Market rides trade thaw

- Tech leads “risk-on” week, SPX and NDX up for year

- Traders embrace tariff pause, inflation still cool

- This week: retail and tech earnings, new home sales

Last Monday may have provided most of the week’s stock-market fireworks, but bulls managed to keep the celebration going until Friday.

The S&P 500 (SPX) jumped 3.3% last Monday after news of a 90-day pause in US-China tariffs, building on that gain amid cool inflation data and signs of continued labor-market strength. By the time the closing bell rang on Friday, the SPX had logged third-best week since November 2023 (the second-best occurred five weeks ago), and the index was back into positive territory for the year:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: S&P 500 ends week within 3% of all-time high.

The fine print: The market’s mood change last week may have been most apparent in its non-response to Friday’s weak consumer sentiment reading, which came in at its lowest level (50.8) since June 2022. That reaction was much different from the sharp sell-offs that followed some of the downside surprises in consumer sentiment and confidence numbers in February and March.

The number: 0.2%, the Consumer Price Index’s (CPI) smaller-than-expected inflation increase, reported last Tuesday. The Producer Price Index (PPI) also came in cool, as did weekly jobless claims. The outlier: retail sales, which were weaker than expected.

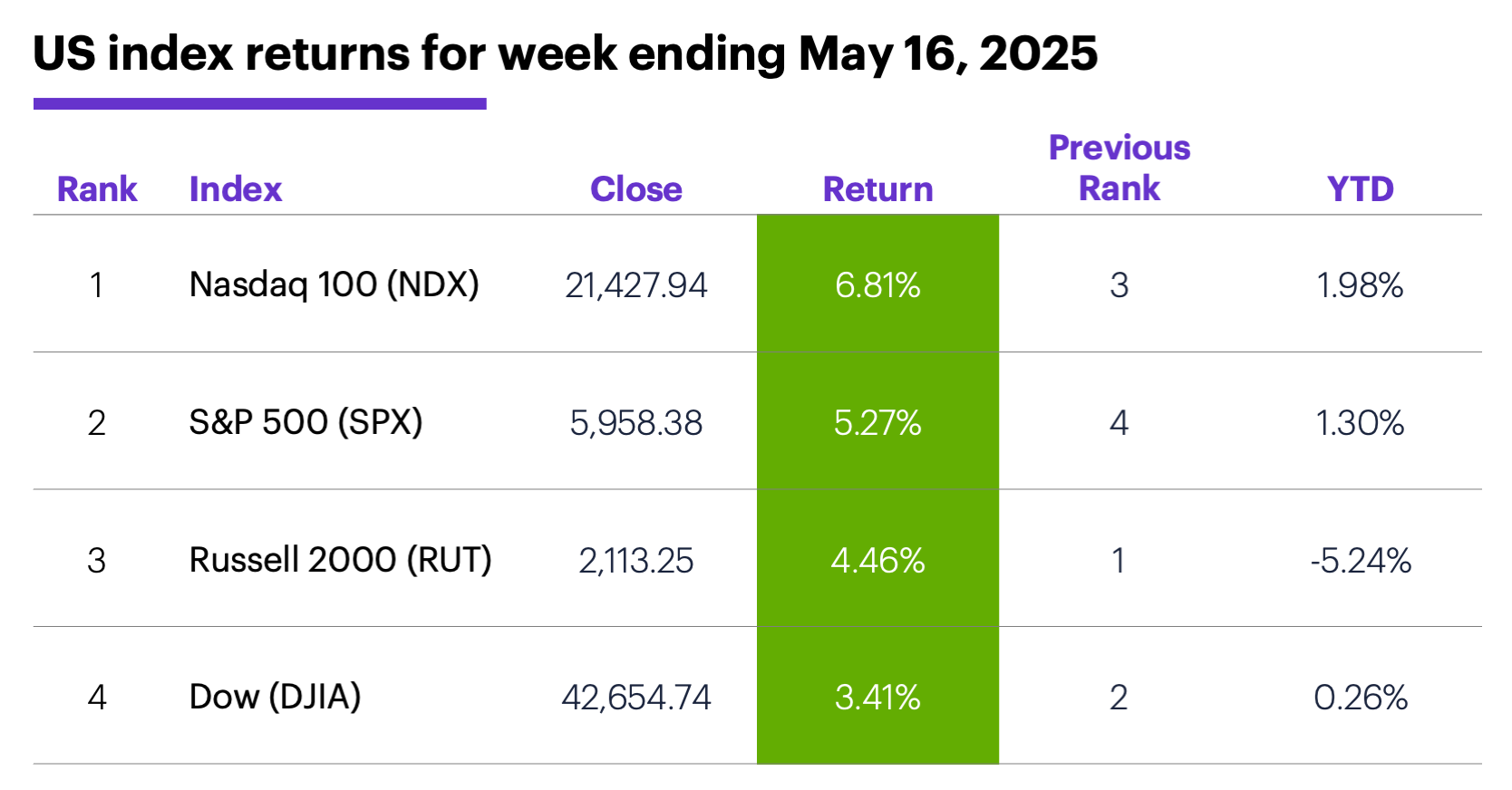

The scorecard: The Nasdaq 100 (NDX) tech index led the market and, along with the SPX and the Dow, ended the week up for the year:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were tech (+7.9%), consumer discretionary (+7.5%), and communication services (+6.4%). The weakest sectors were health care (-0.01%), real estate (+0.8%), and consumer staples (+1.5%).

Stock moves: Bakkt Holdings (BKKT) +47% to $14.75 on Tuesday, Foot Locker (FL) +86% to $23.90 on Thursday. On the downside, Perpetua Resources (PPTA) -23% to $11.74 on Monday, Halozyme Therapeutics (HALO) -25% to $50.23 on Tuesday.

Yields: The benchmark 10-year Treasury yield hit its highest level (4.53%) since February 19 last Wednesday, then pulled back to end the week up 0.07% at 4.44%.

US dollar: The US Dollar Index (DXY) climbed 0.75 to 101.09.

