Market Dashboard

New every Monday with last week’s recap and notes on the week ahead.

Last update: 08/03/2026

Stocks rebounded on renewed artificial intelligence optimism last week, even as semiconductors lagged. The Federal Reserve held rates steady. Short-term Treasury yields fell while longer-term yields rose. Oil and bitcoin fell while gold hovered and the dollar was steady. Data showed cooler inflation and slower growth, but steady consumer spending.

Stocks rebound as AI optimism returns

- U.S. stocks rose over the week as confidence in artificial intelligence (AI) improved.

- The S&P 500 Index gained 1.1% to 7,490, about 1.6% below its June record.

- The Nasdaq Composite Index advanced 1.6%.

- The small-cap Russell 2000 Index rose 0.1%.

- The Magnificent Seven index jumped 4.2%, but chip stocks lagged, with the Philadelphia Semiconductor Index declining 4.3%.

- Market gains were less broad: The equal-weighted S&P 500 rose 0.6%, lagging the cap-weighted index.

- Market stress cooled, with the Chicago Board Options Exchange Volatility Index (VIX), known as the stock market’s “fear gauge,” easing to about 16 by week’s end after topping 20 midweek.

July ends mixed as semiconductors drag

- July performance was uneven as AI-related weakness and technical pressures weighed on markets.

- The S&P 500 fell 0.1% for the month, while the Nasdaq Composite fell 3.2% and the Russell 2000 fell 3.1%.

- Semiconductors faced notable pressure. The Philadelphia Semiconductor Index fell 20.6% for the month.

- The equal-weighted S&P 500 rose 0.9% in July as investors rotated more defensively.

Commodities and crypto soften; dollar steadies

- Brent crude oil fell over the week to $90 per barrel.

- Gold hovered around $4,000 per ounce.

- Bitcoin fell to around $63,000.

- The U.S. Dollar Index was range-bound, with little net change.

Fed holds rates but signals hawkish tilt

- The Federal Reserve kept the federal funds target range at 3.50%–3.75%.

- Three Fed Presidents dissented for a 25-basis-point hike, reinforcing concerns about inflation risks.

- Fed Chair Warsh offered little pushback on the possibility of a rate hike, adding to hawkish perceptions.

- Limited forward guidance increased uncertainty about near-term policy.

- Fed funds futures implied more than a 60% chance of a 25 basis point hike at the September Federal Open Market Committee meeting.

Yield curve steepens as long rates jump

- The U.S. Treasury yield curve steepened over the week.

- The two-year Treasury yield fell 4 basis points over the week to 4.29%, while the 10-year Treasury yield rose 3 basis points to 4.73%, the highest since January 2025.

- The 30-year Treasury yield rose 11 basis points to 5.27%, the highest since 2007.

- Markets priced lower near-term inflation: The one-year U.S. inflation swap rate ended the week at 1.92%, the lowest since 2024.

Earnings beat rates stay strong on AI

- Second-quarter earnings continued to come in above expectations.

- Of the 61% of S&P 500 companies reporting, 86% beat earnings per share expectations and 77% beat sales expectations.

- Hyperscaler results suggested continued growth and margin expansion despite capacity constraints, easing concerns about returns on AI capital spending.

Investment holds up as inflation cools

- Economic data were mixed.

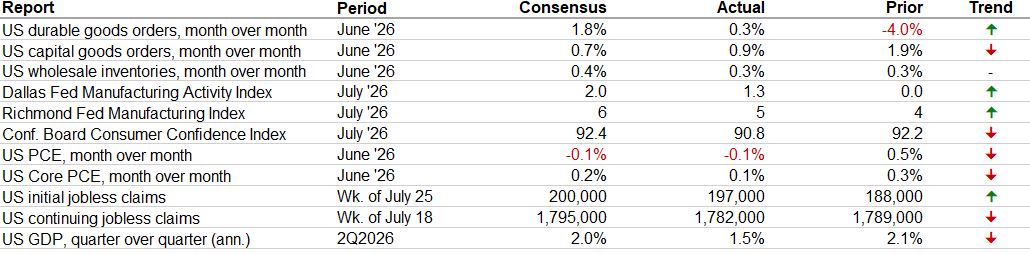

- Business investment looked resilient: Core capital goods orders and shipments exceeded expectations.

