Understanding required minimum distributions (RMDs)

Morgan Stanley Wealth Management

06/26/25Summary: Required minimum distributions (RMDs) are likely to play an important role in your finances in retirement. Planning ahead for what you want to do with the money may help reduce taxes and increase options for re-investing. Here’s what you should know.

1. What is an RMD?

If you have a Traditional, Rollover, SEP, SAR-SEP, or SIMPLE IRA, the federal tax laws require you to withdraw an RMD from the account by December 31 each year, beginning with the calendar year in which you turn “RMD Age”:

- 70 ½ (if you were born before July 1, 1949),

- 72 (if you were born after June 30, 1949, but before 1951),

- 73 (if you were born after 1950, but before 1960), or

- 75 for all others.

On the other hand, if you have a 401(k), Profit Sharing, or Money Purchase Plan, AND own less than 5% of the company you work for, you do not have to take a withdrawal until you turn RMD Age or retire, whichever is later.

If you’re the owner of a Roth IRA or a participant in a designated Roth account under a qualified retirement plan (such as a 401(k) plan), you are not subject to an RMD with respect to that Roth IRA or designated Roth account. You can leave money in the account without taking withdrawals for as long as you live since Roth IRAs and designated Roth accounts (starting in 2024) do not require withdrawals until after the death of the account owner.

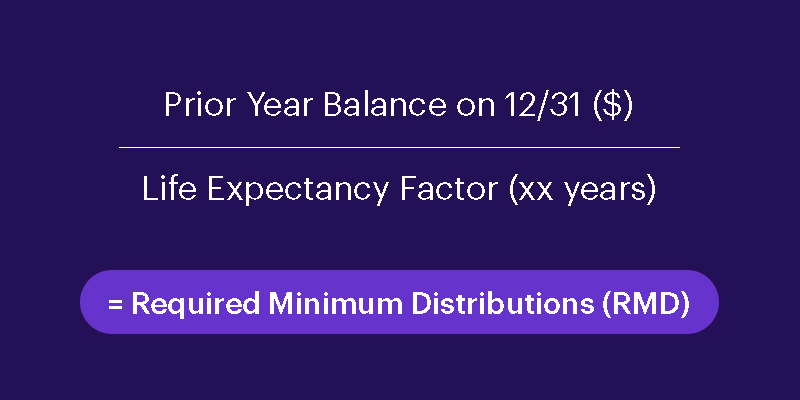

2. How is the RMD calculated?

In general, the amount of an RMD is based primarily on two factors: the account balance and a life expectancy factor. To calculate your RMD, you divide the prior year’s account balance by the applicable IRS life expectancy factor based on your age that year.

Your life expectancy factor is taken from the Uniform Life Expectancy Table which assumes that RMDs are based on the lives of an IRA owner and a beneficiary who is 10 years younger.

However, if your spouse is more than 10 years younger, and is the sole primary beneficiary of the account, you can generally use the Joint Life Expectancy Table, which may result in a lower RMD amount.

Your marital status is determined as of January 1 of each distribution calendar year and, therefore, changes in marital status (such as the death of your spouse) occurring after January 1 generally will not prevent your spouse from being considered the sole beneficiary of your IRA for that year.

3. When should I take my RMD?

In general, the deadline for taking RMDs is December 31 each year. You may want to consider taking your RMD sooner than later to help avoid potential penalty taxes for failure to take the RMD on a timely basis.

However, you may delay taking your first RMD (and only your first RMD) until April 1 of the year after you turn the RMD age (or, for participants in a qualified retirement plan who is not at least a 5% owner, retire from employment with the plan sponsor, if later). If you choose to delay your first RMD, you'll have to take your first and second RMD in the same year (which could result in unintended tax consequences, e.g., push you into a higher tax bracket on a portion of your taxable income for the year).

4. What if I forget to take my RMD?

Forgetting to take an RMD or receiving the full amount may result in the IRS imposing a penalty tax on the amount not distributed as required. If you fail to take an RMD or don’t take enough, you should consult with and rely on your own tax advisor to determine what remedial steps you should take to address such failure.

To avoid potential penalties, you may want to automate withdrawal payments by completing an IRA distribution form online (log-in required) to satisfy the RMD on a monthly, quarterly, or annual basis.

5. What can I do with the RMD money?

Let’s say your pension or other income covers your expenses for the year. If that’s the case, here are some ideas on how you might want to put that RMD to work:

- Reinvest in a taxable brokerage account. If you would like it invested for you, a Core Portfolios account may be an option.

