Market takes spring break

E*TRADE from Morgan Stanley

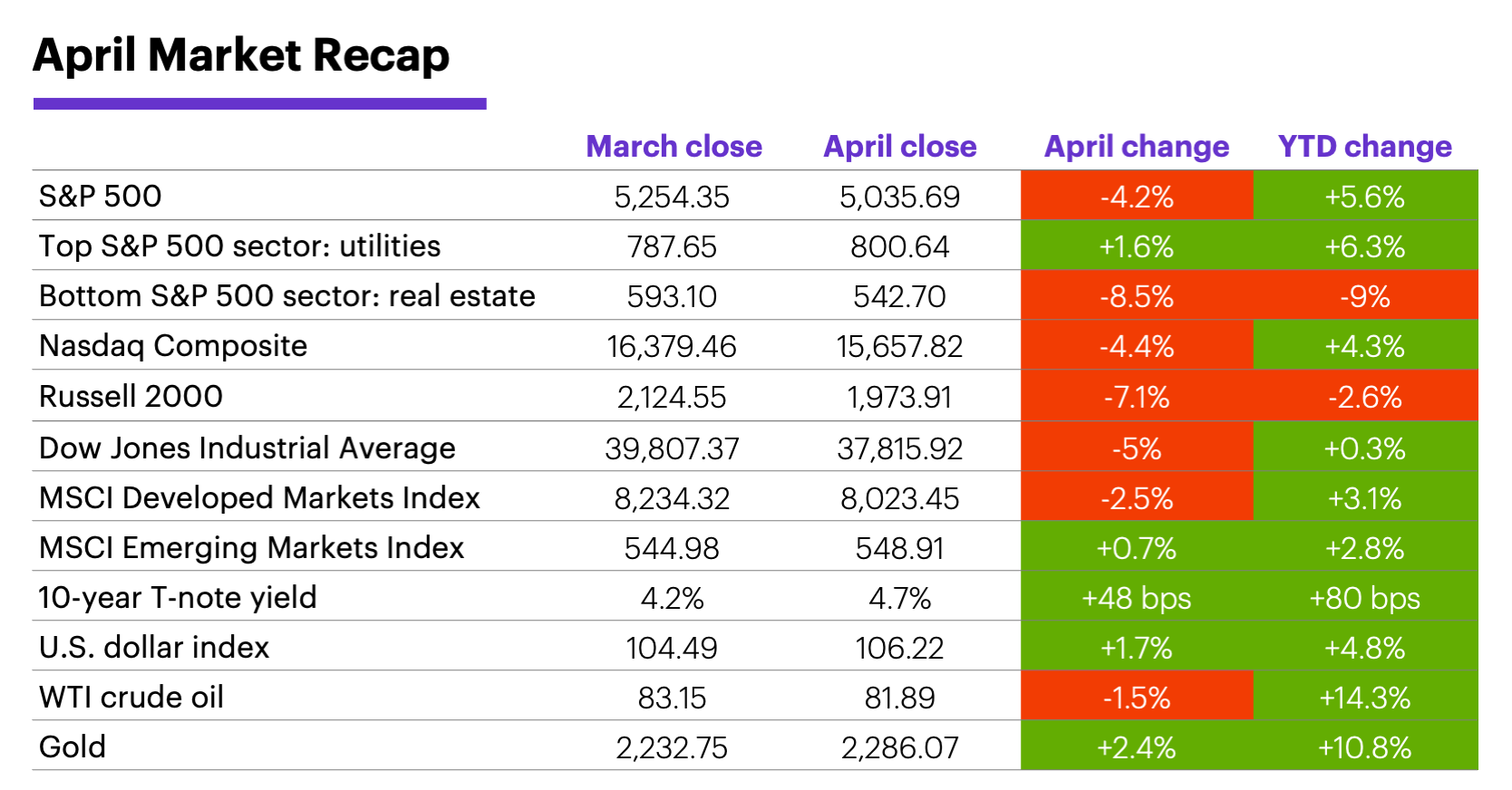

The stock market’s high-momentum rally off its October 2023 lows finally took a breather in April, as concerns over sticky inflation, rising interest rates, and geopolitical turmoil appeared to weigh on sentiment.

