Stocks extend rally

- Stocks hit fresh records amid positive trade talk

- Health care sector leads, mixed earnings for megacaps

- This week: Fed meeting, jobs report, GDP, inflation, “big” earnings

Last week the US stock market pushed to record levels for the fifth week in a row, riding mostly positive earnings, an absence of negative economic news, and signs of progress on trade and tariffs.

The S&P 500 (SPX) hit new record highs every day last week, notching its fourth positive week of the past five:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Stocks extend gains ahead of key week of economic data and earnings.

The fine print: Movement on the tariff front appeared to be positive, although some details were fuzzy. On Tuesday, US Treasury Secretary Scott Bessent said the August 12 deadline marking the end of the 90-day suspension of tariffs on China would “likely be extended.” On Wednesday, the US and Japan announced Japanese exports to the US would be tariffed at 15%, lower than the previously threatened 25% rate,1 but well above pre-Trump Administration levels.

The move: As of Friday, the SPX was up 28.2% from its April 8 tariff sell-off low closing price—its strongest 74-trading-day rally since July 2020.

The number: 4.25%-4.5%, the current fed funds rate, which is expected to remain intact after this week’s FOMC meeting, although the announcement may show some members dissented in favor of cutting rates.

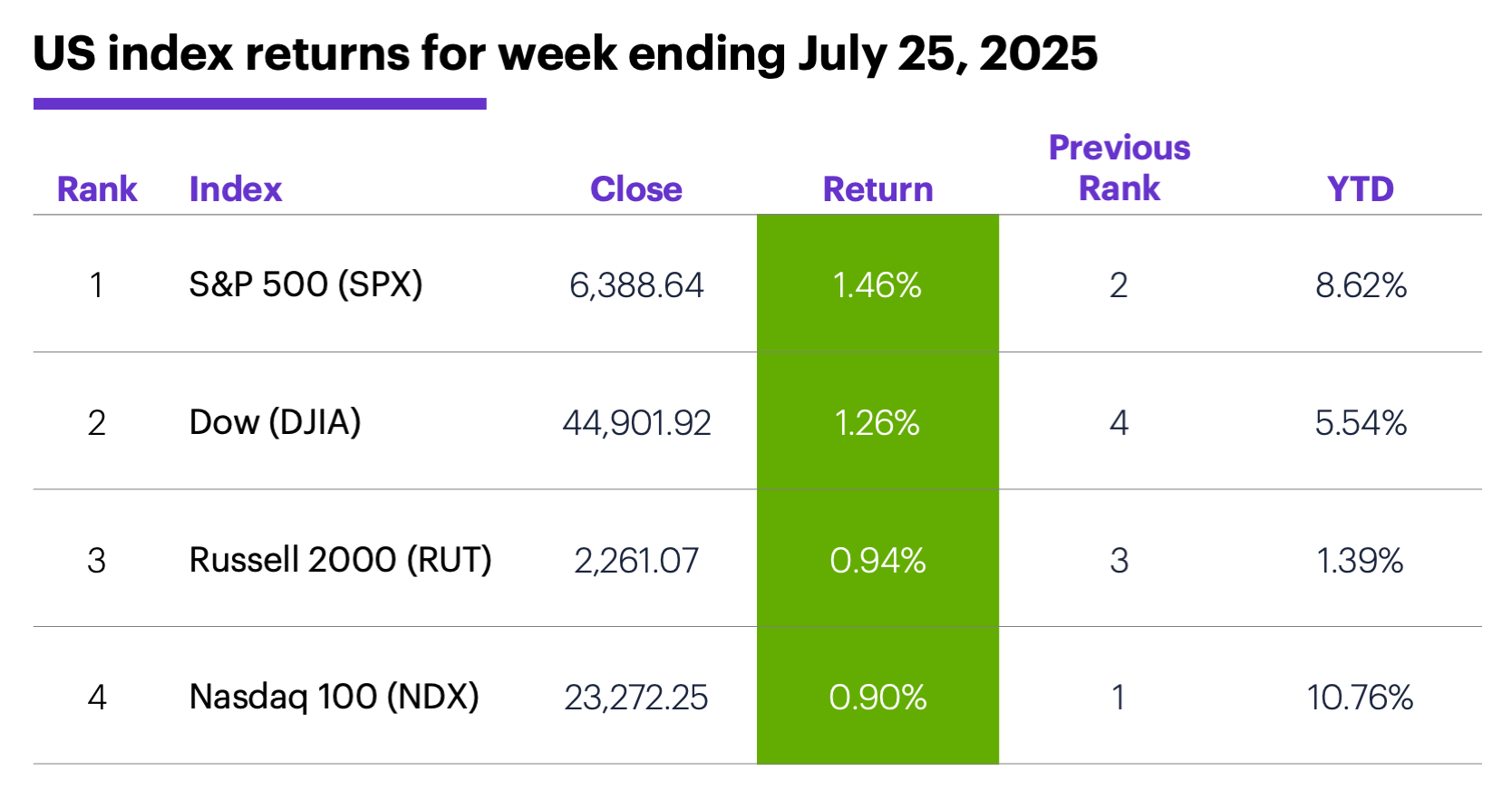

The scorecard: Large caps led the market last week, although Nasdaq 100 (NDX) tech index’s year-to-date percentage gain extended into double digits:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were information technology (+2%), utilities (+1.4%), and industrials (+0.7%). The weakest sectors were energy (-3.9%), health care (-2.5%), and materials (-1.5%).

