Stocks take the high road

- Market bounces back despite latest tariff drama

- “Risk-on” sectors roll, energy slips as oil hits six-week low

- This week: inflation (CPI and PPI), retail sales

Tariffs filled the void left by an absence of high-profile economic data last week, triggering a flood of financial headlines but little in the way of market reaction.

The S&P 500 (SPX) rebounded from the previous week’s jobs-report sell-off, shrugging off the White House’s proposed 100% tariff on semiconductor chips to close Friday less than single point below its July 28 record close:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Market looks past tariff headlines.

The fine print: Last week may have been another sign that markets have become numb to tariff announcements and/or see them purely as a negotiating tool—i.e., threatened today, but potentially modified or cancelled tomorrow. The PHLX Semiconductor Index (SOXX) gained even more than the SPX last week (2.7%), while India’s Nifty 50 Index (NSEI) ended the week down less than 0.9% even though the tariff on Indian imports jumped from 25% to 50%.

The number: 226,000, the initial weekly jobless claim total reported last Thursday—higher than expected, but well below levels from May and June.

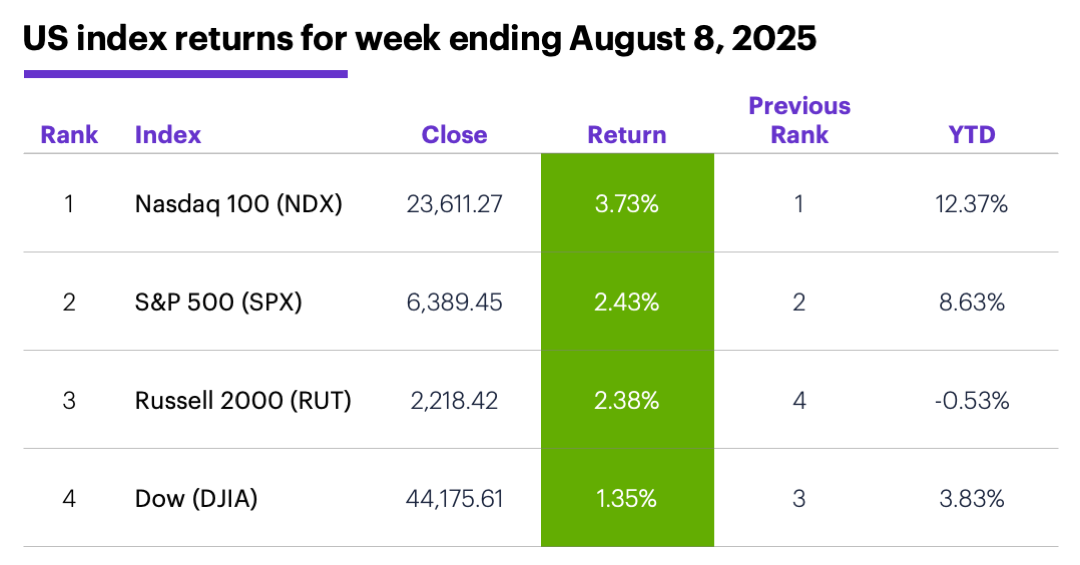

The scorecard: The Nasdaq 100 (NDX) tech index was last week’s biggest gainer:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were tech (+4.1%), consumer discretionary (+3.7%), and communication services (+3.2%). The weakest sectors were energy (-1.1%), health care (-0.8%), and real estate (-0.2%).

Stock moves: Astera Labs (ALAB) +29% to $174.39 on Wednesday, OptimizeRx (OPRX) +35% to $17.30 on Friday. On the downside, Vivid Seats (SEAT) -30% to $17.93 and Crocs (CROX) -29% to $74.39, both on Thursday.

Yields: Last Tuesday the 10-year Treasury yield fell to its lowest level since May 1, but ended the week up 0.07% at 4.28%.

US dollar: The US Dollar Index (DXY) fell 0.96 to 98.18 last week.

Futures: September WTI crude oil (CLU5) slid every day but Friday (when it was unchanged), falling $3.45 to $63.88 for the week. December gold (GCZ5) hit its highest intraday high since April last Friday, ending the week up $91.50 at $3,491.30. Biggest rallies: August ether (ETHQ5) +15.9%, December coffee (KCZ5) +9%. Biggest declines: September VIX (VXU5) -9.2%, September lumber (LBSU5) -6.2%.

Coming this week

The latest inflation numbers and retail sales highlight the economic calendar:

●Tuesday: consumer price index (CPI)

●Thursday: producer price index (PPI)

●Friday: retail sales, Empire State Manufacturing Index, industrial production and capacity utilization, consumer sentiment (preliminary), August options expiration

This week’s earnings include:

●Monday: Monday.com (MNDY), Oklo (OKLO), USA Rare Earth (USAR)

●Tuesday: CoreWeave (CRWV), Cisco (CSCO)

●Wednesday: Dillard's (DDS), Deere (DE), Brinker (EAT)

●Thursday: Advance Auto Parts (AAP), Applied Materials (AMAT), Sandisk (SNDK), Tapestry (TPR)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Spotlight on inflation

While the impact of tariffs on the economy has, so far, been less extreme than some analysts had expected, the weak August 1 jobs report may have fueled concerns that the effects are only now beginning to make their presence felt.

That’s going to shine an even brighter spotlight than usual on this week’s inflation data. Stock market bulls and bears will likely try to press their advantage in the event of a significant downside or upside surprise, respectively, from Tuesday’s CPI. An extremely hot reading could fuel concerns the Fed won’t cut rates at its September meeting. As of Friday, the market-based probability of a 0.25% cut was above 90%.1

Morgan Stanley & Co. analysts expect the CPI to show modestly rising inflation, driven mostly by price increases in core goods as a result of tariffs. While their base case is for most tariff-related price effects to materialize over the summer, they also believe risks are tilted toward a gradual, persistent upswing through the end of this year.2

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 CMEGroup.com. FedWatch. 8/8/25.

2 MorganStanley.com. CPI Preview: Tariffs continue to lift inflation. 8/7/25.