Stock rally spills into June

- Tech strength and labor market resilience fuel gains

- Job creation down, but not as much as expected

- This week: inflation (CPI and PPI), US-China trade talks

A possible takeaway from last week: For now, investors appear comfortable with the idea of a slowing economy, as long as it doesn’t slow too much.

US stocks shrugged off a steady stream of soft economic data in the run-up to Friday’s key jobs report—which, although it showed a drop in job creation in May (along with a downward revision of April’s total), wasn’t as weak as analysts had expected. The S&P 500 (SPX) ended the day as high as it’s been since three days after its February 19 record high:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Jobs surprise keys weekly gain.

The fine print: Friday’s rally may have locked in a positive week for the SPX, but Tuesday’s tech-fueled rally also played a big role, and chip stocks were at the center of the move. The Philadelphia Semiconductor Index (SOX) climbed 2.7%, highlighted by Nvidia’s (NVDA) 3.1% gain.

The number: 49.9, the ISM Services Index reading reported last Wednesday—below expectations and the fourth-lowest reading of the past five years. The ISM Manufacturing Index, construction spending, and factory orders also came in weaker than expected last week.

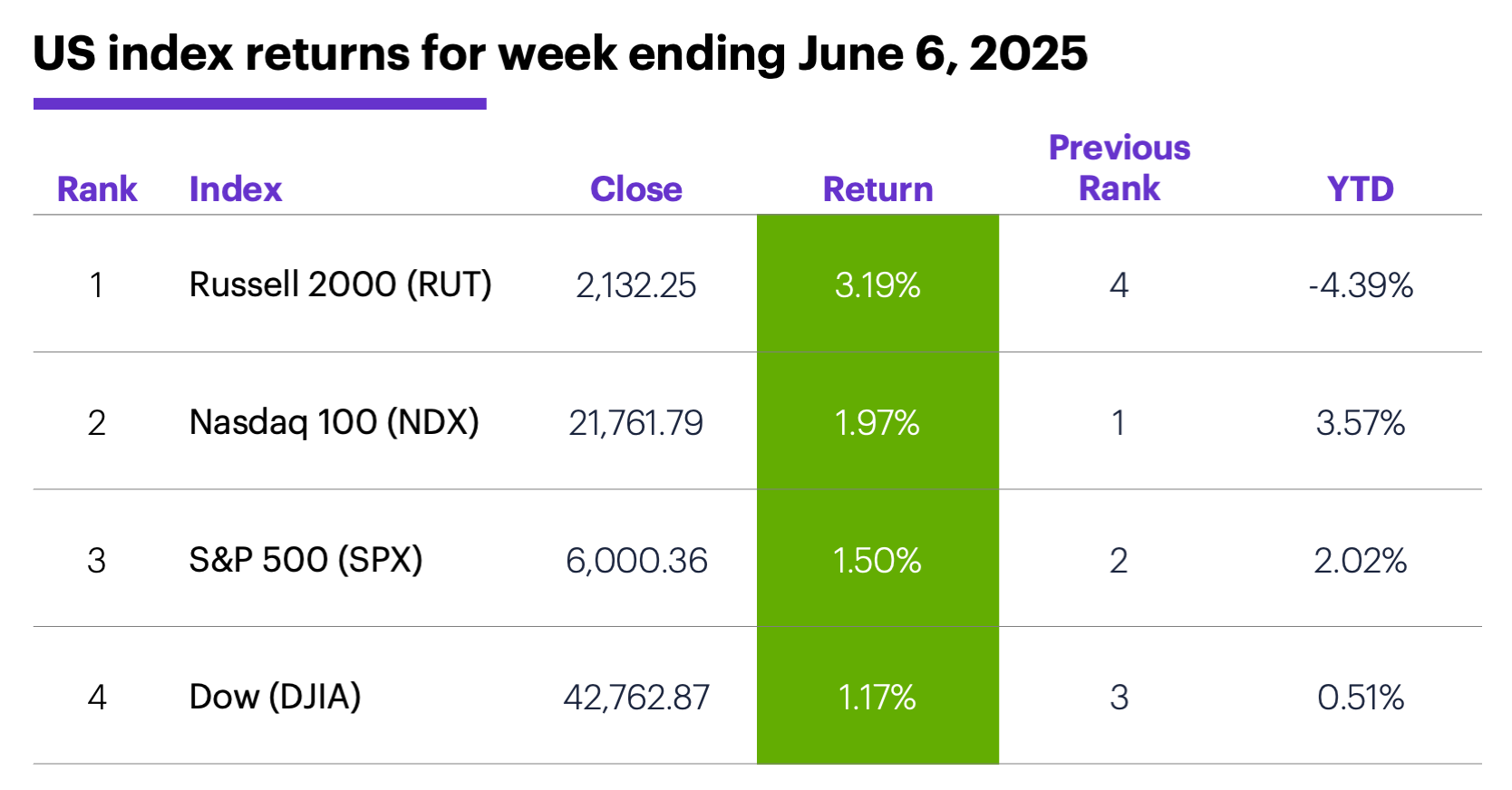

The scorecard: The Russell 2000 (RUT) small-cap index led the market comfortably last week, although it still ended it as the only major index in the red for the year:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were communication services (+3.2%), information technology (+3%), and energy (+2.2%). The weakest sectors were consumer staples (-1.6%), utilities (-1.1%), and consumer discretionary (-0.6%).

Stock moves: Vera Therapeutics (VERA) + 67% to $31.74 and Kymera Therapeutics (KYMR) + 46% to $43.13, both on Monday. On the downside, Vera Therapeutics (VERA) -26% to $22.70 and Lululemon (LULU) -20% to $265.27, both on Friday.

Yields: The benchmark 10-year Treasury yield fell to a four-week low of 4.36% last Wednesday, but jumped Friday to end the week up 0.12% at 4.51%.

