Bulls back off

- Indexes backtrack despite megacap strength

- Fed still cautious, jobs report misses widely

- This week: busiest week of earnings season, ISM Services Index

Last week was shaping up to be a big week for the markets, and it didn’t disappoint.

US stocks wrapped up a solid July last Thursday, but still posted their biggest weekly loss since May as mixed economic data appeared to reignite concerns about the longer-term impact of tariffs, offsetting potential tailwinds from strong big-tech earnings. The market also didn’t get much traction from the announcement of trade deals with the European Union and South Korea.

The S&P 500 (SPX) inched to a record close last Monday—and hit two more intraday records after that—but stepped back the final two days of the week amid a spate of new White House announcements (including a letter demanding US pharma companies lower drug prices) and a notable downside surprise from the monthly jobs report:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Bears take pivotal week.

The fine print: There were disconnects between some of the week’s headlines and the underlying stories. GDP topped expectations, but also revealed slowing consumer spending. Two Fed governors dissented from the FOMC’s decision to leave interest rates unchanged, but Chairman Powell downplayed the likelihood of a September rate cut (although that was before Friday’s jobs miss). On the other hand, the PCE Price Index simply showed inflation climbed last month.

The number: 73,000, the number of new jobs created in June—well below the 110,000 estimate. Also, the previous month’s total of 147,000 new jobs was slashed to 14,000. Hours after the jobs report came out on Friday, President Trump fired Bureau of Labor Statistics Commissioner Erika McEntarfer.

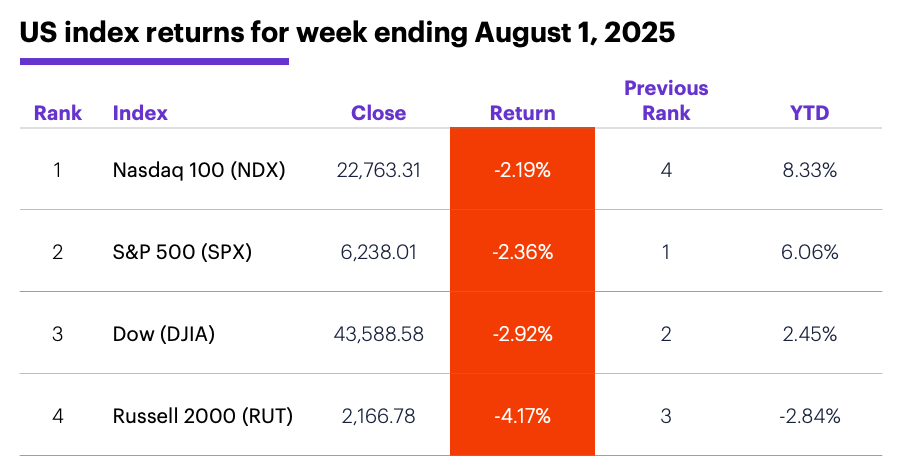

The scorecard: The Nasdaq 100 (NDX) tech index fell the least, while the Russell 2000 (RUT) small-cap index pulled back the most:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were utilities (+1.5%), communication services (+0.02%), and consumer staples (-1.1%). The weakest sectors were materials (-5.4%), consumer discretionary (-4.5%), and health care (-3.9%).

Stock moves: Celcuity (CELC) +167% to $36.79 on Monday, Newegg (NEGG) +44% to $56.19 on Tuesday. On the downside, Bakkt (BKKT) -42% to $10 on Tuesday, Fluor (FLR) -27% to $41.42 on Friday.

Yields: The 10-year Treasury yield tumbled Friday to its lowest close since June 30, ending the week down 0.17% at 4.21%.

US dollar: The US Dollar Index (DXY) also pulled back sharply on Friday, but still closed Friday up 1.49 for the week at 99.14.

Futures: September WTI crude oil (CLU5) closed Friday at $67.33, up $2.17 for the week. Thanks to a big Friday rally, December gold (GCZ5) ended last week up $7.30 at $3,399.80. Biggest rallies: August VIX (VXQ5) +11%, September WTI crude oil (CLU5) +3.3%. Biggest declines: September orange juice (OJU5) -27.1%, September copper (HGU5) -23.3%.

