Stocks approach pre-tariff levels

- Stocks swing—higher—amid shifting Washington narratives

- Tech, consumer discretionary lead “risk-on” charge

- This week: jobs, GDP, Fed inflation, 1,000-plus earnings

Stock market volatility didn’t disappear last week, but given it was mostly the “good kind”—to the upside—few investors were likely complaining.

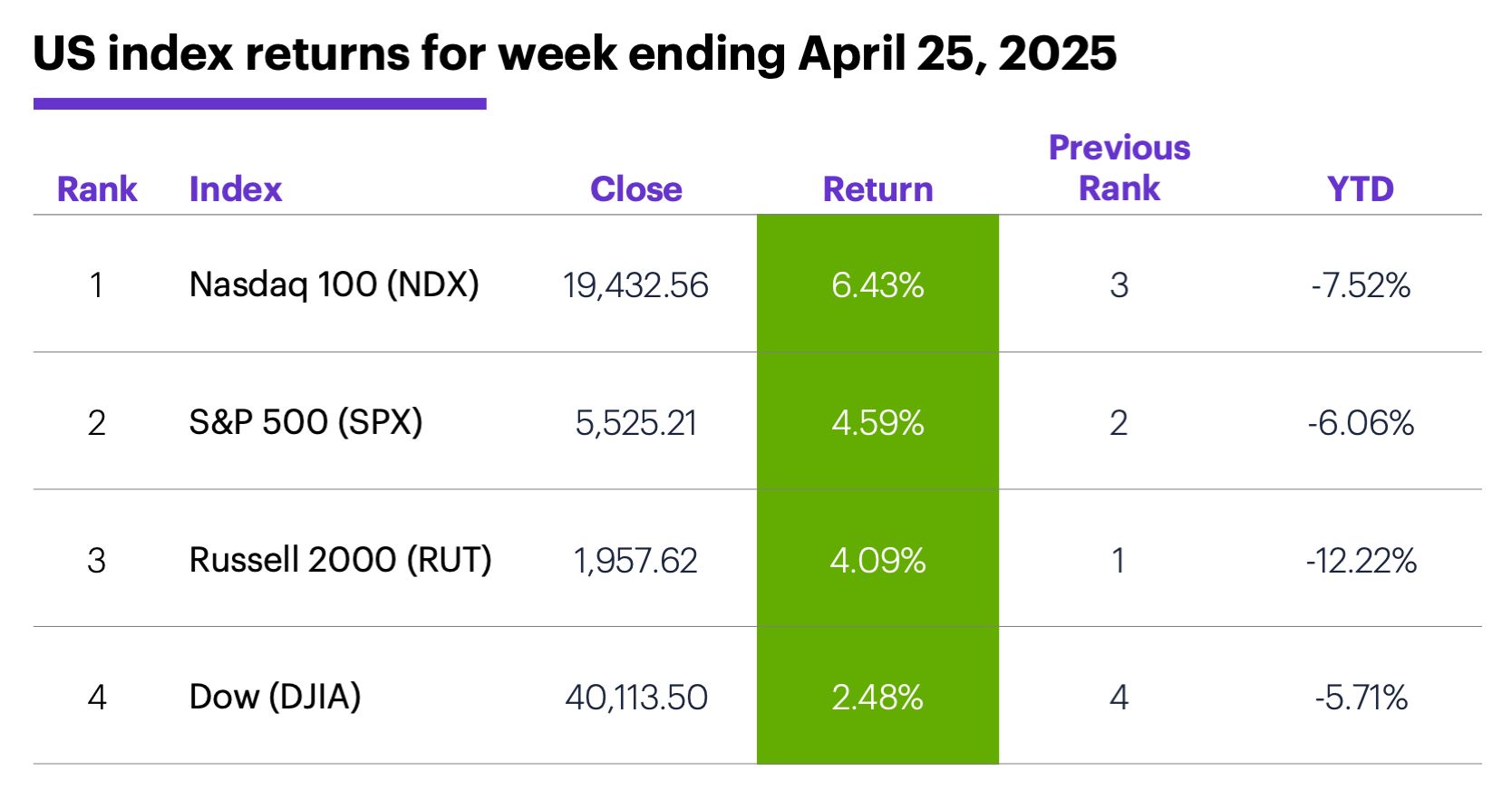

The S&P 500 (SPX) staged its second-biggest weekly gain since November, rallying at least 1.6% on three consecutive days (Tuesday-Thursday) for the first time since 2020. That surge more than offset a sharp Monday sell-off, which unfolded amid concerns that President Trump would attempt to force Fed Chair Jerome Powell out of his position.

Last week’s rally pushed the SPX to test resistance at the level of its early-April tariff breakdown (around 5,500):

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Tech leads “risk-on” charge ahead of key week of data and earnings.

