Market wraps up milestone May

- Stocks ride another tariff pause to weekly gain

- Real estate sector leads, energy slips

- This week: jobs report, manufacturing and services

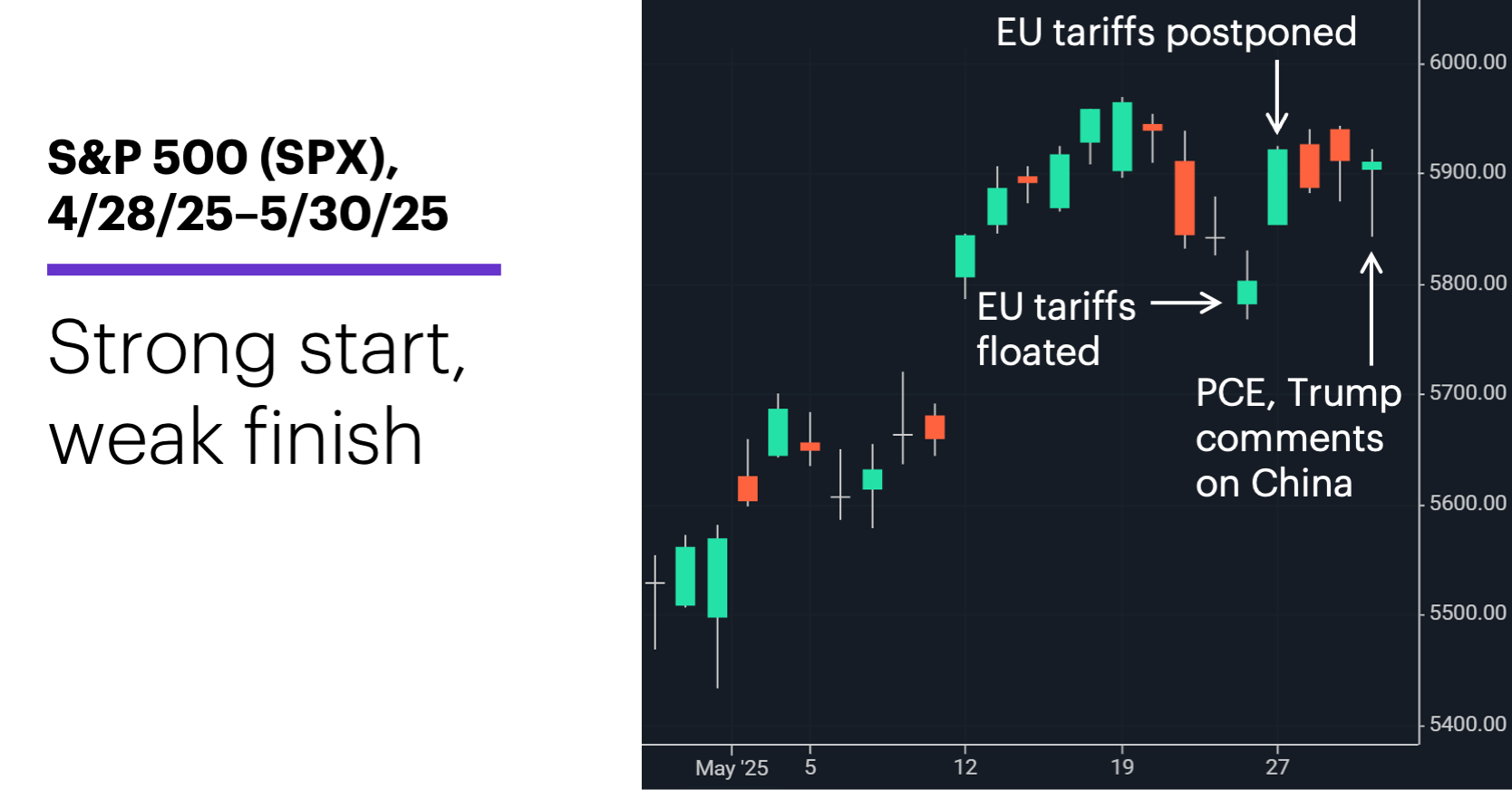

US stocks closed out their strongest May since 1990 with an up week, with tariffs once again fueling momentum—on both sides of the market.