- Inflation eased modestly: Excluding food and energy, the “core” personal consumption expenditures (PCE) price index rose a lower-than-expected 0.1% month over month in June.

- However, growth was below expectations: Second-quarter 2026 gross domestic product (GDP) grew 1.5% annualized—below estimates ranging from 1.8% to 2.1%—as lower government spending offset stronger consumer spending.

Consumers spend, but confidence dips

- Personal spending rose 0.3% month over month in June, in line with expectations, and exceeded income growth of 0.2%.

- The Conference Board Consumer Confidence Index fell to 90.8 in July, as sentiment weakened despite still-stable job conditions.

CRC# 5797819 (08/2026)

How can E*TRADE from Morgan Stanley help?

Undervalued large firms

Consider putting your money in large companies whose stocks may be underpriced based on the principles of value investing.

Hedging with gold

Discover ways to diversify into a precious metal that many investors consider a potential safe haven when the economy slumps.

Futures

Like options, futures let you lock in a price now for an investment you’ll buy in the future. They cost much less than the actual investment, so you can control a large contract with a relatively small amount of capital.

Certificates of Deposit (CD)

Now, lock in 4.40% Annual Percentage Yield1,2 for 12 months for a limited time

Secure a fixed rate when you open and fund a new Bank CD. Additional terms available from to .3

Morgan Stanley Private Bank, Member FDIC.

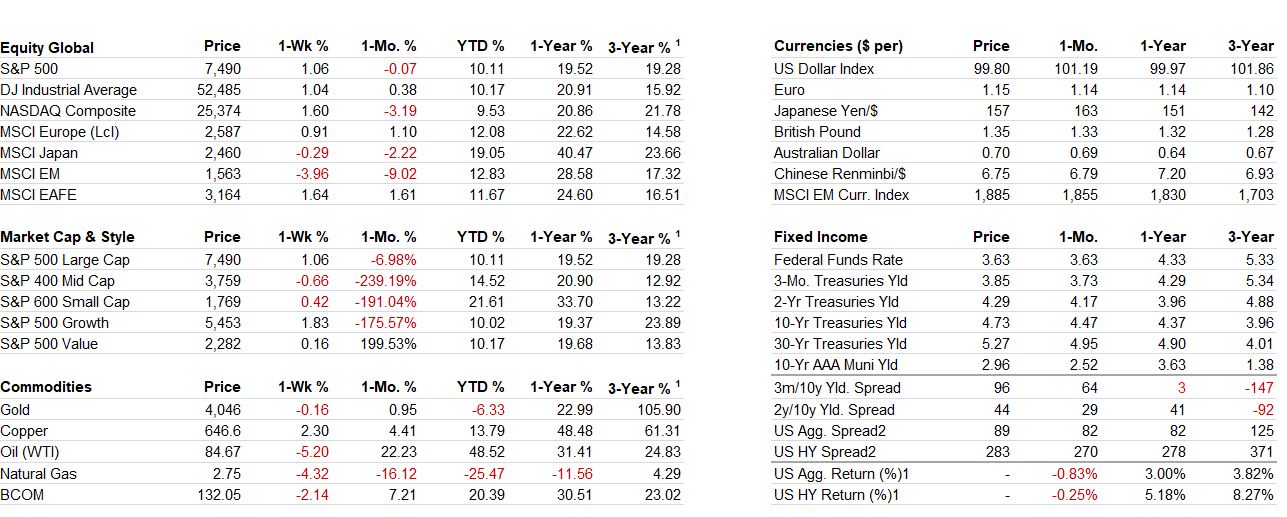

Cross-Asset Performance Table

Returns and prices of the most popular indices and assets as of 07/31/26.