The fine print: The SPX fell more than 3% intraday last Monday as President Trump criticized Powell for not cutting interest rates, raising concerns about an attempt to remove the Fed Chair that could further destabilize financial markets. But on Tuesday, Trump said he had “no intention” of firing Powell, while also suggesting he may lower tariffs on China.1 Also, Treasury Secretary Bessent said he expected a “de-escalation” of trade tensions with China in the “very near future.”

The number: $2.81, Alphabet’s per-share earnings reported last Thursday, handily topping the $2.02 estimate. Earlier in the week, Tesla (TSLA) posted a significant earnings miss. Most of the “Magnificent 7” cohort will release earnings this week.

The scorecard: The Nasdaq 100 (NDX) tech index posted the week’s biggest gain:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were information technology (+7.5%), consumer discretionary (+7.2%), and communication services (+6.1%). The weakest sectors were consumer staples (-1.4%), real estate (+0.3%), and utilities (+0.6%).

Stock moves: Pegasystems (PEGA) +29% to $88.55 and Summit Therapeutics (SMMT) +22% to $33.23, both on Wednesday. On the downside, Summit Therapeutics (SMMT) -36% to $23.465 and Saia (SAIA) -31% to $245.63, both on Friday.

Yields: Bond prices mostly edged higher last week as yields dipped. The benchmark 10-year Treasury yield fell 0.07% to 4.26%—the low of its two-week range.

US dollar: The US Dollar Index (DXY) started out last week by falling to a fresh three-year low of 98.28, then pivoted to end the week up 0.24 at 99.47.

Futures: Gold lost ground after hitting new record highs. June gold (GCM5) pulled back sharply after topping $3,500 (intraday) for the first time last Tuesday, ending the week down $30 at $3,298.40. June WTI crude oil (CLM5) traded mostly sideways, closing Friday down $0.99 for the week at $63.02. Biggest up moves: July cocoa (CCN5) +13.2%, April ether (ETHJ5) +12.8%. Biggest down moves: July orange juice (OJN5) -12.9%, May VIX (VXK5) -11.1%.

Coming this week

It’s a huge week of economic data, with jobs data, Q1 GDP, and Fed inflation (the PCE Price Index) headlining the calendar:

●Tuesday: trade balance in goods (advance), retail inventories (advance), wholesale inventories (advance), S&P Case-Shiller Home Price Index, NAHB House Price Index, Job Openings and Labor Turnover Survey (JOLTS)

●Wednesday: ADP Private Employment Report, Q1 GDP (initial estimate), personal income and spending, PCE Price Index, Chicago PMI, pending home sales

●Thursday: Challenger Job Cuts, S&P Global Manufacturing PMI, ISM Manufacturing Index, construction spending, April vehicle sales

●Friday: Employment Report, factory orders

More than 1,000 companies will be releasing earnings this week, including Apple (AAPL), Amazon (AMZN), Meta (META), and Microsoft (MSFT). Here’s a small sample:

●Monday: F5 (FFIV), NXP Semiconductors (NXPI), Rambus (RMBS), Teradyne (TER), Waste Management (WM)

●Tuesday: General Motors (GM), Honeywell (HON), Kraft Heinz (KHC), Coca Cola (KO), Martin Marietta (MLM), Altria (MO), Pfizer (PFE), Spotify (SPOT), United Parcel Service (UPS), Booking Holdings (BKNG), Lemonade (LMND), Qorvo (QRVO), Starbucks (SBUX), Visa (V)

●Wednesday: Automatic Data Processing (ADP), Caterpillar (CAT), Vulcan Materials (VMC), Yum Brands (YUM), Albemarle (ALB), eBay (EBAY), Meta (META), Microsoft (MSFT), Qualcomm (QCOM)

●Thursday: Baxter (BAX), CVS Health (CVS), Estee Lauder (EL), Hershey (HSY), Kellanova (K), Eli Lilly (LLY), Mastercard (MA), McDonald's (MCD), Moderna (MRNA), Roblox (RBLX), Apple (AAPL), Airbnb (ABNB), Amazon (AMZN), Duolingo (DUOL)

●Friday: Apollo Global Management (APO), Cboe Global Markets (CBOE), Cigna (CI), Chevron (CVX), DuPont (DD), Eaton (ETN), Magna (MGA), Wendy's (WEN), Exxon Mobil (XOM)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Overweight weight-loss drugs?

While acknowledging recent debate regarding the ability of GLP-1 weight-loss drugs to significantly expand their footprint, Morgan Stanley & Co. strategists now project a peak potential market of approximately $150 billion, globally—up from their April 2024 estimate of $105 billion.2

And not all of the companies they expect to benefit are named Eli Lilly (LLY) and Novo-Nordisk (NVO), makers of two of the most popular GLP-1 drugs, Zepbound and Wegovy.

While the analysts’ previous forecasts for expansion were based on the US market, they now see international demand driving growth. For more details, see the report, “Obesity Medications: The Broadening.”

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 The Wall Street Journal. Trump Says He Has ‘No Intention’ of Firing Fed Chair Powell. 4/22/25.

2 MorganStanley.com. Obesity Medications: The Broadening. 4/24/25.