Bulls get late-week pivot

- Small caps lead rebound from down week

- Oil falls to seven-week low, SpaceX launches

- This week: Fed rate decision, retail sales

Last week the market may have seemed to orbit solely around SpaceX, but in reality, the record-setting IPO was just one of many catalysts contributing to an eventful five days for stocks.

The S&P 500 (SPX) ran a gauntlet of geopolitical headlines, up-and-down oil prices, more tech-sector volatility, and stubborn inflation data to avoid posting back-to-back down weeks for the first time since March.

Last Wednesday the SPX set its lowest close since May 5—and was down 1.6% for the week—as oil futures jumped 3.5% amid new US military strikes on Iran. The index waffled early Thursday as President Trump pledged to “assume total control” of Iran’s oil and gas industries, but stormed to a 1.8% gain after he called off additional strikes. The market extended the bounce on Friday as SpaceX (SPCX) made its trading debut:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Choppy week for stocks resolves to the upside.

The fine print: While the Middle East may have lost some of its “shock factor” over the past couple of months, last week showed it could still impact sentiment, as evidenced by the stock market’s day-to-day (and sometimes, hour-to-hour) reactions to a constantly shifting geopolitical narrative and oil price swings that accompanied it. (Oil futures tumbled and stock index futures soared amid news of a US-Iran deal over the weekend.)

The move: SpaceX (SPCX) ended its first day of trading on Friday at $160.95—up 7.3% from its opening trade price of $150.05, and 19.2% above its initial allocation price of $135, which was also its intraday low. Shares traded as high as $176.52.

The number: 3.4%, the year-over-year increase in core PCE Price Index inflation expected by Morgan Stanley & Co. economists (due on June 25). While last week’s three-year-high Consumer Price Index (CPI) didn’t surprise them, increases in parts of the Producer Price Index (PPI) did. Overall, they note data indicates the Fed is more likely to focus on inflation risks than the labor market, implying higher-for-longer interest rates.1

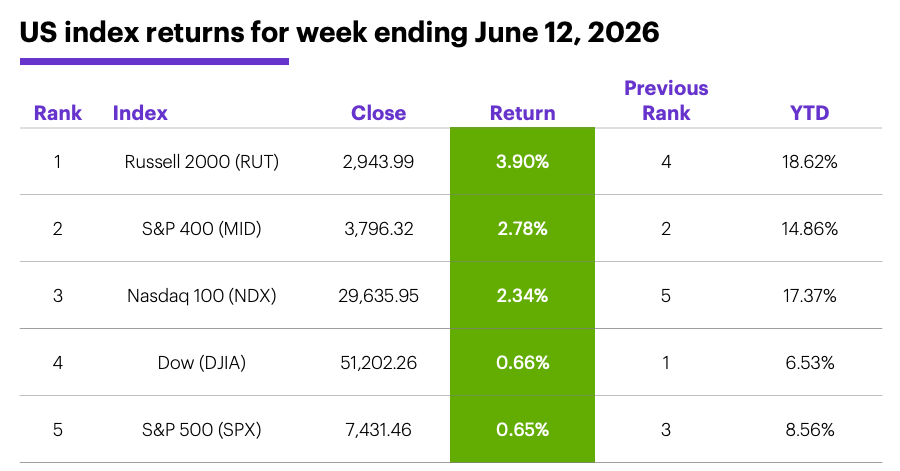

The scorecard: The Russell 2000 (RUT) small-cap index led US indexes last week, jumping back into first place for the year in the process:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were materials (+2.7%), consumer staples (+2.4%), and financials (+1.9%). The weakest sectors were communication services (-2.1%), energy (-0.5%), and utilities (+0.2%).

S&P 500 stock movers: The biggest gains last week KLA (KLAC) +31% to $253.44, Sandisk Corp (SNDK) +28% to $1982.85, Intel (INTC) +26% to $125.13. The biggest losses were Super Micro Computer (SMCI) -27% to $30.50, Adobe (ADBE) -20% to $204.71, PTC (PTC) -16.87% to $114.17. Other moves: Momentus (MNTS) +44% to $16.30 on Thursday (then -27% to $11.95 on Friday), Array Digital Infrastructure (AD) -23% to $40.11 on Thursday.

Yields and the dollar: The 10-year US Treasury yield fell 0.05% to 4.49% last week. The US Dollar Index (DXY) dropped 0.31 to 99.76, despite hitting its highest high (100.31) since March 31 last Thursday.

Commodity futures: August WTI crude oil (CLQ6) ended the week down $4.64 at $83.35—its lowest close since April 21. August gold (GCQ6) fell $126.50 to $4,238.80, despite a 3% rally on Friday. Biggest gains: September coffee (KCU6) +4.7%, July Lithium (LTHN6) +4.5%. Biggest declines: July WTI crude oil (CLN6) -6.9%, August Brent crude oil (BQ6) -6.8%.

Crypto: Bitcoin +4.3% to $63,543.20 last week, Ether +5.3% to $1,665.13.

Coming this week

It’s a short week—US markets will be closed Friday for Juneteenth—but retail sales and the first Fed meeting chaired by Kevin Warsh highlight a busy economic calendar:

●Monday: Empire State Manufacturing Index, Industrial Production and Capacity Utilization, NAHB-Wells Fargo Housing Market Index

●Tuesday: Housing Starts and Building Permits, Import Price Index

●Wednesday: Retail Sales, Business Inventories, Pending Home Sales, Fed interest rate decision

●Thursday: Philadelphia Fed Manufacturing Index, Leading Economic Indicators Index

●Friday: US markets closed for Juneteenth

This week’s earnings include:

●Monday: Dave and Buster’s (PLAY), RF Industries (RFIL)

●Tuesday: Korn Ferry (KFY)

●Wednesday: Jabil (JBL), CarMax (KMX)

●Thursday: Accenture (ACN), Kroger (KR),

This week’s IPOs include:

●Thursday: Kardigan (KARD), First Carolina Financial FCBM)

Volatility less volatile

After closing at a 19-week low the week ending May 29, then closing at a six-week high the week ending June 5, the Cboe Volatility Index (VIX) cooled off again last week. Although it hit an eight-week intraweek high, it ended the week lower, and also below its opening price. After 15 similar weeks since 1990, the SPX closed the next week higher nine times and lower six times (60%), with a 0.05% average return.

That marginal gain—even though there were three more winning weeks than losing weeks—was a function of the typical down week tending to be bigger than the typical up week. Of the six down weeks, five were declines in excess of -2%. In contrast, only two of the nine positive weeks were gains larger than +2%.2

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Reassessing risks to our Fed call after the latest data. 6/12/26

2 All figures reflect S&P 500 (SPX) and Cboe Volatility Index (VIX) weekly prices, 1990-2026. “Similar weeks” refers to a week the VIX closed at a six-week (or longer) close, followed by a week it closed at a six-week (or longer) high), followed by a week it closed lower and below its open. Supporting document available upon request.