1) Annualized 3-year % return. 2) Option Adjusted Spread (OAS): OAS is a measurement of the spread of a fixed income security rate and the risk-free rate of return, which is adjusted to take into account an embedded option. Equity risk premium is the excess return that an individual stock or the overall stock market provides over a risk-free rate. The risk-free rate represents the interest an investor would expect from an absolutely risk-free investment over a specified period of time. Past performance is not indicative of future results.

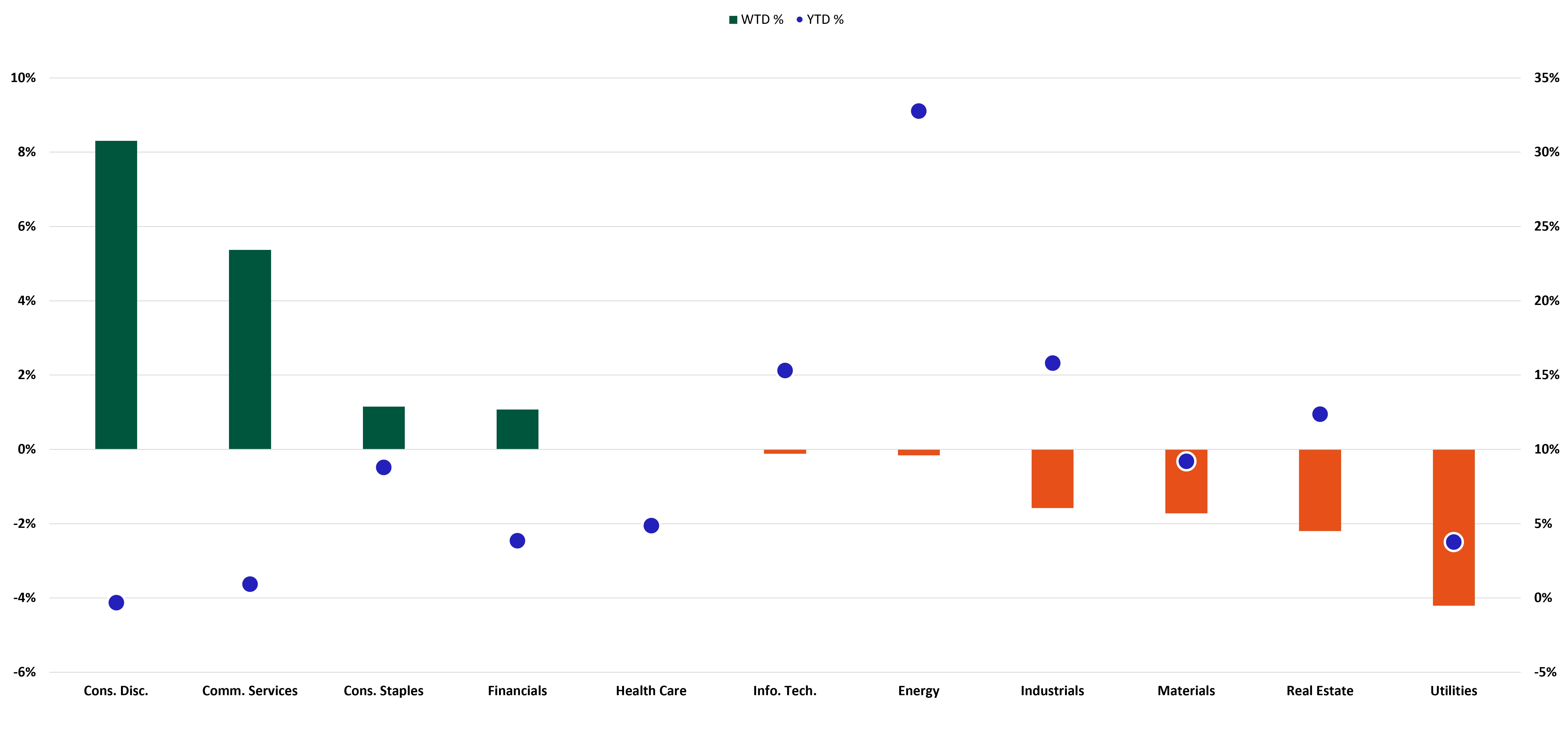

S&P 500 Sector Performance

Consumer Discretionary and Communication Services were the strongest S&P 500 sectors last week, while Real Estate and Utilities lagged.

Past performance is not indicative of future results.

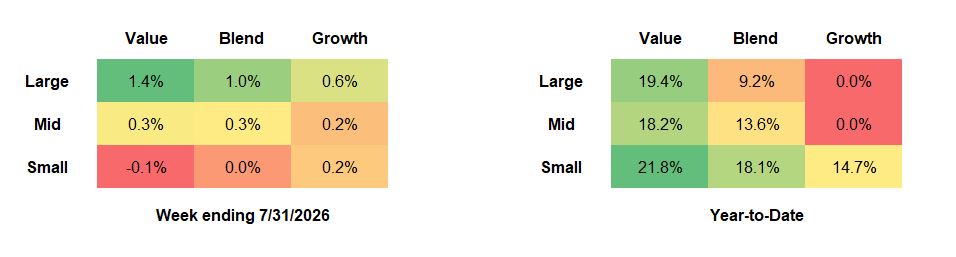

Russell U.S. Equity Style Performance

Large-cap stocks outperformed small-cap equities.

Past performance is not indicative of future results.

