Tech leads market back to records

- Market poised to close out June at record levels

- Bond yields drop, oil tumbles from five-month high

- This week: jobs report, Fourth of July holiday

Geopolitical turmoil, signs of economic slowdown, and surging oil prices turned out to be no problem for the US stock market last week, as a rebounding tech sector propelled some of the major indexes to all-time highs for the first time in more than four months.

Although the S&P 500 (SPX) initially fell to a two-week intraday low last Monday after the US followed Israel with airstrikes on Iran, it reversed to close up on the day and marched higher the rest of the week, ultimately logging its first record high since February on Friday:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: New highs for US market.

The fine print: While Friday’s PCE Price Index showed inflation remained moderate, Thursday’s downward revision of Q1 GDP and Friday’s personal spending data highlighted a cooling economy and a more-cautious consumer. On the other side of the sentiment spectrum, on Friday China confirmed the details of its trade deal with the US, while the White House downplayed the significance of the end of the 90-day tariff pause on July 9 (although it also announced it was ending trade talks with Canada).

The move: August WTI crude oil futures (CLQ5) rallied nearly 6% to a new intraday contract high of $78.40 in pre-market trading on Monday (in the wake of the US airstrikes), then ended the day down more than 7% at $68.51.

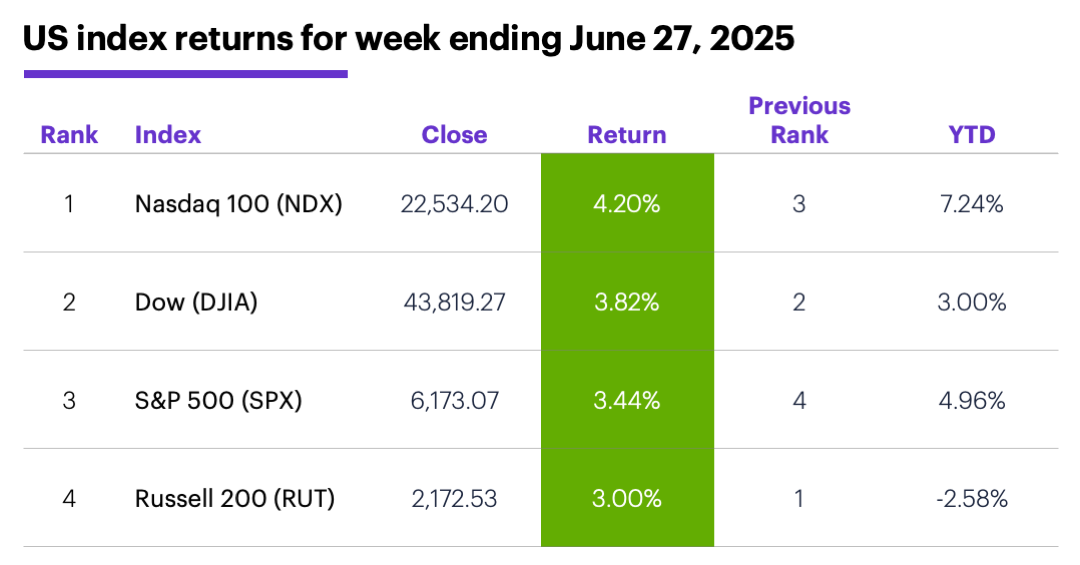

The scorecard: The Nasdaq 100 (NDX) tech index, which hit new record highs along with the SPX and Nasdaq Composite (COMP), led the market:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were communication services (+6.2%), information technology (+4.7%), and consumer discretionary (+4.3%). The weakest sectors were energy (-3.4%), real estate (-0.8%), and consumer staples (+0.4%).

Stock moves: Cidara Therapeutics (CDTX) +114% to $44.95 on Monday, Nektar Therapeutics (NKTR) +156% to $24.45 on Tuesday. On the downside, Hims & Hers Health (HIMS) -35% to $41.98 on Monday, Houston American Energy (HUSA) -31% to $12.83 on Tuesday.

Yields: The benchmark 10-year Treasury yield fell 0.1% to 4.28% last week.

US dollar: The US Dollar Index (DXY) fell to fresh three-year lows, closing the week down 1.31 at 97.40.

Futures: August WTI crude oil (CLQ5) consolidated after its Monday-Tuesday sell-off, ending the week down $8.32 at $65.52. Sharp sell-offs on Tuesday and Friday left August gold (GCQ5) down $98.10 to $3,287.60 for the week. Biggest up moves: September cocoa (CCU5) +9.2%, September palladium (PAU5) +9.2%. Biggest down moves: September Brent crude oil (BU5) -11.5%, August WTI crude oil (CLQ5) -11.3%.

Coming this week

The labor market takes center stage this week. Because US markets are closed Friday for the July 4th holiday, the monthly jobs report will be released on Thursday:

●Monday: Chicago PMI

●Tuesday: Jerome Powell speech, S&P Global Manufacturing PMI, ISM Manufacturing Index, Job Openings and Labor Turnover Survey (JOLTS), construction spending

●Wednesday: Challenger job cuts report, ADP private employment report, vehicle sales

●Thursday: Jobs Report, S&P Global Services PMI, ISM Services Index, factory orders, ISM Services Index

●Friday: US markets closed for July 4th holiday

This week’s earnings include:

●Monday: Progress Software (PRGS)

●Tuesday: Greenbrier (GBX), MSC Industrial Direct (MSM), Constellation Brands (STZ)

●Wednesday: UniFirst (UNF), Franklin Covey (FC)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Bonds lost in the “new record high” shuffle? Last week’s stock market milestones overshadowed an interesting aspect of this year’s market dynamics—the outperformance of bonds vs. equities so far this year. Morgan Stanley Wealth Management thinks short- to intermediate-term Treasuries and investment-grade bonds could continue to outperform stocks in the second half of the year, given the bond market’s current superior yields and a favorable policy backdrop.1

Strong starts to July. The first trading day of July (tomorrow) has been an unusually bullish day for stocks since 1991. It not only had the largest average return of any day of the month (0.49%), it was also the day most likely to close higher (30 of 34 years). The second trading day of July is the only one in the first nine trading days of the month to close down more often than up (29 of 34 years).2 Check back on Wednesday for a deeper dive into July’s historical trading patterns.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 MorganStanley.com.Why Bonds May Keep Beating Stocks. 6/25/25.

2 All figures represent S&P 500 (SPX) closing prices, 1991-2025. Supporting document available upon request.