Stocks bounce as earnings season begins

- Market chops higher for week, trade spat continues

- Big banks up, medium banks down, gold tops $4,300

- This week: Consumer Price Index (CPI), Tesla and Netflix earnings

Last week had a little bit of everything—a new earnings season, more trade-war volleys, another AI mega-deal, and lots of Fed-speak. The result: choppy trading for stocks, but a net gain for the broad market.

Nonetheless, the S&P 500 (SPX) spent the week entirely within the range of Friday, October 10’s sell-off day, which unfolded as the White House threatened to ramp up tariffs on China. But the market bounced back strongly on Monday as President Trump softened his rhetoric and OpenAI announced a strategic partnership with chip firm Broadcom (AVGO).

The SPX swung up and down the remainder of the week as China threatened trade-war countermeasures, Fed Chair Jerome Powell appeared to confirm another rate cut, and earnings rolled in:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Stocks climb, but consolidate below recent record highs.

The fine print: The fine print: Earnings season kicked off with big banks beating estimates, and most of their stocks got at least temporary boosts. But sell-offs in some regional banks that reported loan losses appeared to undermine sentiment on Thursday, and the financial sector turned out to be the S&P 500’s weakest performer, despite bouncing on Friday.

The number: 11, the number of days until the proposed October 31 meeting between President Trump and President Xi Jinping of China. Morgan Stanley & Co. strategists think the recent “rhetorical escalation” will most likely be followed by “a reset and eventual framework deal.”1

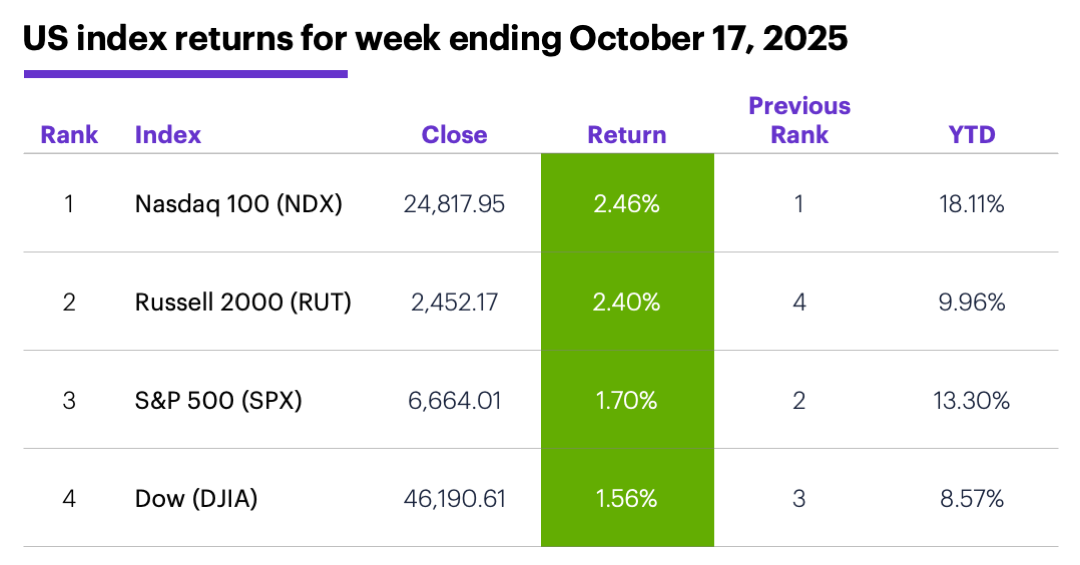

The scorecard: The Nasdaq 100 (NDX) tech index led the market last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were communication services (+3.7%), real estate (+3.5%), and tech (+2.3%). The weakest sectors were financials (+0.2%), health care (+0.8%), and energy (+0.9%).

Stock moves: Critical Metals (CRML) +55% to $23.28 on Monday (and +29% to $29.97 on Tuesday), Praxis Precision Medicines (PRAX) +184% to $162.71 on Thursday. On the downside, Mercurity Fintech (MFH) -22% to $18.15 on Monday (and -27% to $14.83 on Wednesday), Aqua Metals (AQMS) -53% to $13.94 on Wednesday.

Yields and the dollar: The 10-year US Treasury yield fell 0.06% to 4% last week. The US Dollar Index (DXY) fell 0.55 to 98.43.

Futures: Despite a Friday sell-off, December gold (GCZ5) jumped $212.90 to $4,213.30 last week. December WTI crude oil (CLZ5) fell $1.33 to $57.15 for the week. Biggest rallies: December silver (SIZ5) +6.7%, December coffee (KCZ5) +6.5%. Biggest declines: January orange juice (OJF6) -10.5%, October bitcoin (BTCV5) -8.9%.es: January orange juice (OJF6) -10.5%, October bitcoin (BTCV5) -8.9%.

Coming this week

This week’s earnings include the first two Mag-7 stocks, alongside a busy lineup of consumer, defense, tech and airline names:

●Monday: Cleveland Cliffs (CLF), Freeport McMoRan (FCX), NVR (NVR), Southern Copper (SCCO), Steel Dynamics (STLD), Seagate Technology (STX), Taiwan Semiconductor (TSM), Wintrust (WTFC)

●Tuesday: General Electric (GE), General Motors (GM), Halliburton (HAL), Coca Cola (KO), Lockheed Martin (LMT), Mattel (MAT), 3M (MMM), Netflix (NFLX), Northrop Grumman (NOC), Spirit Aerosystems (SPR), Texas Instruments (TXN)

●Wednesday: Alcoa (AA), Edwards Lifesciences (EW), GE Vernova (GEV), Lam Research (LRCX), Medpace (MEDP), O'Reilly Automotive (ORLY), AT&T (T), Tesla (TSLA)

●Thursday: American Airlines (AAL), Aon (AON), Ford (F), Honeywell (HON), Intel (INTC), Southwest Airlines (LUV), Newmont (NEM), T-Mobile US(TMUS), Union Pacific (UNP), Verisign (VRSN)

●Friday: General Dynamics (GD), Gentex (GNTX), Procter & Gamble (PG)

The delayed September Consumer Price Index (CPI) headlines another week of shutdown-curtailed economic data:

●Monday: Leading Economic Indicators Index

●Thursday: Chicago Fed National Activity Index, existing home sales

●Friday: Consumer Price Index (CPI), S&P Global Manufacturing and Services PMIs (flash), consumer sentiment, new home sales

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Inside-out SPX

The past couple of weeks marked a short-term volatility expansion and contraction pattern in the SPX. From October 6 to October 10 the index formed an “outside week” by trading above the prior week’s high and below its low (volatility expansion). Last week it did the opposite, forming an “inside week” by trading within the previous week’s range (volatility contraction).

Also, in this case the outside week closed lower and the inside week closed higher, which has happened only 22 other times since 1957. Four weeks later the SPX’s median return was 1.3%, which is slightly higher than its overall four-week median return of 1%.2

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. US-China: Tactical Escalation. 10/12/25.

2 Reflects S&P 500 weekly closing prices, 1957-2025. Supporting document available upon request