Four things you should consider before rolling over your 401(k)

E*TRADE from Morgan Stanley

10/22/25Individual Retirement Accounts or IRAs are tax-deferred vehicles that can generally accept a rollover of assets from a qualified retirement plan. Here are some things you should consider ahead of deciding whether to roll over your retirement savings.

Congratulations! Whether you are on your way to a new job or reaching an employer-sponsored retirement, there’s quite a bit you may want to consider regarding your employer-sponsored qualified retirement plan assets. The good news: You may be able to take your retirement savings with you without having to pay income taxes or tax penalties.

Rolling over your employer-sponsored qualified retirement plan assets: your options

It’s good to know you have options. When you leave a job, you can typically take one of the following actions with your employer-sponsored qualified retirement plan assets, the most common of which is a 401(k):

- Leave assets in the old plan. Simply do nothing and leave your retirement savings with your old employer (if permitted). Just know you won’t be able to add additional funds to this account. And since you’re no longer an employee, plan management or administration fees, as well as fees on trades, may apply.

- Cash out your assets. Choosing to cash out prior to age 59 ½ from your retirement plan counts as an early distribution. This means that, in addition to being subject to income taxes, your distribution may be subject to a 10% early withdrawal penalty tax, so cashing out before 59 ½ is generally avoided. Plus, you’ll be subject to a mandatory 20% federal income tax withholding and possibly state income tax withholding, depending on where you reside.

- Rollover to your new employer’s plan. You may be able to move assets from your former employer’s qualified retirement plan into your new employer’s qualified retirement plan. Possible advantages include the potential of reduced fees and costs. You can generally continue contributing. And, depending on the new plan, you may be able to take a loan against your accumulated retirement assets in the plan. FYI, you may have a waiting period before you can start to contribute to your new plan.

- Rollover your 401(k) to an IRA. You can continue to save for retirement when you roll over your retirement assets from your former employer’s qualified retirement plan (e.g., 401(k) plan) to an Individual Retirement Account (IRA). While most IRAs offer a variety of investment options, they might not offer the same options as an employer plan. And, with an IRA, you cannot take a loan against your assets.

Also, you may want to compare the cost of opening and maintaining an IRA account with that of leaving your assets in your former employer’s qualified retirement plan and/or rolling over your assets to a new employer’s qualified retirement plan.

When done correctly, rolling over your retirement assets from your former employer’s qualified retirement plan to an IRA or another employer’s qualified retirement plan can help you to continue to defer taxes on the growth of your retirement assets compared to withdrawing the funds from your former employer’s qualified retirement plan and then reinvesting them in a taxable account. However, there are rules to consider.

Two ways to rollover: direct or indirect

In general, you can move retirement assets that are eligible for rollover from a qualified retirement plan (such as a 401(k) or 403(b) plan) to an IRA without being subject to immediate taxation. Rollovers into IRAs typically will not result in income taxes or tax penalties to the participant if Rollover rules are followed. Before making the decision to rollover your qualified retirement plan assets into an IRA, it’s important to understand the difference between the two types and identify which one works best for you:

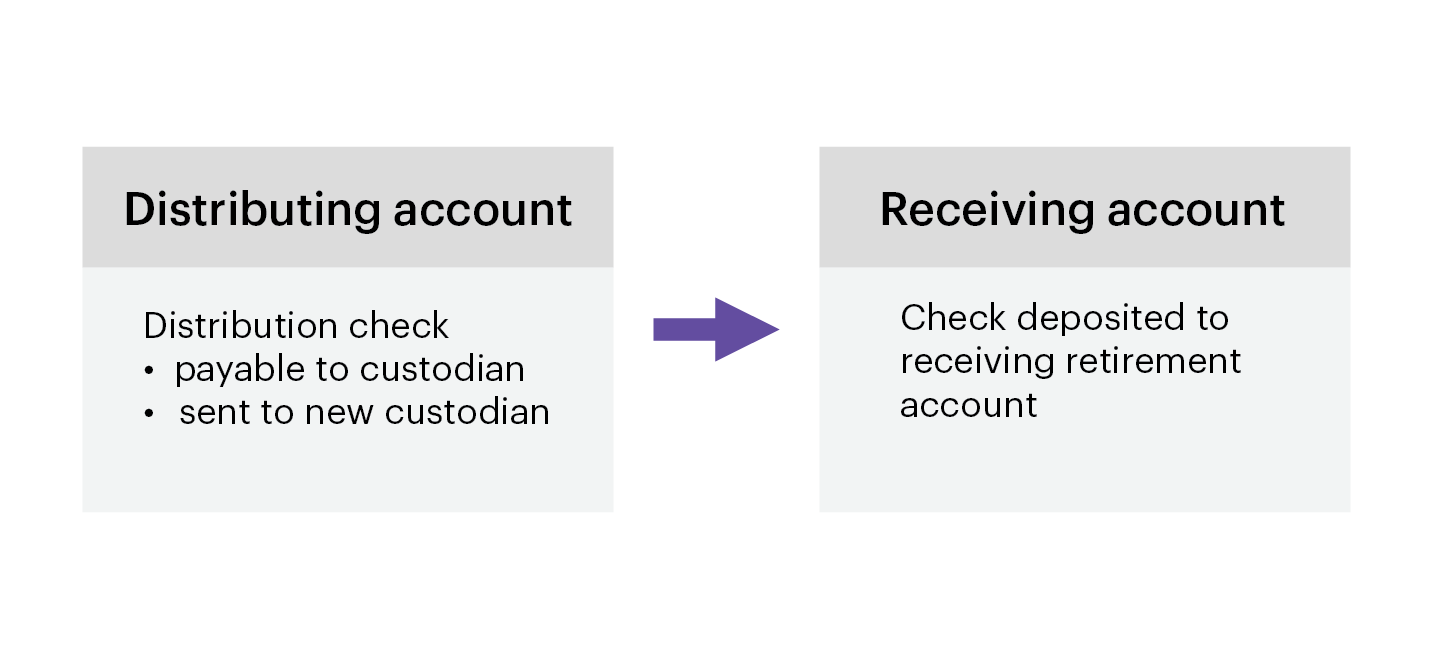

- A direct rollover is the easiest way to move money between retirement plans/accounts. You simply have your former employer make a distribution payable to the custodian of your IRA for credit to your IRA (e.g., distribution check payable the custodian of your IRA for the benefit of your IRA). If processed correctly, a direct rollover is nontaxable.

