Market steps back from highs

- Stocks dip as data signals solid economy, stable inflation

- Energy stocks rally with oil, small caps cool

- This week: jobs report, government shutdown deadline

Whether you call it a just a hint of seasonal weakness or simply a natural pullback within a strong rally, the end result was the same—the first down week for US stocks since August.

After starting last week with another record high, the S&P 500 (SPX) retreated despite a steady stream of better-than-expected economic data, as rallies in some megacap tech stocks lost momentum. But the market bounced on Friday despite the announcement of new tariffs:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Economy shows some heat, stocks cool.

The fine print: Last week’s resilient economic data may have actually worked against bullish sentiment, since a stronger economy could appear to make additional Fed rate cuts less urgent. (Fed Chair Jerome Powell’s comment last Tuesday that stocks may be “fairly highly valued” probably didn’t help the market, either.) GDP was revised higher, jobless claims dropped, and the PCE Price Index showed inflation was steady. At the end of the week, the market-based probability of a 0.25% rate cut later this month stood at 90%.

The number: 4, the number of new tariffs announced last week—100% on branded pharmaceuticals, 50% on kitchen cabinets and bathroom vanities, 30% on “upholstered furniture,” and 25% on heavy trucks. One outlier: The tariffs on European auto imports was lowered to 15%.

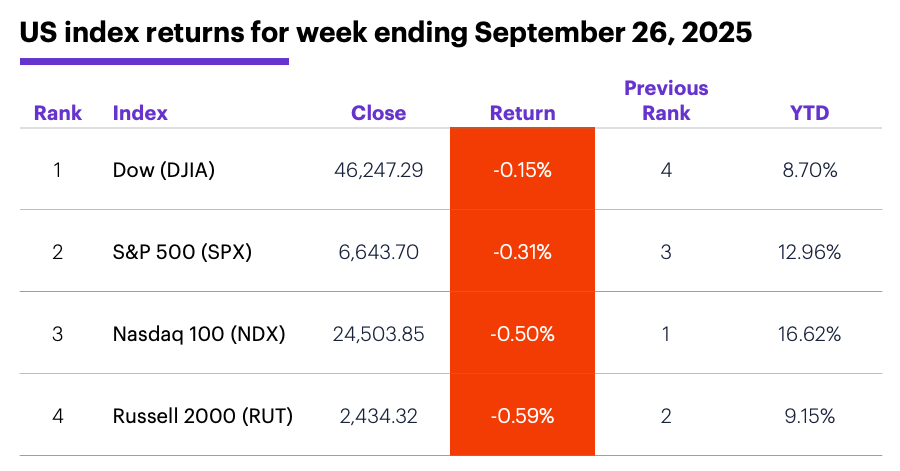

The scorecard: The Russell 2000 (RUT) small-cap index slipped the most last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were energy (+4.7%), utilities (+2.8%), and real estate (+0.9%). The weakest sectors were communication services (-2.7%), materials (-2%), and consumer discretionary (-1.2%).

Stock moves: MBX Biosciences (MBX) +100% to $20 on Monday, UniQure (QURE) +248% to $47.50 on Wednesday. On the downside, Newegg (NEGG) -20% to $44.01 on Monday, CarMax (KMX) -20% to $45.60 on Thursday.

Yields: The 10-year US Treasury yield climbed 0.05% to 4.18%.

US dollar: The US Dollar Index (DXY) rallied 0.51 to 98.15

Futures: November WTI crude oil (CLX5) jumped after pulling back into a long-standing support zone, ending last week up $3.32 at $65.72—its highest close since July. December gold (GCZ5) ended the week up $103.20 at a new record high of $3,809. Biggest rallies: January platinum (PLF6) +12.2%, December palladium (PAZ5) +11.6%. Biggest declines: September ether (ETHU5) -11.3%, October bitcoin (BTCV5) -5.5%.

Coming this week

The labor market returns to center stage this week, but a potential government shutdown may dominate the first 48 hours of the work week:

●Monday: pending home sales

●Tuesday: S&P Case-Shiller Home Price, FHFA House Price Index, Chicago PMI, Job Openings and Labor Turnover Survey (JOLTS), consumer confidence, government funding/shutdown deadline

●Wednesday: ADP private employment, S&P Global Manufacturing PMI, ISM Manufacturing Index, construction spending, auto sales

●Thursday: job cuts, factory orders

●Friday: Employment Report, S&P Global Services PMI, ISM Services Index

This week’s earnings include:

●Monday: Carnival (CCL), Vail Resorts (MTN), Progress Software (PRGS)

●Tuesday: Levi Strauss (LEVI), Lamb Weston (LW), Nike (NKE), Paychex (PAYX), United Natural Foods (UNFI)

●Wednesday: Acuity Inc (AYI), Conagra Brands (CAG), Cal-Maine Foods (CALM), RPM International (RPM)

●Thursday: AngioDynamics (ANGO), Apogee Enterprises (APOG)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

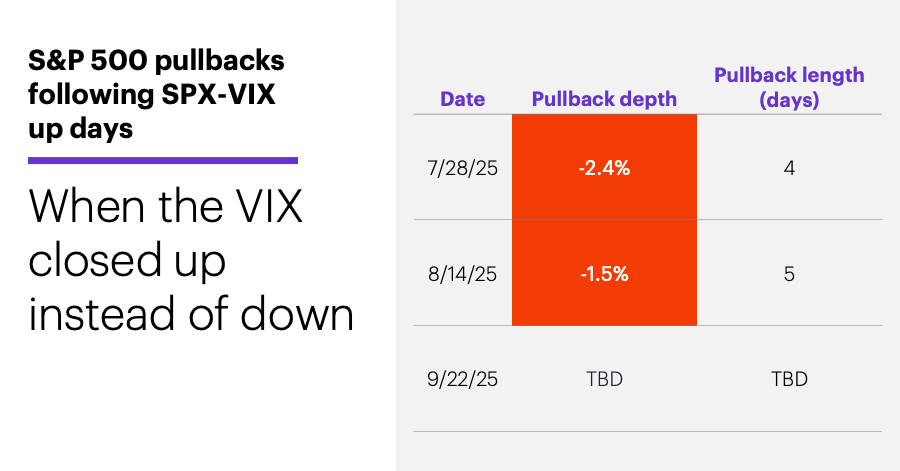

VIX clicks again

Since the SPX first rallied to fresh record highs in June, the index has logged only four pullbacks larger than 1%. Three of these moves, including last week’s, followed days that the Cboe Volatility Index (VIX) closed higher the same day the SPX closed at a new high:1

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index. ”Pullback depth” refers to the percentage change from the close of the day before the pullback started to the lowest close of the pullback. “Pullback length” refers to the number of trading days it took the pullback to reach its lowest close.)

The most notable exception was the pullback that followed the August 28 record high—a day the VIX closed lower, following the typical pattern of the VIX declining when the SPX rallies.

The other side of the coin is that these weren’t the only times the VIX closed higher the same day the SPX closed at a new high. Since late June, the VIX has closed higher the same day the SPX closed at a record high nine times, with the SPX closing lower at least the next day in five instances.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 Reflects S&P 500 (SPX) and Cboe Volatility Index (VIX) daily price data, 6/1/25–5/26/25. ”Pullback depth” refers to the percentage change from the close of the day before the pullback started to the lowest close of the pullback. “Pullback length” refers to the number of trading days it took the pullback to reach its lowest low. Supporting document available upon request.