Futures: After closing at it its highest level ($63.20) in more than five weeks last Tuesday, July WTI crude oil (CLN5) pulled back to end the week up $1.39 at $61.97. June gold (GCM5) fell to a five-week low last week, ending the week $146.70 lower at $3,187.30. Biggest up moves: July cocoa (CCN5) +18.6%, May ether (ETHK5) +10.5%, May Micro ether (METK5) +10.5%. Biggest down moves: June VIX (VXM5) -12%, July natural gas (NGN5) -10%, July coffee (KCN5) -5.7%.

Coming this week

This week’s numbers include:

●Monday: Leading Economic Indicators Index

●Thursday: Chicago Fed National Activity Index, S&P Global Manufacturing and Services PMIs (flash), existing home sales

●Friday: new home sales

This week’s earnings include:

●Monday: Zim Integrated Shipping (ZIM), Agilysys (AGYS), Trip.Com (TCOM)

●Tuesday: Eagle Materials (EXP), Home Depot (HD), Keysight Technologies (KEYS), Palo Alto Networks (PANW), Toll Brothers (TOL), XP (XP)

●Wednesday: Dycom (DY), Lowe's (LOW), Target (TGT), TJX (TJX), E.L.F. Beauty (ELF), Snowflake (SNOW), Urban Outfitters (URBN), Zoom Communications (ZM)

●Thursday: Advance Auto Parts (AAP), Analog Devices (ADI), BJ's Wholesale Club (BJ), Ralph Lauren (RL), Copart (CPRT), Intuit (INTU), Ross Stores (ROST), Workday (WDAY)

●Friday: Booz Allen Hamilton (BAH), Buckle (BKE)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Catching up on a correction

The ride has been fast, both ways.

Just as the S&P 500 correction that began on March 13 unfolded more quickly than most others over the past four decades, the market’s rebound off its April low has been equally impressive.

If the SPX hits a new record high (above 6,144.50) before it closes below the April 8 low of 4,982.77, that means the correction would have reached its bottom in 18 trading days—the fourth-fastest descent to a correction low (except for two corrections that ended the same day they began).

And although in April the SPX twice dipped into bear-market territory on an intraday basis (20% below its February 19 record close), it never closed more than 18.9% below that high. If this turns out to be the move’s maximum decline, it will be the seventh-largest of the SPX’s 14 declines from record highs since 1983.

Finally, as of Friday, it had been 61 trading days since the SPX’s February 19 high. In 12 of the past 14 cases, it took the SPX at least 70 trading days to reach its pre-correction high.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.