are driving high valuations, even though a number of providers are losing money as they pursue growth.

Morgan Stanley views BNPL as an alternative payment method (APM). For analysts, that means that BNPL and the complexity of the payment landscape might accelerate with more APMs entering the marketplace.

In the short term, Morgan Stanley Research analysts see limited impact to banks’ earnings, mostly related to a slower growth in credit cards. Over the long term, however, analysts see a bigger risk, stressing the importance for banks to develop apps that are able to engage customers.

The source of this Morgan Stanley article, ‘Buy Now, Pay Later’: Banking on Global Financial Innovation, was originally published on November 11, 2021.

How can E*TRADE help?

Thematic Investing

Find ETFs that align with your values or with social, economic, and technology trends.

Brokerage account

Investing and trading account

Buy and sell stocks, ETFs, mutual funds, options, bonds, and more.