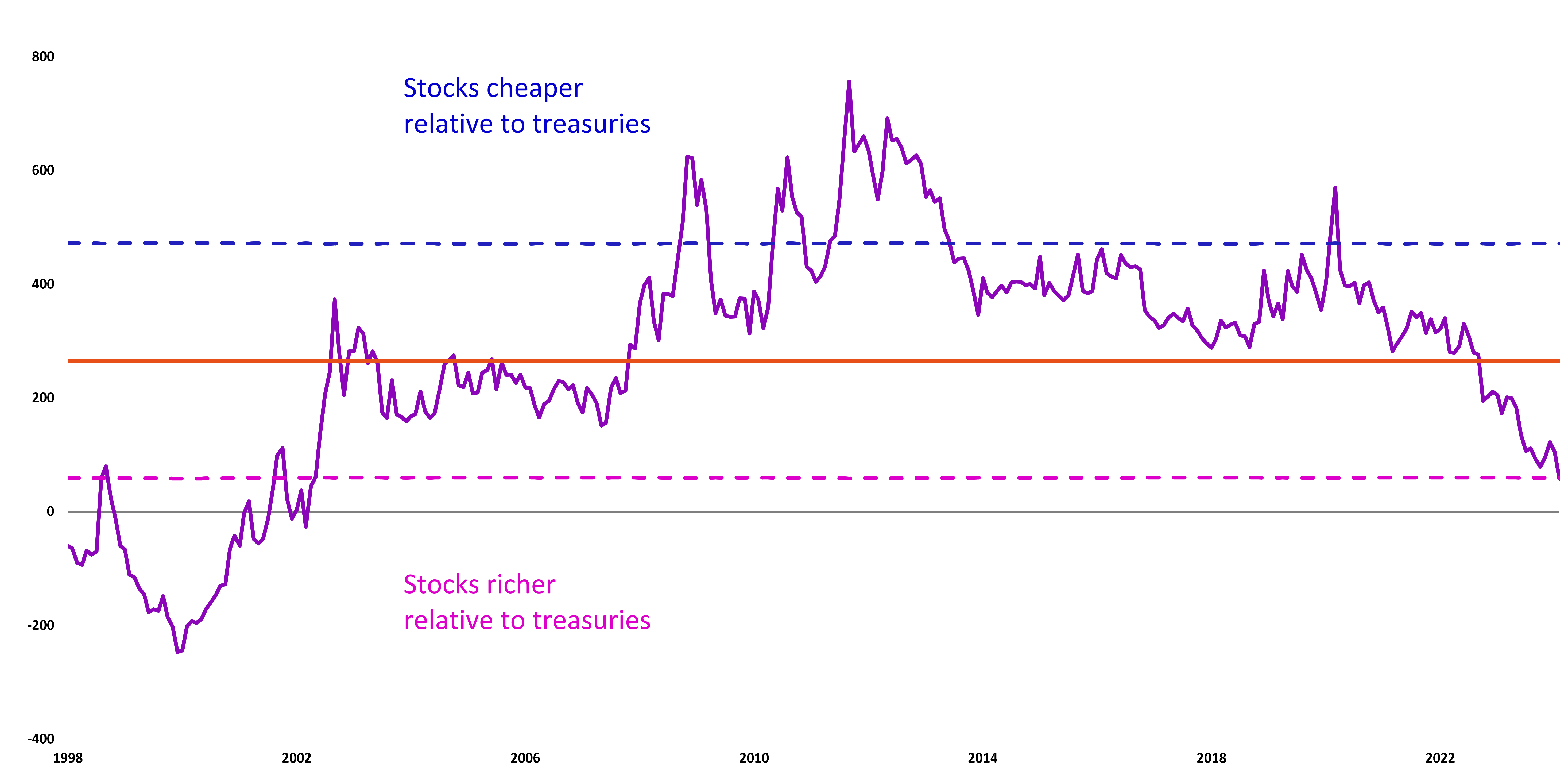

U.S. Equity Valuation

S&P 500 Equity Risk Premium

Bonds continue to appear attractive relative to equities.

Past performance is not indicative of future results.

