What’s your retirement spending reality?

Morgan Stanley Wealth Management

06/26/25Summary: Everyone has a different idea of their dream retirement. Whatever you envision, it’s essential to plan ahead so that your nest egg will last.

What do you envision for your retirement? Traveling the world? Frequently entertaining friends and family at home? Delving into pastimes you had little leeway for during your working years? Whatever your pursuits, it’s essential to plan ahead for your spending needs to help ensure that you can afford your dream retirement.

Dan Hunt, Senior Investment Strategist at Morgan Stanley Wealth Management, leads a team who examines how spending tends to evolve over the course of retirement and how lifestyle choices can affect retirement readiness. One thing they have consistently found: Spending rarely stays constant in this stage of life.

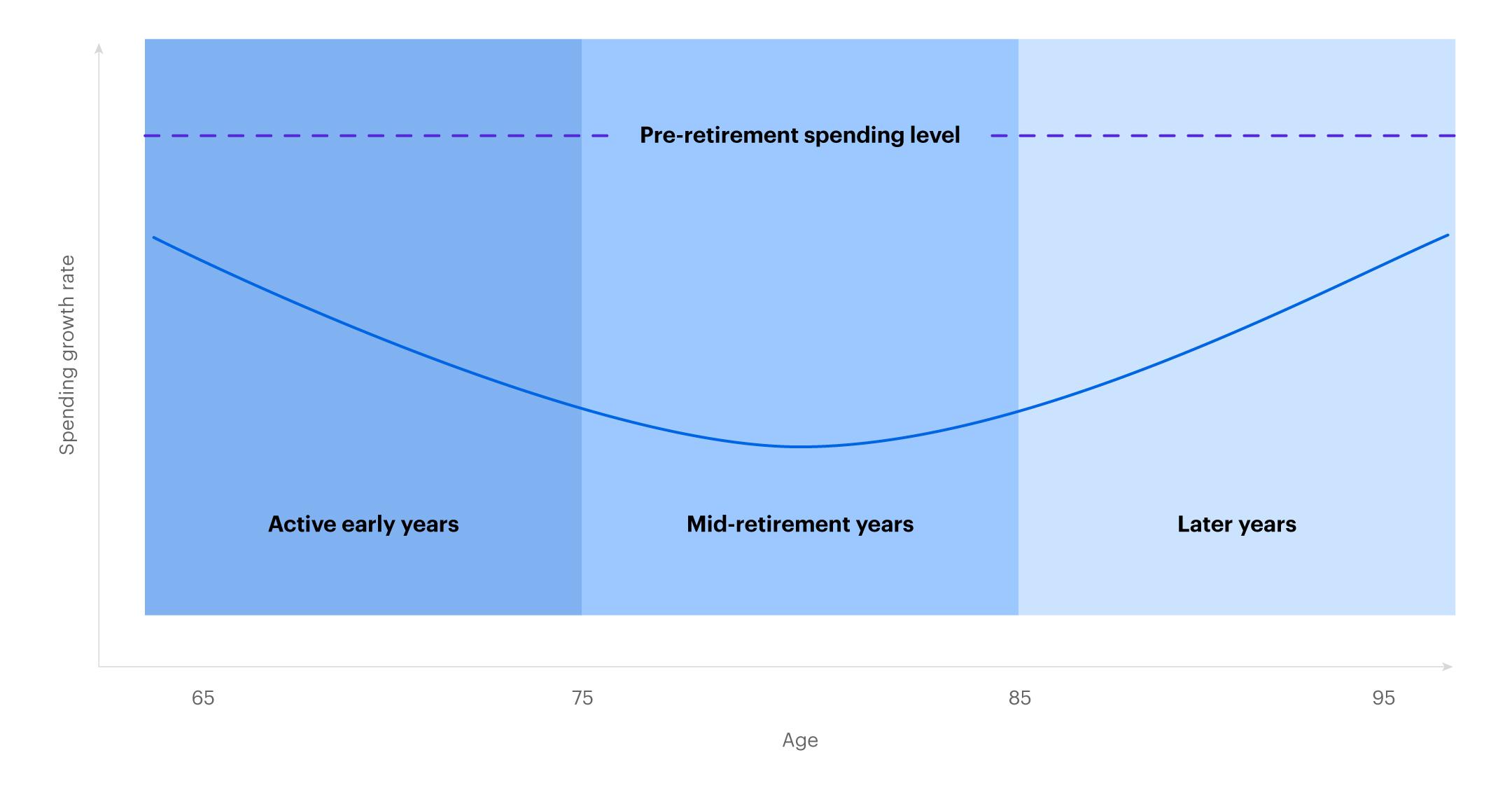

What retirement looks like today

Some investors may assume that planning for retirement means replacing a salary, while perhaps accounting for increases in the cost of living due to inflation. In reality, retirement spending typically varies substantially over three distinct phases:

- The active early years of retirement when spending rates are highest but gradually decline with age.

- The mid-retirement years when activity slows and spending rates are lowest.

- The later years when medical and long-term care needs cause spending rates to rise again.

To be sure, spending choices in retirement have many individual variations, but the “retirement spending smile” is a pattern that describes the lived experience of many households, and can help retirement savers build a plan that better reflects their anticipated needs.

The Retirement Spending Smile

Spending tends to evolve over the course of retirement

Source: Morgan Stanley Wealth Management as of June 2019

Six common retirement lifestyles

Of course, no two retirements look alike. One person’s idea of a “dream retirement”—and the associated costs—may be very different from someone else’s. That’s why it’s essential to plan ahead, with an eye toward your unique lifestyle preferences and spending needs.

To explore this idea further, we created six hypothetical retiree profiles and then used financial modeling to test how each retiree’s unique habits would affect their retirement readiness.

