Market sidesteps winter chill

E*TRADE from Morgan Stanley

The US stock market continued its push into record territory in February, as bulls appeared to focus on the economic potential of artificial intelligence (AI) and the prospect of rate cuts, despite some inflation data that appeared to temporarily raise concerns about how soon the Federal Reserve may act.

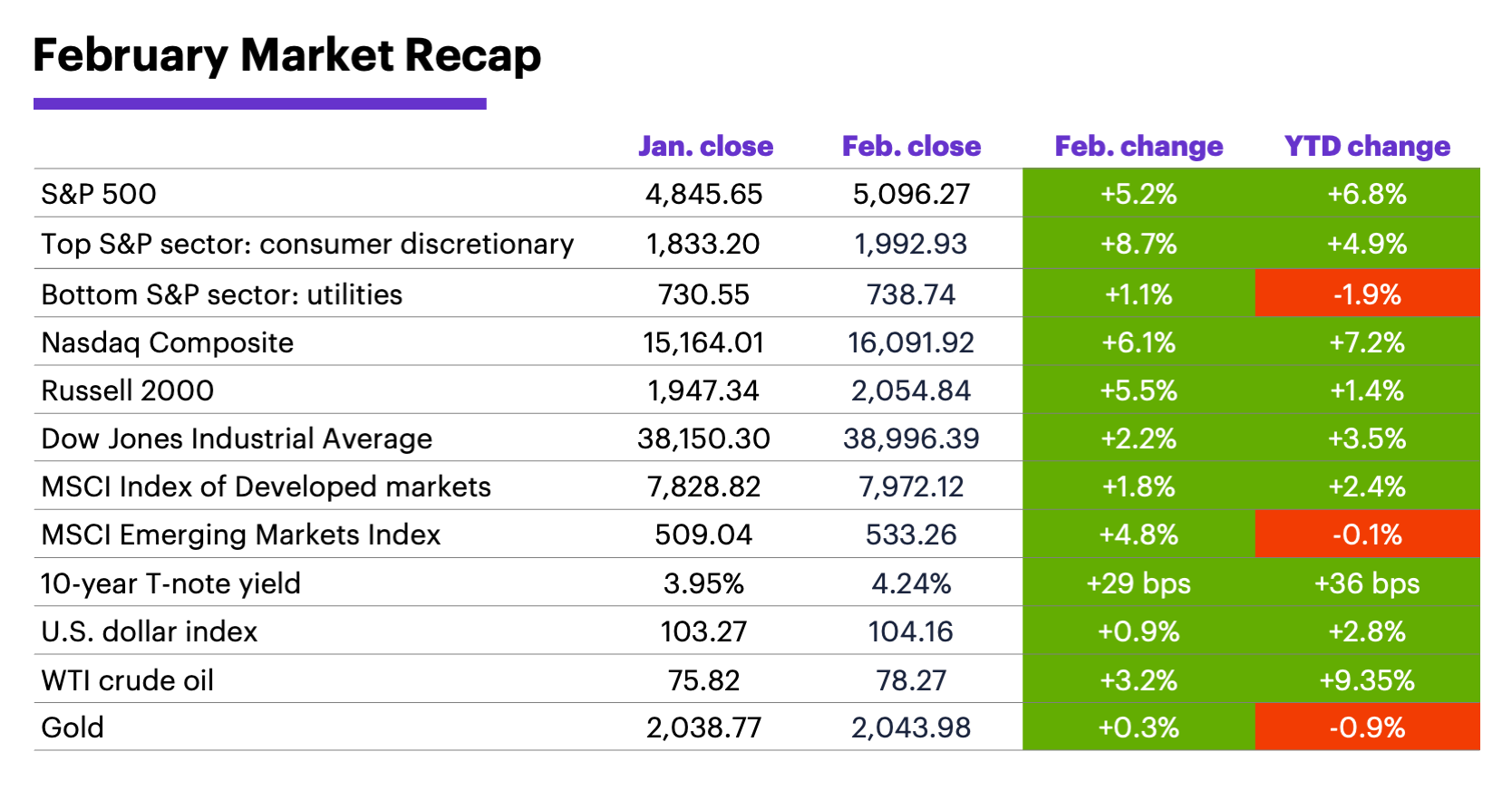

Last month the S&P 500 traded above 5,000 for the first time, posted its fourth-consecutive up month, and logged its second-largest February return of the past 25 years. The tech-heavy Nasdaq Composite ended February with its first record high since 2021.

Bond prices went the other direction as yields climbed, with the benchmark 10-year Treasury yield ending February closer to a three-month high than the nearly six-month low it hit to start the month.

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment).

Two developments last month highlighted the dominance of longstanding market themes. First, stocks stumbled—and bond yields jumped—mid-month when higher-than-expected inflation data from the Consumer Price Index (CPI) and Producer Price Index (PPI) renewed speculation the Fed may delay cutting interest rates. But those concerns appeared to ease somewhat on the final day of the month after the release of a more moderate reading from the PCE Price Index, the Fed’s preferred inflation gauge.

Second, AI returned to center stage as chipmaker Nvidia released earnings, which topped estimates by a wide margin and were followed by the biggest up day in more than a year for both the S&P 500 and tech-centric Nasdaq Composite. Those moves also served as a reminder of how a handful of stocks have continued to drive the majority of gains in what Morgan Stanley & Co. strategists describe as a “historically narrow” market.1

Despite some “sticky” inflation numbers, other data didn’t necessarily suggest the economy was overheating. Retail sales and durable goods orders were among the higher-profile reports that came in weaker than expected last month, and Q4 GDP was revised slightly lower.

The S&P 500’s 6.8% year-to-date return through the end of February was one of its strongest starts to a year since 1999.

For now, the Fed is still poised to cut rates in June, according to Morgan Stanley & Co. strategists, who think slower economic growth will prevail over time, ultimately leading to 100 basis points (1%) of cuts this year.2 While the odds of a May rate cut dropped below 50% in the aftermath of the hot February 13 CPI report, the odds of a June cut climbed above 50% immediately after the February 29 PCE Price Index release.3

Insight of the month. With valuations of non-US equities recently reaching a 20-year low vs. the S&P 500,4 Morgan Stanley Wealth Management noted there may be benefits to gaining exposure to Japan and Europe, as well as emerging markets (including Brazil, Mexico, and India), which rebounded last month after a weak January.

Market calendar. The S&P 500’s 6.8% year-to-date return through the end of February was its third-strongest start to a year since 1999.5 While many market watchers have, understandably, been waiting for the current rally to cool, the S&P has more often than not followed a larger-than-average January-February return with a relatively strong March: When the S&P’s January-February gain was positive but less than 5%, its median March return was 1%. When it rallied 5% or more in the first two months of the year, its median March return was 2.5%.

1 MorganStanley.com. The Gap Between Corporate Haves and Have-Nots. 2/26/24.

2 MorganStanley.com. An Atlantic-sized Divide in Monetary Policy. 2/21/24.

3 CMEGroup.com. FedWatch Tool. 2/29/24.

4 MorganStanley.com. The GIC Weekly: US “Policy Exceptionalism.” 2/26/24.

5 Figures reflect S&P 500 (SPX) monthly closing prices, 1/2/57–2/29/24. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.