Market rides tech into summer

E*TRADE from Morgan Stanley

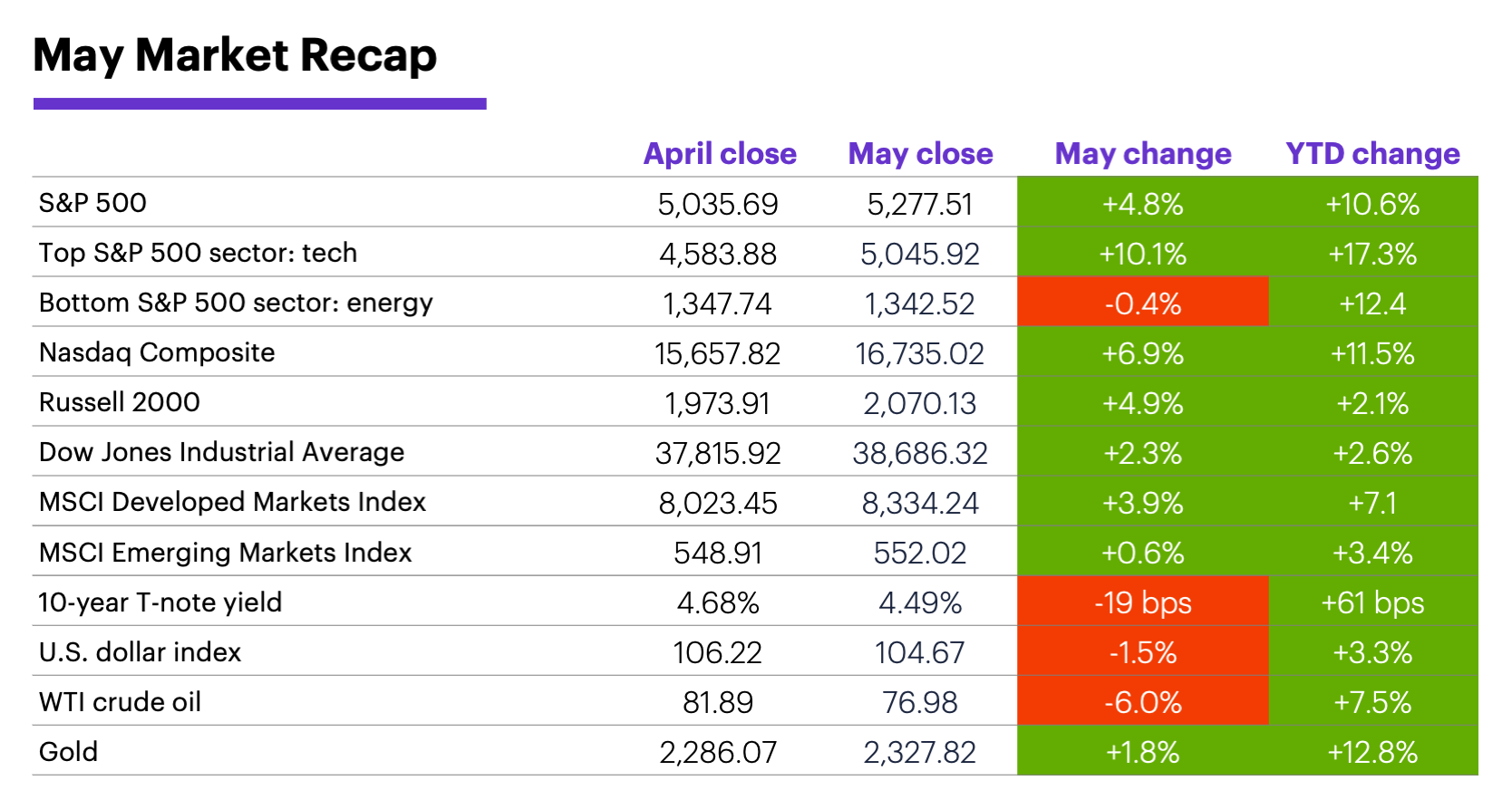

Heading into mid-year, most US stock indexes have found themselves sitting on larger-than-average returns for the year, thanks in no small part to a stronger-than-average May—even if the market lost some momentum late in the month.