Specifically, we looked at:

- Home Hobbyists spend heavily on home remodeling and may also pursue other pastimes, such as restoring antique cars or donating to community projects, resulting in above-average spending early on.

- Entertainers spend more of their income on food and beverages to entertain friends and family at home. Their overall spending tends to decline more rapidly early in retirement than other groups.

- Globetrotters spend a large fraction of their budget on travel prior to retiring. Once they retire and have more free time, travel expenses increase even more, especially in the early and middle years of retirement.

- Early Birds live by the motto “you only live once.” Early Birds tend to retire early, and have higher spending rates, especially on travel and entertainment.

- Health-Care Spenders use a significant share of their disposable income on higher insurance premiums for supplemental policies, prescription-drug expenses, and special treatments in excess of insurance coverage.

- Average Retirees set the benchmark by which the other five types can be compared. Their spending most closely resembles the “retirement spending smile.”

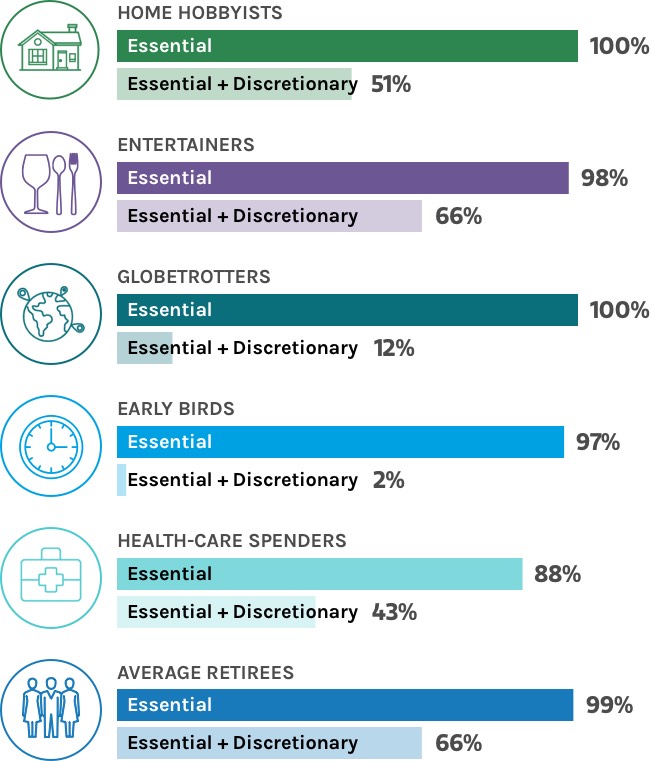

Retirement spending outcomes: Best and worst

How did each hypothetical retiree make out in their modeling?

Assuming everyone starts retirement with a $2 million tax-qualified retirement account, 60% in stocks and 40% in bonds, could they successfully cover their costs? The good news is that all six retiree types had a very high likelihood of being able to cover their essential expenses, such as food and housing, throughout retirement. However, some hypothetical retirees had an easier time than others affording both their essential and discretionary expenses.

The probability of success in retirement

This graph is for illustration purposes only and may or may not reflect the probability of success in retirement

Source: Morgan Stanley Wealth Management, as of June 2019. Assumes a $2 million tax exempt portfolio invested 60% in stocks and 40% in bonds.

- Due largely to their more modest spending habits, Average Retirees and Entertainers fared best, each with a 66% chance of being able to cover the total cost of their desired lifestyle throughout retirement.

- Home Hobbyists and Health-Care Spenders, respectively, had a 51% and 43% likelihood of being able to sustain their lifestyle throughout retirement.

- However, Globetrotters and Early Birds may have to take a hard look at their spending plans. Their probability of covering all of their retirement expenses was only 12% and 2%, respectively, due to their much higher spending in early and middle retirement, with the Early Birds facing the added challenge of a longer retirement and having to pay health insurance premiums out-of-pocket until they become eligible for Medicare at age 65.

Strategies to prepare for any retirement style

No matter your retirement lifestyle, there are steps anyone can take to increase the odds of a successful retirement. Here are three steps, that the team particularly points to, for retirees who spend more heavily:

| Part-time work in early retirement Taking on a home-based gig can help retirees boost their savings, while also keeping the mind engaged. |

| Belt-tightening Cutting back on nonessential expenses if investments underperform can give a portfolio the space it needs to recover and grow. This approach may be necessary for higher-spending retirees. |

Time-segmented bucketing With this approach, investors allocate assets into three pools of spending, reflecting the three phases of retirement. Each pool is then invested based on investor risk preferences for the time horizon of each phase. For example, investors might consider allocating funds for shorter-term early-retirement expenses in more conservative assets, while initially investing funds for later years in more aggressive growth assets. |

The bottom line: If you’ve saved diligently and made strategic investment decisions5 during your working years, a dream retirement is within reach—but it’ll likely require careful planning and, for some retirees, a willingness to make certain tradeoffs to make your dream a reality.

The source of this article, What Kind of Retiree Do You Want to Be?, was published on March 14, 2024.

CRC# 3992356 01/2025

How can E*TRADE from Morgan Stanley help?

Plan for your future

Explore easy-to-use planning tools and resources—designed to help you take control of your financial future.

E*TRADE CompleteTM IRA

For retirement investors over age 59½

Upgrade your account for flexible access to cash with free checking, online bill pay, and ATM/debit cards.1,2

Roth IRA3

Tax-free growth potential retirement investing

Pay no income taxes or tax penalties on qualified distributions if you meet certain requirements.

Certificates of Deposit (CD)

Now, lock in 4.40% Annual Percentage Yield4,5 for 12 months for a limited time

Secure a fixed rate when you open and fund a new Bank CD. Additional terms available from to .6

Morgan Stanley Private Bank, Member FDIC.