US dollar: The US Dollar Index (DXY) fell close to the three-year low it hit in April last Thursday, but its Friday rally left it down only 0.14 at 99.19.

Futures: July WTI crude oil (CLN5) ended last week up $3.79 at $64.58, testing resistance at the top of its two-month trading range. August gold (GCQ5) jumped nearly 3% last Monday, then drifted lower to end the week up $31.20 at $3,346.60. Biggest up moves: July platinum (PLN5) +10.9%, September palladium (PAU5) +9.9%. Biggest down moves: June VIX (VXM5) -6.8%, July ethanol (ZKN5) -4.3%.

Coming this week

Inflation takes center stage this week:

●Monday: Wholesale Inventories, NY Fed Consumer Inflation Expectations

●Tuesday: NFIB Business Optimism Index

●Wednesday: Consumer Price Index (CPI)

●Thursday: Producer Price Index (PPI)

●Friday: Michigan Consumer Sentiment (preliminary)

This week’s earnings include:

●Monday: Casey’s General Stores (CASY), Limoneira (LMNR), Oracle (ORCL), Rent The Runway (RENT), Skillsoft (SKIL)

●Tuesday: Designer Brands (DBI), Dave & Buster's (PLAY), Children's Place (PLCE), J.M. Smucker (SJM), Gitlab (GTLB), United Natural Foods (UNFI)

●Wednesday: J.Jill (JILL), Korn Ferry (KFY), Oxford Industries (OXM), RH (RH)

●Thursday: Adobe (ADBE)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Fueling the energy story

With AI adoption ramping up, discussions about energy demand—specifically, the power needs of AI datacenters—have (re)gained traction. While much of the focus over the past several months has been on nuclear power, Morgan Stanley & Co. researchers pointed out that expected demand will require drawing on a wide range of energy sources—including fossil fuels, and especially natural gas.

While natural gas prices have been mostly rangebound the past couple of months, Morgan Stanley & Co. research suggests supply is not on track to keep pace with demand growth, and uncertainty in the crude oil market could contribute to that tightness.1 That could have implications for natural gas prices, natural gas stocks, and the overall energy sector—which, although it was the third-strongest last week, is still the second-weakest for the year.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Softer Oil, Stronger Gas. 6/3/25.