What is a CD ladder?

E*TRADE from Morgan Stanley

05/22/26Summary: A Certificate of Deposit (CD) ladder can help you earn competitive yields, choose your maturity schedule, and provide steady access to cash.

Saving should be like climbing a ladder, with each step getting you closer to the goals. But it can sometimes feel like you are stuck on the bottom rung, where you are not growing your savings fast enough.

With a CD ladder, you can maintain regular access to your funds and still benefit from the higher yields. Here’s how the strategy works.

What is a Certificate of Deposit (CD)?

A CD is a deposit that pays a fixed rate on your cash for a preset time period.

Unlike high-yield savings accounts, the money you deposit in a CD must stay in the account for a specific amount of time, which usually lets you earn a higher interest rate. This timeframe can last anywhere from a few months to several years.

CDs are a great option when you have extra cash you don’t need right away. But what if you think you might need access to some of your cash down the road, or want more steady access to it? That’s where CD laddering comes in.

How does a CD ladder work?

CD laddering is a strategy where you spread your investment across multiple CD terms to access some of your money each time one of your CDs matures.

To build a CD ladder, you split your total funds across multiple CDs with staggered maturity dates. Once each CD matures, you can either withdraw your funds or reinvest them into a new CD. You continue to reinvest to build a CD ladder, with staggered maturity dates for each CD.

