Tech boosts rebound

- Stocks rally on Middle East deal, stumble on Fed

- Chips bounce, oil retreats as Hormuz reopens

- This week: Fed inflation, final Q1 GDP

Familiar themes drove up-and-down market action—the Middle East, inflation and the Fed, and AI—but US stocks still logged their 11th up week of the past 12.

The S&P 500 (SPX) charged out of the gate last Monday after news of a US-Iranian Memorandum of Understanding (MoU) that would reopen the Strait of Hormuz—and, it was hoped, begin to normalize global energy markets and ease inflation pressures. But Wednesday’s sharp sell-off after the first Fed meeting of the Kevin Warsh era erased that gain, before a robust Thursday rally put the index back into positive territory for the week:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Stocks recover from Fed stumble.

The fine print: The Fed’s seemingly hawkish (and brief) statement last Wednesday, which showed nine board members expected a rate hike this year, appeared to catch the market off guard. But Morgan Stanley & Co. economists believe the Fed will leave rates unchanged this year,1 while Ellen Zentner, Chief Economic Strategist for Morgan Stanley Wealth Management, expected the Fed’s next move to be a cut—but not until 2027.

The move: Brent crude oil prices—the global benchmark—tumbled $7.48 (8.6%) to $79.82 last week. While Morgan Stanley & Co. analysts expect a “tight” summer for oil, they believe the Brent oil price to be anchored around $80 in Q4.2

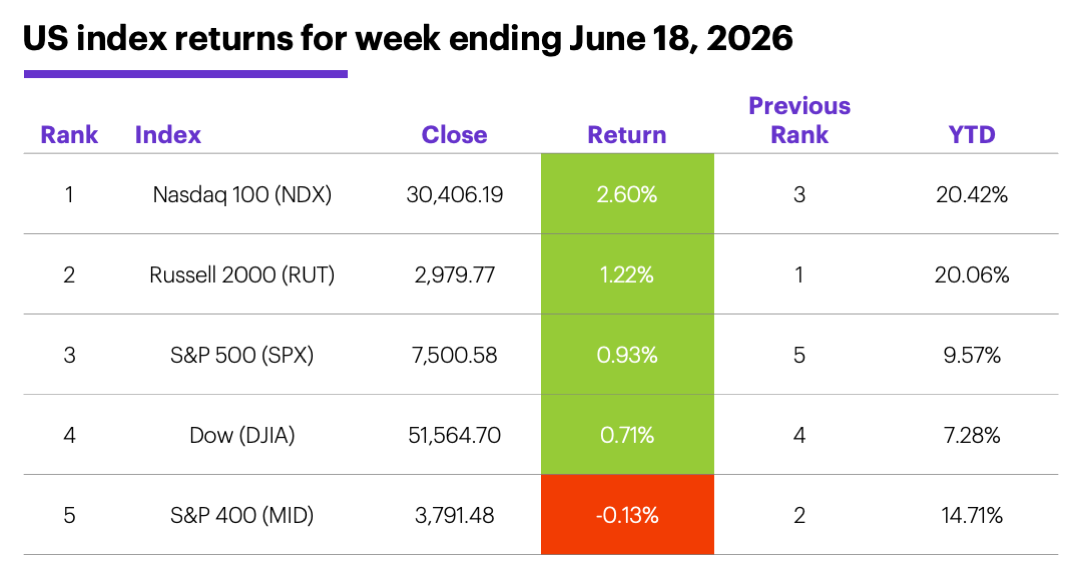

The scorecard: Fueled by a rebound in the volatile semiconductor space, the Nasdaq 100 (NDX) tech index outperformed last week, pushing its year-to-date gain above 20%:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

S&P 500 sector returns: The strongest S&P 500 sectors last week were tech (+3%), industrials (+2.6%), and communication services (+1.1%). The weakest sectors were energy (-7%), real estate (-3.6%), and health care (-3%).

S&P 500 stock movers: Last week’s biggest gains were Western Digital (WDC) +43% to $746.23, Moderna (MRNA) +28% to $63.96, Seagate (STX) +23% to $1,070.23. The biggest losses were Fox Class A (FOXA) -23% to $52.23, Accenture (ACN) -23% to $127.98, Fox Class B (FOX) -23% to $46.95. Other: uniQure (QURE) +78% to $48.16 on Wednesday.

Yields and the dollar: The 10-year US Treasury yield fell 0.03% to 4.45% last week. The US Dollar Index (DXY) rallied 1.10 to a 13-month high of 110.85.