The S&P 500 (SPX) started last week with its second-largest up day of the month as the White House said it would delay the tariffs on the European Union that it had announced the previous Friday. But a brewing court battle over the constitutionality of the tariff campaign weighed on the market later in the week, which ended with a volatile Friday in the wake of President Trump’s claim that China had violated its trade agreement:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Cautious end to “risk-on” month.

The fine print: While trade concerns appeared to ease throughout most of May, last week’s developments were a reminder that tariff uncertainty was still a factor in the markets. Morgan Stanley & Co. economists still think the US economy can avoid recession if there is de-escalation in trade tensions, although they believe high tariffs will likely “keep inflation firm, slow US GDP growth, and keep the Fed on hold into 2026.”1

The number: 2.5%, in-line year-over-year inflation reading from the core PCE Price Index. Traders will have to wait until next month to get a clearer picture of how tariffs have impacted the economy, although the record decline in imports and drop in consumer spending also reported on Friday may have provided a preview.

The move: NVIDIA (NVDA) gained 3.3% last Thursday after releasing earnings, but that represented just a little more than half of its early intraday gain of 6.4%. The stock slipped 2.9% on Friday.

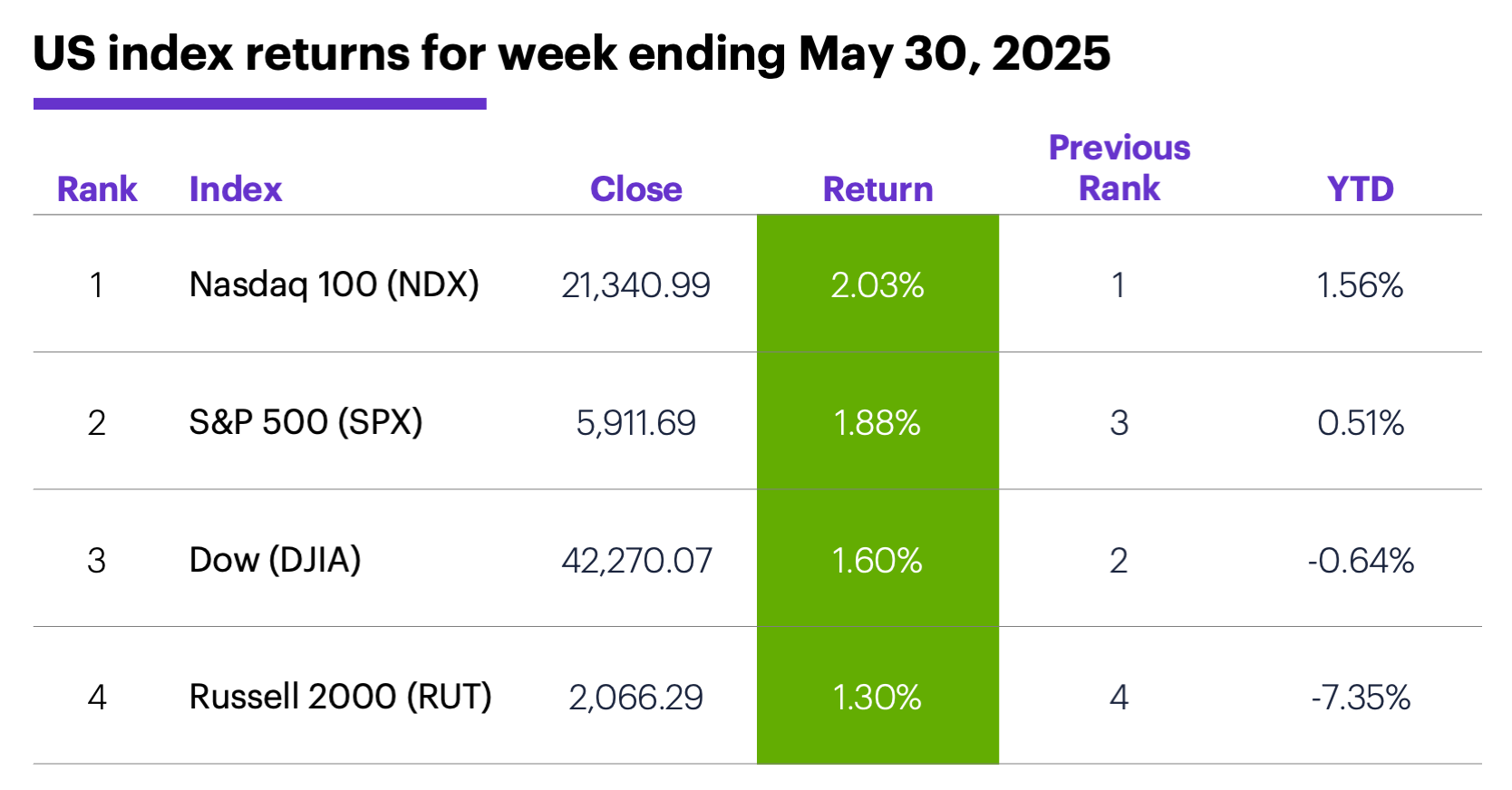

The scorecard: All the major indexes gained ground, but only the Nasdaq 100 (NDX) tech index and the SPX ended the week in positive territory for the year:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were real estate (+2.7%), tech (+2.4%), and communication services (+2.1%). The weakest sectors were energy (-0.4%), materials (+0.8%), and utilities (+1.1%).

Stock moves: Monro (MNRO) +31% to $16.75 on Wednesday, Claritev (CTEV) +'35% to $35.94 on Thursday. On the downside, NeuroPace (NPCE) -28% to $12.66 on Tuesday, Summit Therapeutics (SMMT) -31% to $18.22 on Friday.

Yields: The benchmark 10-year Treasury yield closed Friday down 0.12% at 4.39%.

US dollar: The US Dollar Index (DXY) rallied slightly, ending last week up 0.22 at 99.33.

Futures: August gold (GCM5) slipped $79.10 to $3,315.40 last week. July WTI crude oil (CLN5) continued to trade mostly sideways, ending the week down $0.74 to $60.79, toward the bottom of its recent range.