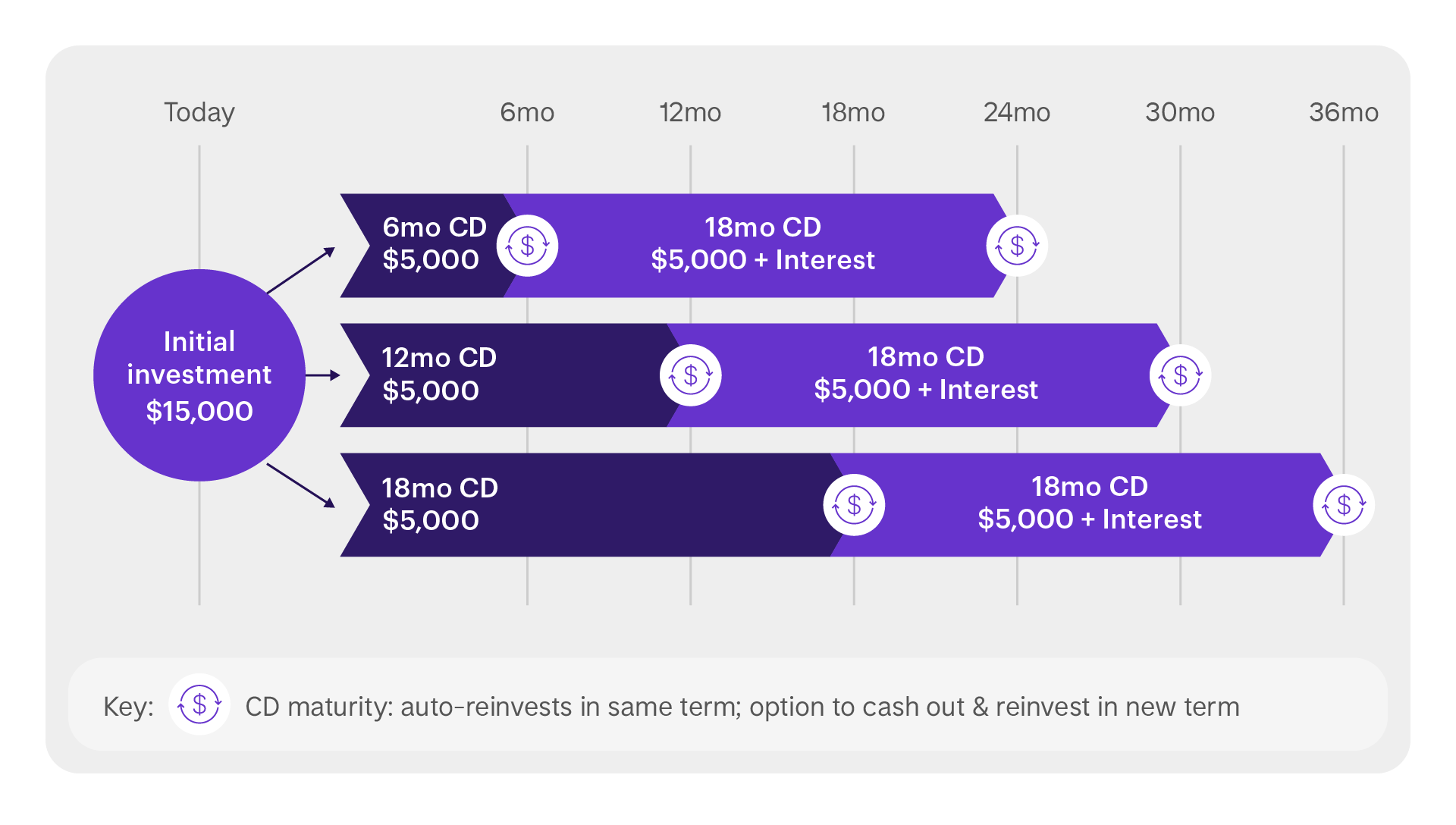

Example of a CD ladder

Consider that you have $15,000 to build a CD ladder. You start by spreading your money evenly across three CDs with maturities of 6, 12, and 18 months. Each CD earns its own annual percentage yield (APY), creating a structured approach to balance growth and liquidity.

- $5,000 in a 6-month CD

- $5,000 in a 12-month CD

- $5,000 in a 18-month CD

Once the 6-month matures, you can either cash out your $5,000 plus interest or reinvest into a new 18-month CD, keeping your ladder going. As the other two CDs mature, you repeat the same process. Once that is complete, you will have three high-yield 18-month CDs maturing every six months.

For illustrative purposes only

What are the benefits of a CD ladder?

A CD ladder can help you get more out of your cash by taking advantage of the potentially greater returns of a long-term CD, while providing you access to some of your cash sooner.

With a CD ladder, you get:

- Predictable access to your funds: CDs that mature at regular intervals can help you pay for upcoming expenses and reach savings goals.

- Greater diversification: CD laddering helps you diversify your cash so that you aren’t locked into a single maturity date or interest rate. This reduces the risk of getting locked into a non-competitive rate while keeping your cash fully invested.

- Protection from interest-rate risk: Unlike savings account APYs, which can go up or down, Bank CDs maintain the same interest rate throughout their duration.

- Long-term interest: Laddering lets you take advantage of the potentially greater returns of long-term CDs, while maintaining the accessibility of a short-term CD. Even when short-term interest rates for CDs are higher than long-term CD rates, the longer-term CDs will have more time for compounding interest to work in your favor and boost returns.

A step-by-step guide to building your CD ladder

Building a CD ladder is easy. Here’s how to create a CD ladder:

- Choose your total investment amount. This should be cash you don’t need immediate access to.

- Pick your ladder structure based on your financial goals. For example, using a three-rung CD ladder means you could have one CD maturing every year for the next three years, or you could have a ladder with 6-, 12-, and 18-month CDs (maturing every 6 months).

- Open accounts. You’ll need to open a new Bank CD account for each time period (e.g., 12 or 6 months). Open account

- Divide your funds as you see fit. For example, if you have $15,000 to invest, you might initially divide it into three CDs of $5,000 each, with respective terms of,12-, 24-, and 36-months.

- As each CD matures, reinvest. After one year, your first CD matures. You can either withdraw the funds or reinvest into a new 36-month CD, maintaining the ladder structure.

- Track and adjust as needed. Your ladder can evolve over time. If rates rise or your goals change, you can adjust reinvestment decisions accordingly.

Planning tips for building a smart CD ladder

Here are a few tips to help you build a CD ladder that works for you:

- Consider when you might need the cash. Match your CD maturities to any known expenditures. For example, if you are positioning some cash for a house down payment in the next five years, structure the ladder to fully mature then, while building in maturity checkpoints along the way for flexibility.

- Make sure you have enough liquidity. An early withdrawal of a bank CD will typically incur a penalty. Make sure you keep your emergency fund in an account that is immediately accessible, such as in a high-yield savings account.

CRC# 5459434 05/2026

How can E*TRADE from Morgan Stanley help?

Certificates of Deposit (CD)

Now, lock in 4.40% Annual Percentage Yield1,2 for 12 months for a limited time

Secure a fixed rate when you open and fund a new Bank CD. Additional terms available from to .3

Morgan Stanley Private Bank, Member FDIC.

Learn about Brokered CDs

Brokered CDs can help investors find competitive interest rates for their cash that includes FDIC coverage from hundreds of banks all over the country.

Premium Savings Account

Boost your savings with a guaranteed 4.00% Annual Percentage Yield for 6 months5

With rates 10X the national average6 and FDIC-insured up to $500,000;7 certain conditions must be satisfied.

Morgan Stanley Private Bank, Member FDIC.