Stocks reclaim record levels

E*TRADE from Morgan Stanley

The US stock market heads into the second half of the year at all-time highs, riding strength in the tech sector past geopolitical risk and continued tariff uncertainty.

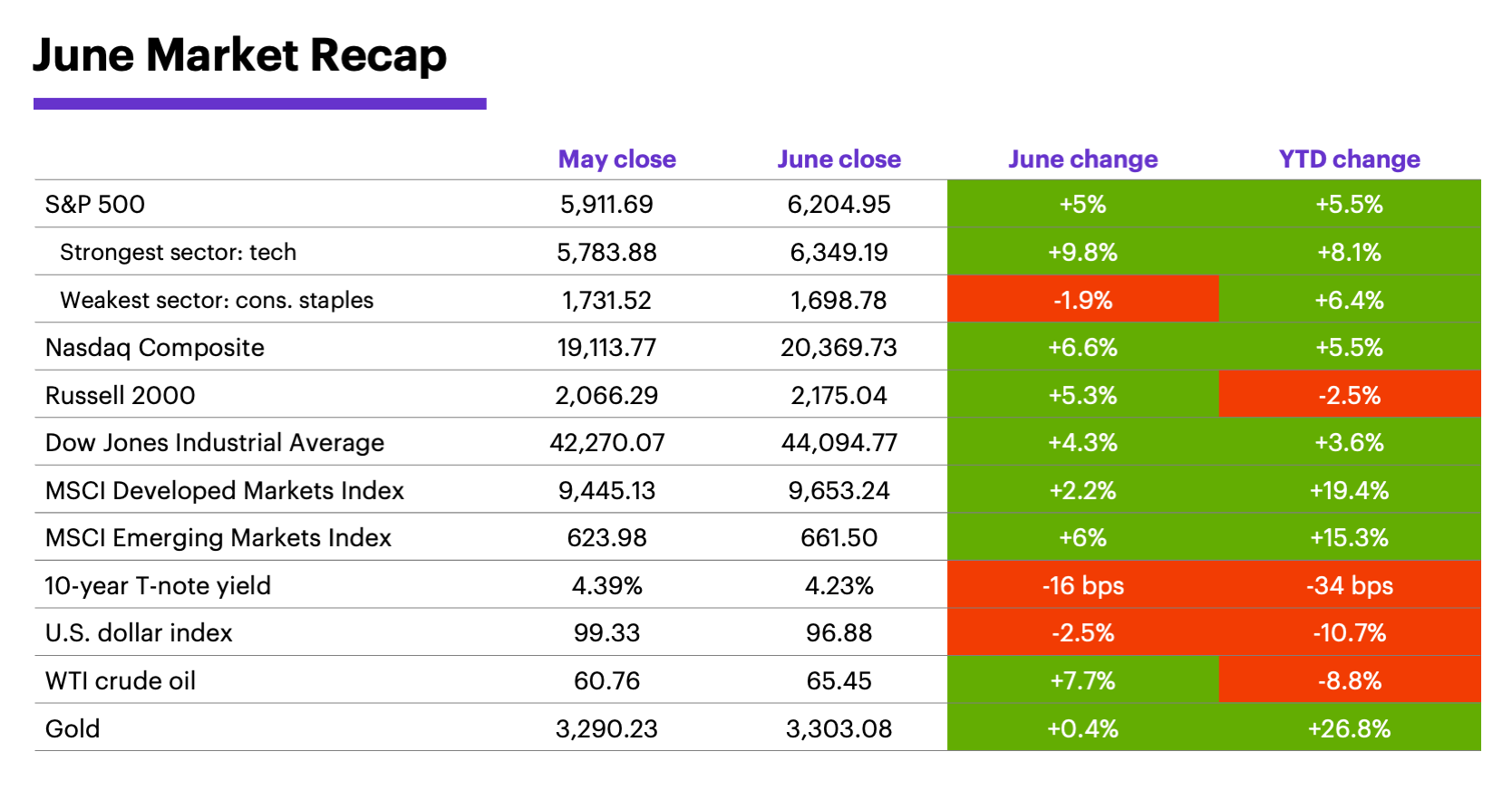

The S&P 500 closed June in positive territory, having rallied nearly 25% off its April low to hit new record highs for the first time since February, and posting its strongest two-month return since December 2023:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.)

