Stocks march on

- Stocks hit new highs, inflation readings mixed

- Health care leads, small caps strengthen, tech slips

- This week: retail earnings, Jackson Hole, FOMC minutes

A buoyant US stock market continued to embrace good news and shrug off bad news last week, pushing to multiple record highs amid mixed inflation data.

The S&P 500 (SPX) set records every day but Monday, getting its biggest boost last Tuesday after the release of a Consumer Price Index (CPI) that was more or less in line with expectations, while stumbling briefly—but recovering—after a much-hotter-than-expected Producer Price Index (PPI) on Thursday. The SPX closed slightly lower Friday but not before hitting a record intraday high early in the trading session:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: New index highs as markets remains focused on rate cuts.

The fine print: Initial reactions don’t always hold, but the market appeared to decide the “hot” PPI print was less important than the merely warm CPI reading, and that the Fed will be inclined to cut interest rates next month amid growing signs of labor-market weakness. Separately, the year’s weakest sector—health care—led the market to the upside last week. Tech, the strongest sector over the past six months, lost ground.

The number: 4, the number of Magnificent-7 stocks underperforming the SPX this year, as of Friday.

The move: Despite falling 21% last Friday, Newegg (NEGG) rallied 26.6% to $101.02 for the week. At Friday's close, it was up 1,987.2% since May 30, when it closed at $4.84.

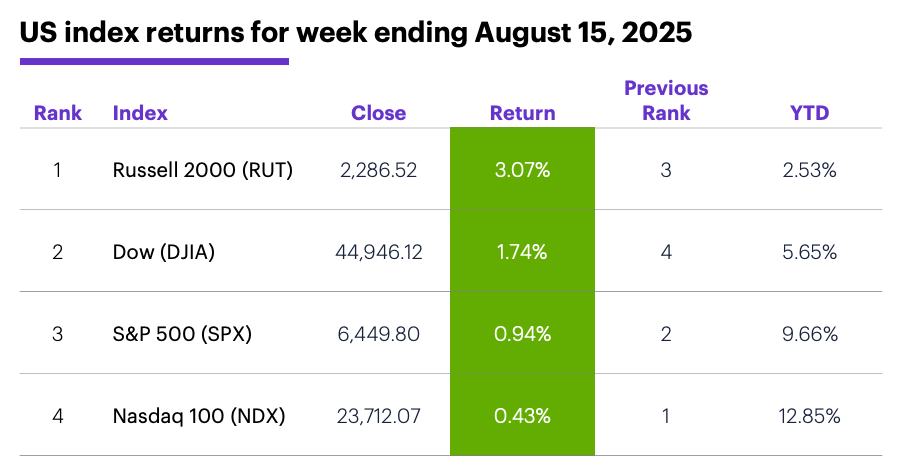

The scorecard: The Russell 2000 (RUT) small-cap index led the market:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were health care (+4.6%), consumer discretionary (+2.5%), and communication services (+2.1%). The weakest sectors were utilities (-0.9%), consumer staples (-0.8%), and industrials (-0.3%).

Stock moves: Sapiens (SPNS) +44% to $42.56 and Paramount Skydance (PSKY) +37% to $15, both on Wednesday. On the downside, Monday.com (MNDY) -30% to $174.13 on Monday, Innovative Solutions & Support (ISSC) -32% to $13.51 on Thursday.

Yields: The 10-year US Treasury yield climbed 0.04% to 4.32% last week.

US dollar: The US Dollar Index (DXY) ended a choppy week down 0.33 at 97.85.

Futures: October WTI crude oil (CLV5) tagged its lowest low since June 6 last Wednesday, ending the week down $1.02 at $61.98. Thanks mostly to a 2.6% sell-off last Monday, December gold (GCZ5) fell $108.70 to $3,382.60 last week. Biggest rallies: December coffee (KCZ5) +10.5%, September Lithium (LTHU5) +9%. Biggest declines: September lumber (LBSU5) -6.7%, September VIX (VXU5) -3.6%.

Coming this week

Retail earnings take center stage this week:

●Monday: Fabrinet (FN), Palo Alto Networks (PANW)

●Tuesday: Dycom (DY), Keysight (KEYS), Macy's (M), Medtronic (MDT), Toll Brothers (TOL)

●Wednesday: Analog Devices (ADI), Estee Lauder (EL), Lowe's (LOW), Target (TGT), TJX (TJX), Williams Sonoma (WSM)

●Thursday: Intuit (INTU), Ross Stores (ROST), Ubiquiti (UI), Workday (WDAY), Walmart (WMT), Zoom Communications (ZM)

●Friday: BJ's Wholesale Club (BJ), Buckle (BKE)

On the economic calendar traders will get a look at the minutes from the Fed’s July policy meeting, along with any notable comments emerging from the Fed’s annual Jackson Hole Economic Policy Symposium:

●Monday: NAHB Housing Market Index

●Tuesday: housing starts and building permits

●Wednesday: FOMC minutes

●Thursday: S&P Global Manufacturing and Services PMIs (flash), existing home sales, Leading Economic Indicators Index, Jackson Hole, day 1

●Friday: Jackson Hole, day 2 (Jerome Powell speech)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

News from the nuclear renaissance

The 10 months since “AI fuels unique energy space” highlighted rallies in certain nuclear energy stocks, the industry has kept humming. Oklo (OKLO), Centrus Energy (LEU), and NuScale Power (SMR) have gained an additional 332%, 133%, and 86%, respectively, since then.

Morgan Stanley & Co. research recently updated its coverage of the nuclear renaissance theme, noting its intersection with three other “global megatrends”—Tech Diffusion, Multipolar World, and Future of Energy. While the foundation of the nuclear bull case is AI-driven energy demand, it represents an evolving market with many moving parts. The analysts discuss other countries that could emerge as leaders in the global nuclear market, as well as different nuclear technologies that may play a role in the market.

Their recent report expands their previous list of stocks that may benefit from this theme from 51 to 63, including 26 with an Overweight rating.1

Short-term VIX signal. Finally, Friday’s stock market softness may not have surprised traders who keep tabs on the Cboe Volatility Index (VIX). On Thursday the VIX closed higher even though the SPX closed at a new record high, signaling heightened concerns about volatility despite a rising stock market. Since 1990, whenever the VIX closed higher the same day the SPX closed at a 50-day (or longer) high, the SPX closed lower the next day more than half of the time the next two days.2

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Global Thematics and Sustainability: The Nuclear Renaissance Is Here – What's Next? 8/12/25.

2 Figures reflect S&P 500 (SPX) and Cboe Volatility Index (VIX) daily price data, 1993-2025. There were 383 instances of the pattern. Supporting document available upon request.