Coming this week

Earnings season hits high gear this week—more than 1,600 companies will release their numbers. A few highlights:

●Monday: Axsome Therapeutics (AXSM), BioNTech (BNTX), Anheuser-Busch InBev (BUD), WK Kellogg (KLG), Lattice Semiconductor (LSCC), ON Semiconductor (ON), Palantir (PLTR), Spirit AeroSystems (SPR), Tyson Foods (TSN), Wayfair (W), Williams Companies (WMB)

●Tuesday: Advanced Micro Devices (AMD), Arista Networks (ANET), Cirrus Logic (CRUS), Marathon Petroleum (MPC), Pfizer (PFE), Powell Industries (POWL), Silicon Laboratories (SLAB), Super Micro Computer (SMCI), Snap (SNAP), Sunoco (SUN), Molson Coors Beverage (TAP), Teradata (TDC), Yum Brands (YUM)

●Wednesday: Airbnb (ABNB), AppLovin (APP), DoorDash (DASH), Disney (DIS), Duolingo (DUOL), e.l.f. Beauty (ELF), Global Payments (GPN), Lyft (LYFT), McDonald’s (MCD), Occidental Petroleum (OXY), Roblox (RBLX), Shopify (SHOP), Uber Technologies (UBER)

●Thursday: ConocoPhillips (COP), Dropbox (DBX), Doximity (DOCS), Epam Systems (EPAM), Eli Lilly And (LLY), MP Materials (MP), Ralph Lauren (RL), SolarEdge Technologies (SEDG), Talen Energy (TLN), Trade Desk (TTD), Wynn Resorts (WYNN), Block (XYZ)

●Friday: Bayer AG (BAYRY), Mazda Motor (MZDAF), Tempus AI (TEM), Wendy's (WEN)

This week’s numbers include:

●Monday: factory orders

●Tuesday: trade balance, S&P Global Services PMI, ISM Services Index

●Thursday: productivity and labor costs, wholesale inventories, NY Fed consumer inflation expectations, consumer credit

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

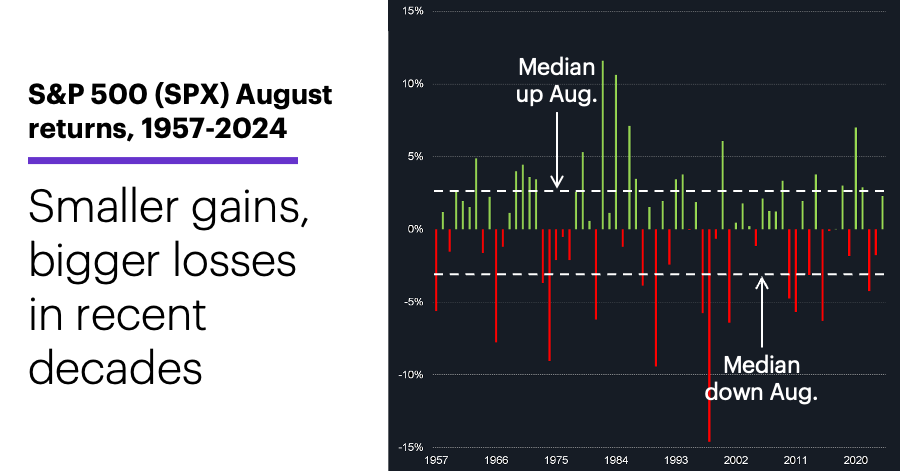

Dog days of August?

Since the SPX expanded to 500 stocks in 1957, August has never consistently been a stronger-than-average month for the US market. Overall, it’s been a positive month 29 times and a negative one 19 times:

Data source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index.)

In the most recent 34 years, though, it’s been noticeably softer. Since 1991, August was a positive month less often (19 of 34 years) than any other month but September, and the SPX’s 0.4% median August return was the third-lowest of all months.1

But this weakness wasn’t a matter of August being a down month more frequently than it used to be. In fact, there was only one more positive August between 1957-1990 than there was between 1991-2024. The difference? In the more recent window, August gains tended to be smaller and August losses tended to be larger.

From 1957-1990, the median positive August return was +3% and the median negative August was -2.9%. Since 1991, the median positive August return contracted to +2.1% while the median negative August increased to -3.1%.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 All figures reflect S&P 500 (SPX) monthly closing prices, 1957–2024. Supporting document available upon request.