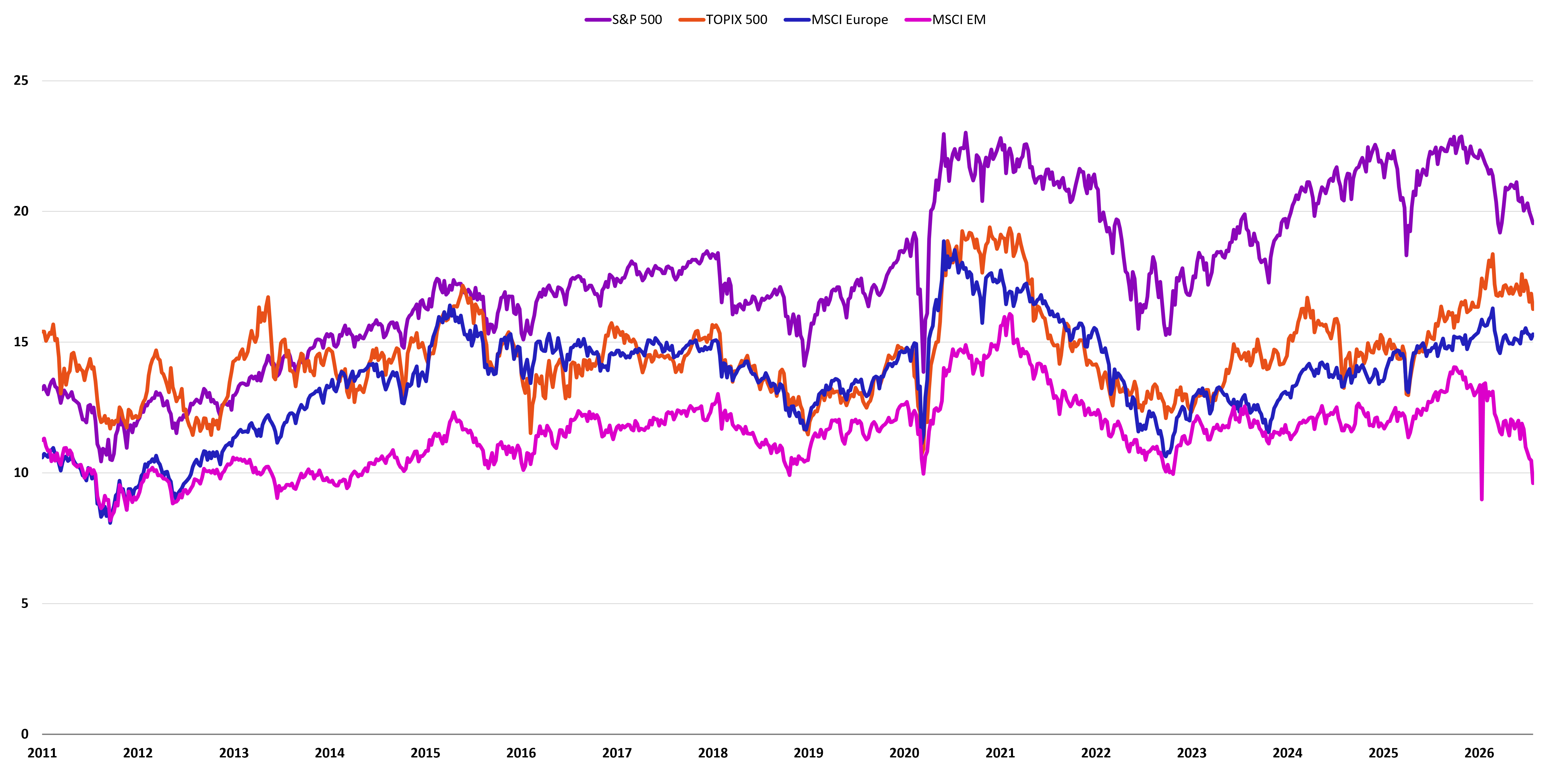

P/E Relative to Rest of World

The S&P 500 remains expensive relative to the rest of the world.

Past performance is not indicative of future results.

U.S. Fixed Income Valuation

The two-year Treasury yield decreased by 4 bps to 4.29% last week, while the 10-year Treasury yield increased by 3 bps to 4.73%.

†Interest Rate Volatility as measured by ICE BofAML Option Volatility Estimate Index (MOVE); *Mortgage-backed securities (MBS) are debt obligations that represent claims to the cash flows from pools of mortgage loans, most commonly on residential property. Mortgage loans are purchased from banks, mortgage companies, and other originators and then assembled into pools by a governmental, quasi-governmental, or private entity; **Options Adjusted Spread (OAS): A measurement of the spread of a fixed income security rate and the risk-free rate of return, which is adjusted to take into account an embedded option. Past performance is not indicative of future results.

Latest Economic Data

The Conference Board Consumer Confidence Index fell to 90.8 in July, as sentiment weakened despite still-stable job conditions.

The Week Ahead

Upcoming reports include Institute for Supply Management (ISM) Manufacturing and Services surveys for July, the Job Openings and Labor Turnover Survey (JOLTS) for June, second-quarter U.S. nonfarm productivity, and the Employment Situation Summary for July.

- ISM Manufacturing at 10:00 AM ET

- ISM Prices Paid at 10:00 AM ET

- Palantir Technologies Inc. Reports Earnings

- U.S. trade balance at 8:30 AM ET

- U.S. imports and exports at 8:30 AM ET

- U.S. factory orders at 10:00 AM ET

- U.S. JOLTS Survey at 10:00 AM ET

- Space Exploration Technologies Corp. Reports Earnings

- Advanced Micro Devices, Inc. Reports Earnings

- Caterpillar, Inc. Reports Earnings

- U.S. nonfarm productivity at 8:30 AM ET

- U.S. initial and continuing jobless claims at 8:30 AM ET

- U.S. average hourly earnings at 8:30 AM ET

- U.S. unemployment rate at 8:30 AM ET

- New York Fed One-Year Inflation Expectations at 8:30 AM ET

Index benchmarks

Cross-Asset Performance

S&P 500: A market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. It measures the movement of the largest issues. Standard and Poor's chooses the member companies for the 500 based on market size, liquidity and industry group representation. Included are the stocks of industrial, financial, utility, and transportation companies. Since mid-1989, this composition has been more flexible and the number of issues in each sector has varied. The returns presented for the S&P 500 are total returns, including the reinvestment of dividends each month.