Geopolitics temporarily upstaged tariffs in June. Although Israeli and US airstrikes on Iran caused US oil prices to briefly spike to a five-month high, the stock market’s reaction was contained. As of June 30, the SPX hadn’t fallen more than 1.7% below its June 12 close, the day before the first strikes.

Deadlines may not be deadlines after all. In late June, the White House suggested the July 9 expiration of the 90-day tariff pause “wasn’t critical,” floating the idea that it could be extended, or that different deals could be negotiated.1 Meanwhile, it remains unclear whether the Senate will be able to pass the “big, beautiful” tax and spending bill by the White House’s July 4 deadline.

Despite the return to record levels, investors may want to resist the urge to chase the stock market. Given superior yields and a favorable policy backdrop, short- to intermediate-term Treasuries and investment-grade bonds could outperform the stock market in the second half of the year, according to Morgan Stanley Wealth Management.2

While a near-term test of the April sell-off lows may be a low-probability event, Morgan Stanley Wealth Management notes a continued stock market rally faces a few potential headwinds, including elevated policy uncertainty in the US (e.g., tariffs and the budget bill), geopolitical stresses, potential weakening in the US labor market, and pressures on corporate profit margins.3

Tech did the heavy lifting for bulls last month. The tech sector was largely responsible for last month’s record index highs, following through on a strong May with an equally strong June. Consumer staples was the weakest S&P 500 sector, and the only one to decline.

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment).

Although the S&P 500 outperformed developed markets last month, it lagged emerging markets. Overall, Morgan Stanley & Co. strategists continue to prefer US over international stocks. A key reason: US dollar weakness is providing a “tailwind for rebounding US earnings revisions breadth,” while earnings revisions for Europe and Japan have yet to inflect meaningfully higher.4

Long-term yields retreated along with the dollar. In May, rising long-term interest rates appeared poised to threaten further stock market gains. They eased notably last month, with the benchmark 10-year Treasury yield falling 0.16% to 4.23%. The US dollar Index ended June at its lowest level since February 2022.

The Federal Reserve kept its cards close to its vest. The Fed held interest rates steady last month, and is expected to do the same later this month, as it continues to wait for more clarity on tariffs.

Demand for the minerals critical to humanoid robots could skyrocket, but the market is currently dominated by China.

Insight of the month: Robots, critical minerals—and China. According to Morgan Stanley & Co., the emergence of a multi-trillion-dollar humanoid robot market means demand for the minerals required to build them (including “rare earths,” lithium, and graphite) could skyrocket. China currently dominates this market, and a comprehensive deal on these materials has yet to emerge.5 Morgan Stanley & Co.’s global materials team recently laid out 34 global stocks tied to investing in the theme in these minerals.

July market history. July has been a positive month for the S&P 500 for the past 10 years, but its prior performance was much less bullish. Since 1991, July has the third-highest median return of any month (1.8%), and is tied for third in how often it was an up month (22 of 34 years, or 65%). By contrast, from 1991-2014, July was last in both categories.6

Important dates: Employment Report (7/3), end of tariff “pause” (7/9), FOMC minutes (7/9), CPI (7/15), PPI (7/16), retail sales (7/17), housing starts (7/17), Fed interest rate decision (7/30), Q2 GDP, initial estimate (7/30), PCE Price Index (7/31).

1 CNBC.com. Trump trade deadlines in July ‘not critical’: White House. 6/26/25.

2 MorganStanley.com. Why Bonds May Keep Beating Stocks. 6/25/25.

3 MorganStanley.com. Four Risks Investors Shouldn’t Ignore. 6/17/25.

4 MorganStanley.com. Leading Indicators Point to Earnings Resiliency. 6/16/25.

5 MorganStanley.com. Humanoids Insatiable Hunger for Minerals. 6/25/25.

6 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2024. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.