While it would be logical to assume May’s push to record highs was mostly fueled by optimism about potential rate cuts in the wake of cooler inflation data, the market actually racked up most of its gains before the highest-profile of those numbers hit the Street.

The S&P 500 was up 3.7% for the month on May 13—one day before the Producer Price Index (PPI) was released, and two days before the Consumer Price Index (CPI)—and it gained only an additional 1.9% by May 21 before drifting mostly lower the remainder of the month. Nonetheless, the S&P 500’s 4.8% net return for the month made it the third-strongest May of the past 20 years, and the seventh-strongest since 1957.

Data source: Power E*TRADE and FactSet. (For illustrative purposes. Not a recommendation. It is not possible to invest directly in an index.) Note: crude oil, gold, and U.S. Dollar Index data reflect spot-market prices. BPS (basis point) = 0.01%. MSCI Index of Developed Markets and MSCI Emerging Markets Index represent “total-return” performance (index change including dividend reinvestment).

Tech played the starring role in May’s rally. Technology was the strongest S&P 500 sector in May, and the tech-heavy Nasdaq Composite was the month’s top-performing US index. Tech owed a great deal of its strength to the semiconductor space—most notably AI chipmaker Nvidia, which broke out to fresh record highs toward the end of the month.

But Morgan Stanley & Co. strategists point out the market’s reliance on a few increasingly correlated megacap stocks is not without risk, even if Nvidia and other high-profile tech leaders have strong businesses and growth prospects. Toward the end of 2023, for example, 10 stocks accounted for more than a third of the market’s total capitalization, and as the analysts noted, history has shown such a condition is “rarely sustainable.”1

Although the inflation downticks reported last month raised hopes for rate cuts this year, higher-for-longer rates remained a concern. Rising yields appeared to weigh on stocks in the latter part of May, although they eased a bit on the final day of the month when the Fed’s preferred inflation gauge, the PCE Price Index, didn’t surprise to the upside. After falling to a six-week low in mid-May, on May 29 the benchmark 10-year Treasury yield closed at its highest level since the end of April, and it ended the month down only 19 basis points at 4.49%.

Historically, June has been one of the weaker months for stocks, although it has bucked that trend over the past decade or so.

But Morgan Stanley & Co. strategists expect disinflation to continue as the year progresses,2 and their baseline forecast is for the Fed to first cut rates in September.3 That said, hawkish comments from Fed officials as recently as last week suggest the central bank still perceives its greatest risk as cutting rates too soon or too much.

Commodities continued to rally even though oil prices dropped for a second-straight month. Orange juice, wheat, silver, and natural gas were among the markets with double-digit percentage gains in May.

Insight of the month: Investing for “perfection.” With stock valuations as high as they’ve been since 2021, markets are “priced for perfection,” according to Morgan Stanley Wealth Management analysts. In this environment, the strategists have “little interest in taking on duration in either stocks or bonds,” and suggest investors focus on quality cash flows and earnings achievability—and perhaps incorporate cheap “insurance,” such as Cboe Volatility Index (VIX) calls or S&P 500 puts.4

Looking ahead to June. The S&P 500’s average June return since 1957 is an uninspiring 0%, with 36 gains vs. 31 losses. And while June has been a positive month more frequently since 1990 (20 out of 34 years, including eight of the past 10), its average return during this period was -0.1%, thanks to several larger-than-average losses, including in 2022 and 2008.5

Key dates: Jobs report (6/7), Fed interest rate announcement (6/12), CPI (6/12), PPI (6/13), Retail Sales (6/18), Housing Starts (6/20), quarterly expiration (6/21), presidential debate (6/27), PCE Price Index (6/28).

1 MorganStanley.com. What if Rates are Higher for Longer? 5/6/24.

2 MorganStanley.com. Midyear Economic Outlook: Reasons for Optimism. 5/20/24.

3 MorganStanley.com. Midyear U.S. Economic Outlook: Continued Resilience. 5/22/24.

4 The GIC Weekly: Valuations Don’t Matter Until They Do. 5/28/24.

5 Figures reflect S&P 500 (SPX) monthly closing prices, 1957–2023. Supporting document available upon request.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.