Dow Jones Industrial Average: Computed by summing the prices of the stocks of 30 companies and then dividing that total by an adjusted value—one which has been adjusted over the years to account for the effects of stock splits on the prices of the 30 companies. Dividends are reinvested to reflect the actual performance of the underlying securities.

NASDAQ Composite: Measures the performance of all issues listed in the NASDAQ Stock Market, except for rights, warrants, units, and convertible debentures. Morningstar reports the NASDAQ Composite as a price return.

MSCI Europe IMI: This index captures large, mid and small cap representation across 16 Developed Markets countries in Europe. With 1,372 constituents, the index covers approximately 99% of the free float-adjusted market capitalization across the Developed Markets countries of Europe.

MSCI Japan IMI: This index is designed to measure the performance of the large, mid and small cap segments of the Japan market. With 1,134 constituents, the index covers approximately 99% of the free float-adjusted market capitalization in Japan.

MSCI EM (Emerging Markets) Index: A free float-adjusted market-capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 23 emerging market country indexes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Russia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates. For more information, visit the MSCI web site.

MSCI EAFE (Europe, Australasia, Far East) Index: A free float-adjusted market-capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Index consists of the following 21 developed market country indexes: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom. For more information, visit the MSCI website.

S&P 400 Index: This index provides investors with a benchmark for mid-sized companies. The index measures the performance of mid-sized companies, reflecting the distinctive risk and return characteristics of this market segment.

S&P 600 Index: This index measures the small-cap segment of the U.S. equity market. The index is designed to track companies that meet specific inclusion criteria to ensure that they are liquid and financially viable.

S&P 500 Growth: This index is a style-concentrated index designed to track the performance of stocks that exhibit the strongest growth characteristics by using a style-attractiveness-weighting scheme.

S&P 500 Value: This index is a style-concentrated index designed to track the performance of stocks that exhibit the strongest value characteristics by using a style-attractiveness-weighting scheme.

Bloomberg Commodity Index: Made up of 22 exchange-traded futures on physical commodities. The index currently represents 20 commodities, which are weighted to account for economic significance and market liquidity.

US Trade-Weighted Dollar Index: A weighted average of the foreign exchange value of the US dollar against a subset of the broad index currencies that circulate widely outside the US.

MSCI Emerging Markets Currency Index: sets the weights of each currency equal to the relevant country weight in the MSCI Emerging Markets Index.

Bloomberg US Aggregate Index: The US Aggregate Index covers the dollar-denominated investment-grade fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS pass-through securities, asset-backed securities, and commercial mortgage-based securities. These major sectors are subdivided into more specific sub-indices that are calculated and published on an ongoing basis. Total return comprises price appreciation/depreciation and income as a percentage of the original investment. This index is rebalanced monthly by market capitalization.

Bloomberg US Corporate High Yield Bond Index: This index is composed of fixed-rate, publicly issued, non-investment grade debt.

S&P Sector Performance

The S&P 500 Consumer Discretionary sector comprises those companies included in the S&P 500 that are classified as members of the consumer discretionary sector.

The S&P 500 Consumer Staples sector comprises those companies included in the S&P 500 that are classified as members of the consumer staples sector.

The S&P 500 Energy sector comprises those companies included in the S&P 500 that are classified as members of the energy sector.

The S&P 500 Financials sector comprises those companies included in the S&P 500 that are classified as members of the financial sector.