Stock moves: USA Rare Earth (USAR) +31% to $15.54 on Tuesday, SharpLink Gaming (SBET) +29% to $37.38 on Wednesday. On the downside, Newegg Commerce (NEGG) -26% to $36.22 on Monday (and -19% to $29.33 on Tuesday), CareDx (CDNA) -38% to $11.81 on Wednesday.

Yields: The benchmark 10-year Treasury yield rose 0.01% to 4.43% last week.

US dollar: The US Dollar Index (DXY) rallied 0.63 to 98.48.

Futures: September WTI crude oil (CLU5) ended another choppy week $1.30 lower at $66.05. August gold also (GCQ5) extended its consolidation, falling $5.70 to $3,358.30 last week. Biggest gains: July ether (ETHN5) +18.8%, September orange juice (OJU5) +10.3%. Biggest losses: September cocoa (CCU5) -4.6%, September hard red wheat (KWU5) -3.7%.

Coming this week

The economic calendar is packed—a Fed meeting, inflation (PCE Price Index), and the monthly jobs report are highlights:

●Tuesday: trade balance in goods (advance), retail and wholesale inventories (advance), S&P Case-Shiller Home Price Index, FHFA House Price Index, Job Openings and Labor Turnover Survey (JOLTS), consumer confidence

●Wednesday: ADP private employment report, Q2 GDP (second estimate), pending home sales, Fed interest rate decision

●Thursday: job cuts, personal income and spending, PCE Price Index

●Friday: Employment Report, S&P Global Manufacturing PMI, ISM Manufacturing Index, consumer sentiment (final), construction spending

This week’s earnings lineup is just plain big—big pharma, big oil and (especially) big tech, including Magnificent-7 members Microsoft (MSFT), Meta (META), Apple (AAPL), and Amazon (AMZN). Here’s a sample of the roughly 1,000 companies scheduled to release their numbers:

●Monday: Archer Daniels Midland (ADM), Amkor Technology (AMKR), AstraZeneca (AZN), Lattice Semiconductor (LSCC), McDonald's (MCD), CarParts.com (PRTS), Rambus (RMBS), Whirlpool (WHR), Waste Management (WM)

●Tuesday: Boeing (BA), Electronic Arts (EA), Eagle Materials (EXP), Merck (MRK), Procter & Gamble (PG), PayPal (PYPL), Qorvo (QRVO), Starbucks (SBUX), Spotify Technology (SPOT), UnitedHealth Group (UNH), United Parcel Service (UPS), Visa (V)

●Wednesday: Arm Holdings (ARM), Carvana (CVNA), eBay (EBAY), Ford Motor (F), Hershey (HSY), Humana (HUM), Kraft Heinz (KHC), Lam Research (LRCX), Meta Platforms (META), Microsoft (MSFT), Qualcomm (QCOM), Turning Point Brands (TPB), Verisk Analytics (VRSK), US Steel (X)

●Thursday: Apple (AAPL), AbbVie (ABBV), Amazon (AMZN), Baxter International (BAX), Bristol Myers Squibb (BMY), Clorox (CLX), Coinbase (COIN), CVS Health (CVS), Kellanova (K), Mastercard (MA), MicroStrategy (MSTR), Reddit (RDDT)

●Friday: BP (BP), Cboe Global Markets (CBOE), Colgate-Palmolive (CL), Chevron (CVX), Kimberly Clark (KMB), Moderna (MRNA), Regeneron Pharmaceuticals (REGN), Exxon Mobil (XOM)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Industrial strength

With two of the “Magnificent-7” stocks reporting earnings last week and four more scheduled to do so this week, the recent market discussion has understandably been skewed toward tech and megacap performance.

That’s as good a reason as any to note that while it’s been a good year for tech—the S&P 500 tech sector was up 12.5% as of Friday—it’s been an even better one for the industrial sector, which has gained 17.5%. One of the primary drivers of that return has been the aerospace and defense industry, which on Friday was up 32.5% for the year.

When Morgan Stanley & Co. upgraded the group’s outlook in April, the analysts highlighted two pillars of potential strength. First, defense is largely insulated from tariff risk, in part because of its primarily domestic supply chain. Second, buying from US defense suppliers may be an opportunity for countries to reduce their trade imbalances with the US—a major goal of the Trump administration. 2

More recently, the analysts reiterated the potential relative strength of defense contractor Northrop Grumman (NOC), noting that accelerating global defense spending (among other factors) provides a tailwind for NOC’s business.3 The stock rallied to a new record high last Tuesday after announcing earnings.

Market Mover Update: Toyota (TM) fell for a second-straight day on Friday after posting its biggest one-day gain since 2008 last Wednesday (see “Tariff news turbocharges auto stocks”).

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 The New York Times. U.S. and Japan Reach Trade Deal. 7/23/25.

2 MorganStanley.com. Upgrading Defense to Attractive; Upgrade LMT to OW and Downgrade GD to EW; NOC to Top Pick. 7/23/25.

3 MorganStanley.com. Best of Breed Defense Portfolio, Top Pick in Defense. 7/23/25.