Despite logging its first negative month since October, though, the S&P 500 trimmed its losses toward the end of April as a solid start to Q1 reporting season got an extra boost from a few Big Tech earnings beats.

Small cap stocks continued to be a weak link in the equity chain. The Russell 2000 fell more than any other major US index in April, sliding back into negative territory for the year. Utilities were the strongest S&P 500 sector, while real estate was the weakest, ending April as the only one in negative territory for the year.

International stocks mostly outperformed the US, as the MSCI Developed Markets Index fell less than the S&P 500, while the MSCI Emerging Markets Index posted a small gain for the month.

Bond prices fell in April as yields pushed to their highest levels since mid-November. The benchmark 10-year Treasury yield ended April 48 basis points higher at 4.7%—its biggest monthly increase since September.

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment).

The Federal Reserve kicked off May by leaving interest rates unchanged, as expected, after a third month of higher-than-expected inflation data. Despite concerns that stubborn inflation and a potentially overheating economy could prompt the Fed to leave rates unchanged this year—or even hike them—Morgan Stanley & Co.’s baseline case is for a first cut in July, followed by two more by the end of the year.

That outlook reflects the analysts’ belief that the economy is not so much overheating as it is expanding, in large part because of immigration that was more than four times the expected rate in 2023 (3.3 million vs. 800,000), and which is expected to run at a similar level this year.1 In their view, for example, higher-than-forecasted payroll numbers represent a bigger labor market for which such readings are the norm, not a tighter labor market that threatens to fuel inflation because of accelerating wage growth.

This scenario also suggests long-run inflation expectations will likely reset upward by 0.4%-0.6%, according to Morgan Stanley Wealth Management. That, they note, is an environment in which investors should favor real assets that track inflation dynamics, such as infrastructure, select real estate, and commodities. But US small-cap stocks, in particular, could continue to struggle.2

Commodities did, in fact, extend their rally in April, although with different markets in the driver’s seat than in past months. While gold rallied to fresh record highs above $2,400 in April before pulling back, US crude oil prices ended a volatile month with a small loss. But strong rallies in markets ranging from wheat, rice, coffee, and copper helped propel some commodity indexes to their highest levels in more than a decade.

Since 1990, May has been a positive month for the S&P 500 73% of the time, although weaker Mays have sometimes followed negative Aprils.

Insight of the month: The AI story’s overlooked theme. Morgan Stanley & Co. analysts estimate that in 2027, datacenter power consumption from Generative AI will equal 80% of the consumption from all data centers in 2022. That suggests significant opportunities in the “picks and shovels” of the AI revolution—companies that provide key solutions such as datacenter infrastructure management software, connected equipment, racks, switchgears, and last but not least, cooling.3

Market calendar. May’s reputation as one of the weaker months of the year doesn’t have much of a basis in reality, especially over the past few decades. Since 1990, the S&P 500 had a positive May return 73% of the time, second only to April and December.4

The caveat: Weaker-than-average Aprils have more often than not been followed by weaker-than-average Mays. Since 1957, the S&P 500’s median May return after positive Aprils was 1.2%. Following negative Aprils, the median May return dropped to -0.1%, and after the five other times the April loss was -4% or more, May’s median return was -1.9%.4

1 MorganStanley.com. U.S. Economy: Bigger, But Not Tighter. 4/23/24.

2 MorganStanley.com. GIC Tactical Asset Allocation Changes: Reflation Calls for Real Assets. 4/18/24.

3 MorganStanley.com. A Central Piece of the GenAI Puzzle. 4/18/22.

4 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2024. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.