The S&P 500 Health Care sector comprises those companies included in the S&P 500 that are classified as members of the health care sector.

The S&P 500 Industrials Sector comprises those companies included in the S&P 500 that are classified as members of the industrials sector.

The S&P 500 Information Technology Sector comprises those companies included in the S&P 500 that are classified as members of the information technology sector.

The S&P 500 Materials Sector comprises those companies included in the S&P 500 that are classified as members of the materials sector.

The S&P 500 Communications Services Sector comprises those companies included in the S&P 500 that are classified as members of the telecommunications services sector.

The S&P 500 Utilities Sector comprises those companies included in the S&P 500 that are classified as members of the utilities sector.

The S&P 500 Real Estate Sector comprises those companies included in the S&P 500 that are classified as members of the real estate sector.

US Equity Style Performance

Weekly and monthly style performance charts use Russell 1000, Russell Mid Cap, and Russell 2000 style indexes to represent large cap, mid cap, and small cap respectively.

Russell 1000: Consists of the 1000 largest companies within the Russell 3000 index. Also known as the Market-Oriented Index, because it represents the group of stocks from which most active money managers choose. The returns we publish for the index are total returns, which include reinvestment of dividends. Frank Russell Company reports its indexes as one-month total returns.

Russell 1000 Growth: Market-capitalization weighted index of those firms in the Russell 1000 with higher price-to-book ratios and higher forecasted growth values. The Russell 1000 includes the largest 1000 firms in the Russell 3000, which represents approximately 98% of the investable US equity market.

Russell 1000 Value: Market-capitalization weighted index of those firms in the Russell 1000 with lower price-to-book ratios and lower forecasted growth values. The Russell 1000 includes the largest 1000 firms in the Russell 3000, which represents approximately 98% of the investable US equity market.

Russell 2000: Consists of the smallest 2000 companies in the Russell 3000 Index, representing approximately 7% of the Russell 3000 total market capitalization. The returns we publish for the index are total returns, which include reinvestment of dividends.

Russell 2000 Growth: Market-weighted total return index that measures the performance of companies within the Russell 2000 Index having higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Index includes the 2000 firms from the Russell 3000 Index with the smallest market capitalizations. The Russell 3000 Index represents 98% of the of the investable US equity market.

Russell 2000 Value: Market-weighted total return index that measures the performance of companies within the Russell 2000 Index having lower price-to-book ratios and lower forecasted growth values. The Russell 2000 Index includes the 2000 firms from the Russell 3000 Index with the smallest market capitalizations. The Russell 3000 Index represents 98% of the of the investable US equity market.

Russell Midcap: Measures the performance of the 800 smallest companies in the Russell 1000 Index, which represent approximately 25% of the total market capitalization of the Russell 1000 Index. As of the latest reconstitution, the average market capitalization was approximately $4.0 billion; the median market capitalization was approximately $2.9 billion. The largest company in the index had an approximate market capitalization of $12 billion.

Russell Midcap Growth: Market-weighted total return index that measures the performance of companies within the Russell Midcap Index having higher price-to-book ratios and higher forecasted growth values. The Russell Midcap Index includes firms 201 through 1000, based on market capitalization, from the Russell 3000 Index. The Russell 3000 Index represents 98% of the of the investable U.S. equity market.

Russell Midcap Value: Market-weighted total return index that measures the performance of companies within the Russell Midcap Index having lower price-to-book ratios and lower forecasted growth values. The Russell Midcap Index includes firms 201 through 1000, based on market capitalization, from the Russell 3000 Index. The Russell 3000 Index represents 98% of the of the investable U.S. equity market.

P/E Relative to Rest of World

TOPIX: This free-floated-adjusted index tracks all domestic companies of the exchange’s First Section.

US Fixed Income Valuation

ICE BofAML Option Volatility Estimate Index (MOVE): A yield curve-weighted index of the normalized implied volatility on one-month treasury option.

An investment cannot be made directly in a market index.