Stocks dip ahead of trade talks

- Mixed week for stocks amid tariff anticipation

- Fed still cautious, but cites “resilient” economy

- This week: inflation (CPI and PPI), retail sales

After five weeks of rollercoaster trading, stocks appeared to take a breather last week as traders and investors looked ahead to upcoming trade negotiations with China and the latest US inflation readings.

The S&P 500 (SPX) narrowly missed a third-consecutive up week, which would have been its longest run since October. But soft trading on Friday left the index in the red for the week, just a little below where it was before the April 2 tariff announcement:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

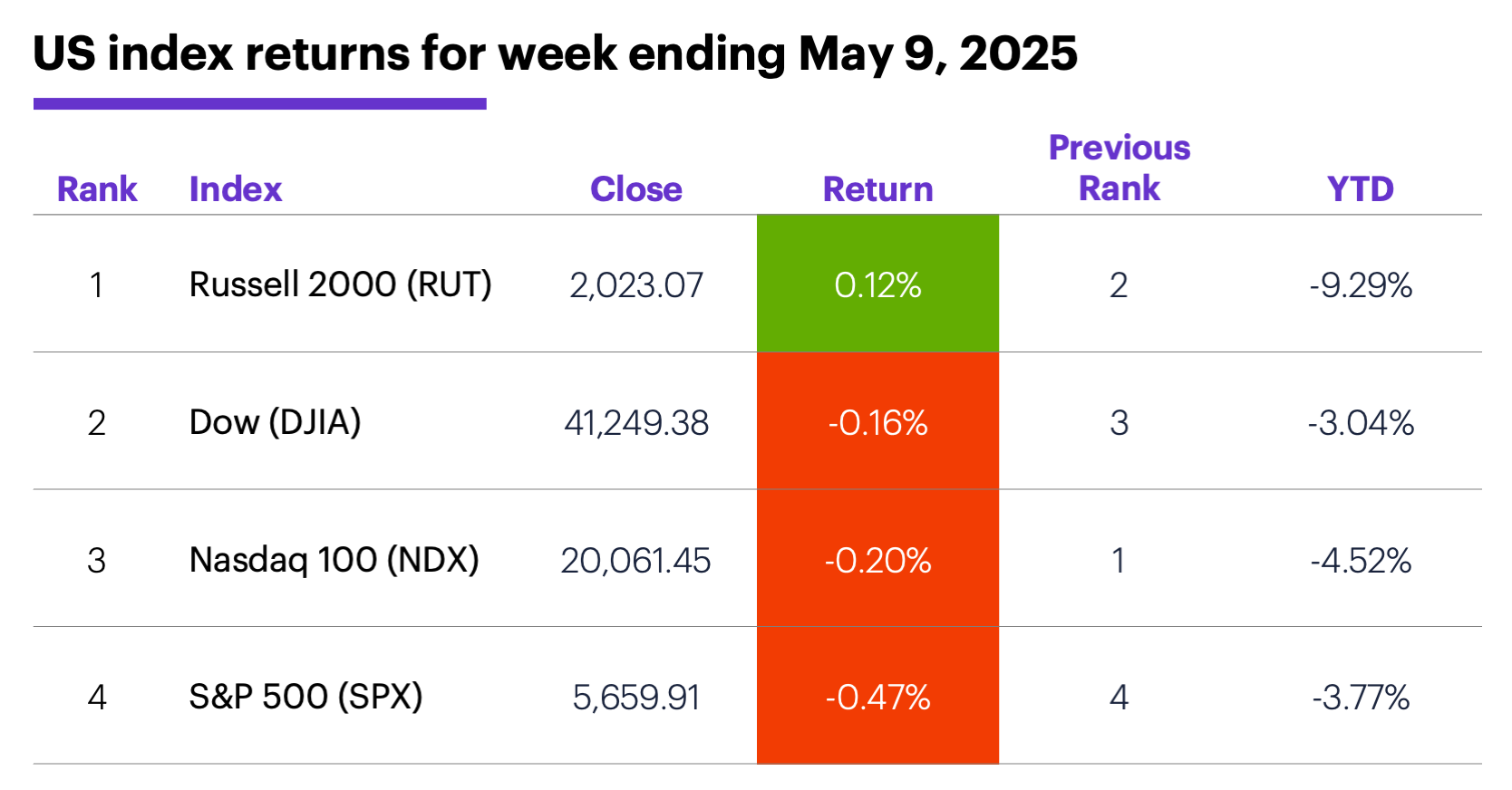

The headline: Stocks snap two-week win streak.