Coming this week

Jobs data dominates the economic calendar:

●Monday: S&P Global Manufacturing PMI, ISM Manufacturing Index, construction spending

●Tuesday: Job Openings and Labor Turnover Survey (JOLTS), factory orders, total vehicle sales

●Wednesday: ADP Employment Change, S&P Global Services PMI, ISM Services Index, Fed Beige Book

●Thursday: job cuts, balance of trade, productivity and labor costs

●Friday: Employment Report, used car prices

This week’s earnings include:

●Monday: Campbell's (CPB), Credo Technology (CRDO), Nordstrom (JWN), Science Applications (SAIC)

●Tuesday: CrowdStrike (CRWD), Dollar General (DG), Hewlett Packard Enterprise (HPE), HealthEquity (HQY), Land’s End (LE), Ollie's Bargain Outlet (OLLI), Thor Industries (THO), Victoria's Secret (VSCO)

●Wednesday: Dollar Tree (DLTR), Five Below (FIVE), GIII Apparel (GIII), MongoDB (MDB), PVH PVH), Rev Group (REVG), Verint Systems (VRNT)

●Thursday: Broadcom (AVGO), Braze (BRZE), Cracker Barrel (CBRL), Ciena (CIEN), DocuSign (DOCU), Lululemon (LULU)

●Friday: ABM Industries (ABM), Core & Main (CNM), Ferguson Enterprises (FERG)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Inside scoop on inside weeks

As choppy as last week’s trading may have seemed to some traders, the SPX’s volatility declined in a fundamental way—the index formed an “inside week” by trading entirely within the high-low range of the previous week (May 19-23). Many traders look for volatility to resume after such pauses.

Over the past 68 years, the SPX formed 79 other inside weeks similar to last week—that is, ones that occurred two weeks after the index hit its highest high in at least seven weeks. The market closed higher the next week more often than not (65% of the time), with an average return of 0.44%. But the market tended to be slightly less bullish after the subset of this group that, like last week, also followed a down week: The next week was positive 56% of the time, with an average gain of 0.09%.

But if last week was any indication, the tariff story will likely continue to drive short-term market momentum.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Still Slow Growth, Firm Inflation. 5/20/25.

2 All figures represent S&P 500 (SPX) weekly closing prices, 1956-2024. Supporting document available upon request.