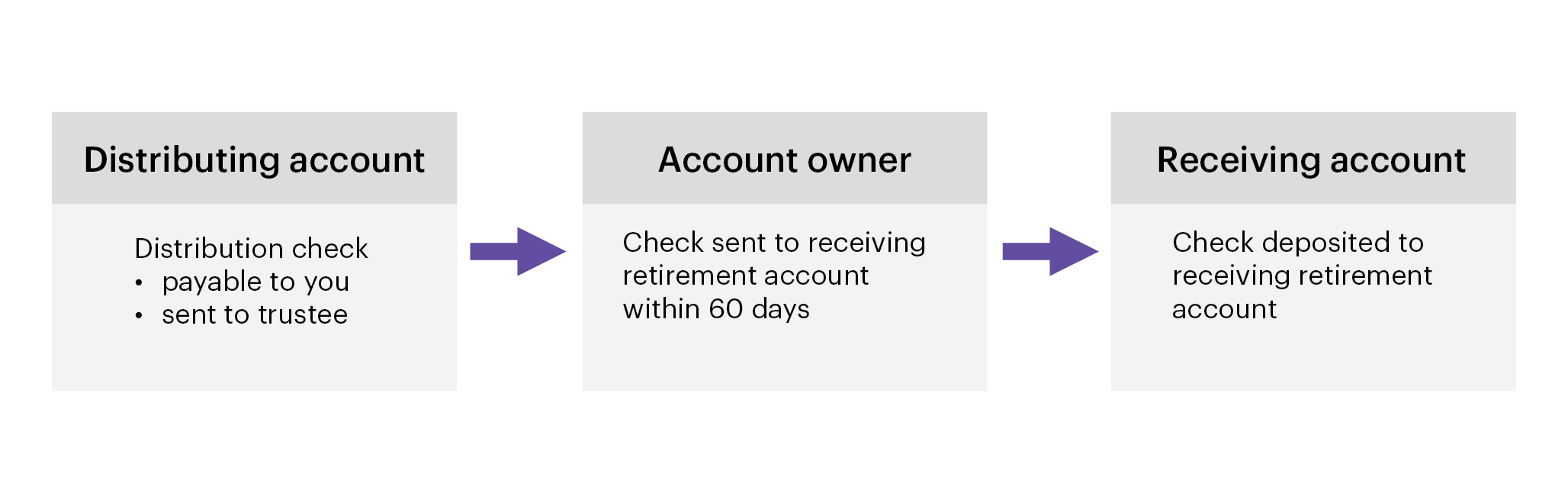

- An indirect rollover means the distribution gets paid directly to you (e.g., distribution check payable directly to you). It is then up to you to deposit the funds into your IRA no later than 60 days after you receive the distribution. Your distribution will generally be subject to mandatory 20% federal income tax withholding. If you decide to keep some, or all of the funds, or you don’t deposit the amount distributed (including any amount withheld for taxes) into an IRA (or other qualified retirement plan) within that time period, you will have to pay income tax on the amount you don’t deposit. If you’re under the age of 59½, you will have to pay an additional 10% distribution penalty tax.

Trustee-to-trustee transfers

- A trustee-to-trustee transfer is a transfer of funds from one trustee directly to another. Unlike rollovers, trustee-to-trustee transfers are not allowed between different retirement account types. For example, an investor is not allowed to transfer assets from a 401(k) to an IRA, but an IRA to an IRA transfer is permitted.

Trustee-to-trustee transfers are not taxable at the time of the transfer, since there is no distribution to the account owner and they are exempt from one-rollover-per-year rule for IRA to IRA rollovers, since they are not considered rollovers.

To get further help understanding the above options or all options available with a former employer’s plan, feel free to call 800-387-2331 for step-by-step assistance with rollovers or transfers.

Getting the ball rolling

Preparing for a new job or retirement can be challenging but rolling over your workplace qualified retirement plan to an IRA doesn’t have to be. At E*TRADE, you can roll over your retirement savings in three steps1:

- Open an E*TRADE IRA online in about 15 minutes

- Roll over your former employer’s qualified retirement plan assets

- Choose investments

If all or a portion of your rollover is coming from a designated Roth account (e.g., Roth 401(k) account, Roth 403(b) account or Governmental Roth 457(b) account), then you will need to open a Roth IRA to receive your designated Roth account assets.

Article Footnotes

1 Some rollover situations may require additional steps. If your situation is a little more complicated (for example, splitting assets between a traditional and Roth IRA or transferring company stock), give us a call (800-387-2331). We’ll be glad to walk you through exactly what to do.

CRC# 4886275 10/2025

How can E*TRADE from Morgan Stanley help?

Roll over your retirement assets with Capitalize

E*TRADE has partnered with Capitalize to make rolling over an old 401(k) quick and easy. They can help you navigate the rollover process for funding your E*TRADE IRA.

Rollover IRA

Roll over your former employer’s qualified retirement plan.

Explore our rollover tool

Our interactive tool can help you understand your options.