Commodity futures: August WTI crude oil (CLQ6) tumbled $7.50 (9%) to $75.85 last week—its lowest close since March 5. August gold (GCQ6) rose $7.10 to $4,245.90. Morgan Stanley Wealth Management strategists recently noted the weakness in gold, which is trading below its 200-day moving average, could present an opportunity to build a long-term hedge against geopolitical, fiscal, and inflation risks.3

Crypto: Bitcoin -1% to $62,896.47 last week, Ethereum +2.7% to $1,709.53.

Coming this week

Thursday’s the big day on the economic calendar, with the Fed’s preferred inflation gauge (PCE Price Index), Durable Goods Orders, and the final Q1 GDP estimate:

●Tuesday: S&P Global Manufacturing and Services PMIs (flash)

●Wednesday: Current Account, New Home Sales

●Thursday: Personal Income and Spending, PCE Price Index, Chicago Fed National Activity Index, Durable Goods Orders, GDP (Q1 final)

●Friday: Trade Balance in Goods, Retail and Wholesale Inventories (advance), Consumer Sentiment

This week’s earnings include:

●Monday: AeroVironment (AVAV)

●Tuesday: FedEx (FDX), KB Home (KBH)

●Wednesday: Micron (MU), Paychex (PAYX), Trip.com (TCOM), Worthington Enterprises (WOR)

●Thursday: Commercial Metals (CMC), Darden Restaurants (DRI), McCormick (MKC), TD Synnex (SNX), Winnebago Industries (WGO)

●Friday: Apogee (APOG)

This week’s IPOs include:

●Thursday: Doncasters (DPC) on Thursday.

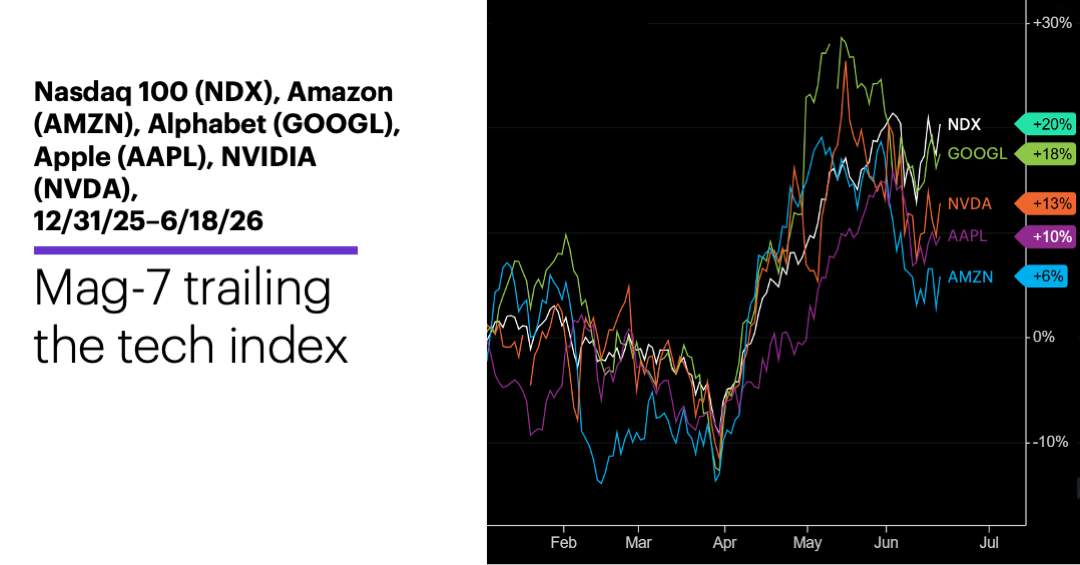

A “more reasonable” Mag-7?

As of Friday, the Magnificent 7 stocks found themselves in an unusual position. Not only were most of them underperforming the SPX so far this year, three of them—Microsoft (MSFT), Meta (META), and Tesla (TSLA)—were in the red.

Source: Power E*TRADE Pro. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest directly in an index.)

This relative underperformance is even more evident in the context of the tech sector. The chart above shows that even the four Magnificent 7 stocks that were positive territory for the year—Alphabet (GOOGL), Amazon (AMZN), Apple (AAPL), and NVIDIA (NVDA)—were still trailing the NDX.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. June FOMC Reaction: Hawkish Today, Reforms Tomorrow. 6/18/26.

2 MorganStanley.com. Let the Oil Flow. 6/15/26.

3 MorganStanley.com. From Energy to AI: Global Inflation Risks Evolve. 6/17/26.