- Contribute to a 529 Education Savings Plan for a grandchild or loved one.

- Use it towards a major purchase like a vacation, new car, new roof or even a more energy-efficient furnace.

- Support causes that matter to you by making a charitable donation through a qualified charitable distribution (QCD).1

6. Do I have to take my RMD from my IRA if I’m still working?

When you reach RMD Age, you must withdraw the RMD amount by April 1 of the following year, even if you’re still working. You’re then required to take another withdrawal from your IRA by December 31 of that year and every year thereafter. This applies to Traditional, SEP or SIMPLE IRAs.

If you own a Roth IRA, RMDs don’t apply during your lifetime (but RMDs do apply after your death). The qualified retirement plan rules regarding RMDs are different so check with your plan administrator to determine when you are required to take an RMD.

7. What if I own multiple IRAs?

You must calculate your RMD for each IRA separately. Then, you can:

- Withdraw an RMD from each account. Or, you can add up the RMD amount from each IRA (but not RMDs from qualified retirement plans, such as a 401(k) plan) and withdraw the aggregate amount from only one IRA (other than Roth IRAs or Inherited IRAs).

- Alternatively, you may want to consider consolidating IRAs that are subject to an RMD into one account. By consolidating IRAs, you’ll only need to calculate and withdraw an RMD from one account each year.

While RMDs don’t apply during your lifetime if you own a Roth IRA, they will apply to your beneficiaries after your death. Be sure to designate beneficiaries on your retirement accounts if you haven’t already.

8. What happens to RMDs when an owner passes away?

When you are the beneficiary of a retirement plan or an IRA, there are specific rules that regulate the minimum withdrawals that must be taken. The after-death RMD rules are complex and depend on the identity of the beneficiary (e.g., spouse beneficiary, individual beneficiary who qualifies as an eligible designated beneficiary, individual beneficiary who does not qualify as an eligible designated beneficiary, an entity, such as a trust or estate, etc.).

Generally, the first year that beneficiaries must take a withdrawal from an IRA is December 31st following the year the original account holder passed away. However, if the plan participant or IRA owner died before taking their full RMD for the year of death, a beneficiary would need to receive the undistributed portion of the year of death RMD.

For example, if an IRA owner passed away on February 1, 2025, the beneficiary would need to take his or her first withdrawal by December 31, 2026. However, if the original owner was over age 72 at the time of death and had not yet withdrawn an RMD for 2025, the beneficiary would also be required to withdraw that amount before the end of 2025.

To learn more, visit our Inherited IRA page and if you’re a client, our Inherited IRA RMD Calculator.

Final thoughts

When it comes to RMDs, different people have different opinions. Some look forward to making their withdrawals, while others absolutely dread it.

If you are lucky enough to not need funds from the IRA, there are a number of options you may be able employ to put that RMD to work. And remember, you can always withdraw more than the minimum if necessary.

Navigating the complexities of RMDs can be challenging. Visit our RMD Resource Center (log-in required), which includes FAQs, which provides helpful information on RMDs.

Article Footnotes

1 Ongoing SIMPLE and SEP IRAs (including SAR-SEP IRAS) are not eligible for QCDs. An SEP or SIMPLE IRA is considered ongoing if the employer made a contribution (including a salary reduction contribution to a SAR-SEP or SIMPLE IRA) for the year in which the QDC would be made. If you make a tax deductible IRA contribution after age 70 ½, the amount you can exclude from your taxable income as a QCD generally will be reduced. Work with your Tax Advisor to ensure that you satisfy all the QCD requirements and that QCDs have been correctly reported on your tax return.

CRC# 3976290 11/2024

How can E*TRADE from Morgan Stanley help?

Traditional IRA

You may be eligible to make income tax deductible contributions

Earnings potentially grow tax-deferred until you withdraw them in retirement.

Rollover IRA

Consider rolling over your old 401(k) plan assets to an E*TRADE from Morgan Stanley IRA

Consolidate assets from a former employer’s retirement plan.

E*TRADE CompleteTM IRA

For retirement investors over age 59½

Upgrade your account for flexible access to cash with free checking, online bill pay, and ATM/debit cards.1,2

Premium Savings Account

Boost your savings with a guaranteed 4.00% Annual Percentage Yield for 6 months3

With rates 10X the national average4 and FDIC-insured up to $500,000;5 certain conditions must be satisfied.

Morgan Stanley Private Bank, Member FDIC.