The fine print: As expected, the Fed held interest rates steady last Wednesday, and continued to reinforce its “waiting for clarity” stance on tariffs and the economy. And while their statement acknowledged elevated risks to employment and inflation, Fed Chair Jerome Powell also noted the US economy is currently in a good place.

The number: 70%, the percentage of the globally traded liquid natural gas (LNG) that will be consumed by Asia by 2030, according to Morgan Stanley & Co. analysts. The strategists think US gas exports could “transform” the Asia-Pacific region’s energy consumption the way the oil shale boom did in North America last decade, with potentially significant implications for investor portfolios.1

The scorecard: The Russell 2000 (RUT) was the only index to close higher last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were industrials (+1.1%), consumer discretionary (+1%), and utilities (+0.6%). The weakest sectors were health care (-4.2%), communication services (-2.3%), and consumer staples (-0.9%).

Stock moves: Groupon (GRPN) +43% to $24.21 and Sezzle (SEZL) +42% to $74.98, both on Thursday. On the downside, Cantor Equity Partners (CEP) -28% to $33.90 on Monday, Pra Group (PRAA) -29% to $13.57 on Tuesday.

Yields: The benchmark 10-year Treasury yield rose 0.06% to 4.37%.

US dollar: The US Dollar Index (DXY) extended its modest climb off April’s lows, ending the week up 0.39 at 100.42.

Futures: June gold (GCM5) closed at a new record high of $3,441.80 last Wednesday, then pulled back to end the week up $90.70 at $3,334. June WTI crude oil (CLM5) started last week by closing at a contract-low $57.23, but rebounded to end the week $2.73 higher at $61.02. Biggest up moves: May ether (ETHK5) +26.8%, May bitcoin (MBTK5) +6.4%. Biggest down moves: July orange juice (OJN5) -10.3%, May pork cutout (PRKK5) -4.5%.

Coming this week

Inflation data and retail sales highlight this week’s economic calendar, but traders will also be watching to see how—or if—the markets react to Friday’s consumer sentiment number:

●Tuesday: NFIB Business Optimism Index, consumer price index (CPI)

●Thursday: producer price index (PPI), retail sales, Philadelphia Fed Manufacturing Survey, Empire State Manufacturing Survey, industrial production, business inventories

●Friday: housing starts and building permits, import and export prices, consumer sentiment (prelim)

This week’s earnings include:

●Monday: Apogee Therapeutics (APGE), Monday.com (MNDY), Davita (DVA), Nuscale Power (SMR), Simon Property Group (SPG)

●Tuesday: Honda (HMC), On Holdings (ONON), Silicon Laboratories (SLAB), Grail (GRAL), Oklo (OKLO)

●Wednesday: CoreWeave (CRWV), Dynatrace (DT), Cisco (CSCO), USA Rare Earth (USAR)

●Thursday: Alibaba (BABA), Dillard's (DDS), Deere & Co. (DE), Walmart (WMT), Applied Materials (AMAT), Copart (CPRT), Doximity (DOCS)

●Friday: Flowers Foods (FLO)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

So far, May flowers

As of Friday, the SPX was up x.x% for the month—a move that’s slightly out of step with the market’s track record of early-May weakness. Whether it can sustain those gains through the end of the month will likely depend on how the tariff negotiations progress, and whether economic data reinforces or alleviates concerns about recession or stagflation. But May’s early strength does align with a few other historical patterns.

For example, the SPX closed up the month after three-month losing streaks 65% of the time since 1957. It also rallied four of six times the month after a month that, like April, made a 14-month (or longer) low but closed in the upper third of the month’s range.

The Cboe Volatility Index (VIX) offers another perspective. After the 19 other times since 2004 that the VIX hit its highest high in at least two months, while opening in the bottom half of the month’s range and closing in the bottom 25% (as it did in April), the SPX closed higher the following month 16 times.2

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Natural Gas: Fueling the Decade, Powered by AI. 5/6/25.

2 All figures reflect S&P 500 (SPX) and Cboe Volatility Index (VIX) monthly prices, 2004-2025. Supporting document available upon request.