Essential strategies for managing your investments during market downturns

E*TRADE from Morgan Stanley

Summary: Investors can use these six principles to not only mitigate risk during market volatility but also keep anxiety in check.

Investing during periods of market volatility can be a daunting experience. The sight of fluctuating account values can unsettle even the most seasoned investors. However, understanding the dynamics of bear and bull markets, alongside adopting a disciplined investment strategy, can potentially help you ease the anxiety associated with these market fluctuations.

1. Understand market dynamics

Living through a bear market can be a difficult experience, but it inevitably happens as market volatility is not an anomaly but a regular aspect of the financial markets. Since 1965, the US equity markets have experienced ten bear markets, lasting an average of 13 months with a typical decline of 29% in the S&P 500®. On the other hand, the markets have also seen nine bull markets during the same period lasting an average of 56 months and resulting in an average increase of 178% in the S&P 500®. These statistics highlight a crucial fact: markets tend to rise for longer periods than they fall, and the extent of the upward movement tended to be substantially greater than the downward movement. So don’t get anxious; try to keep everything in perspective.

2. Keep your emotions in check

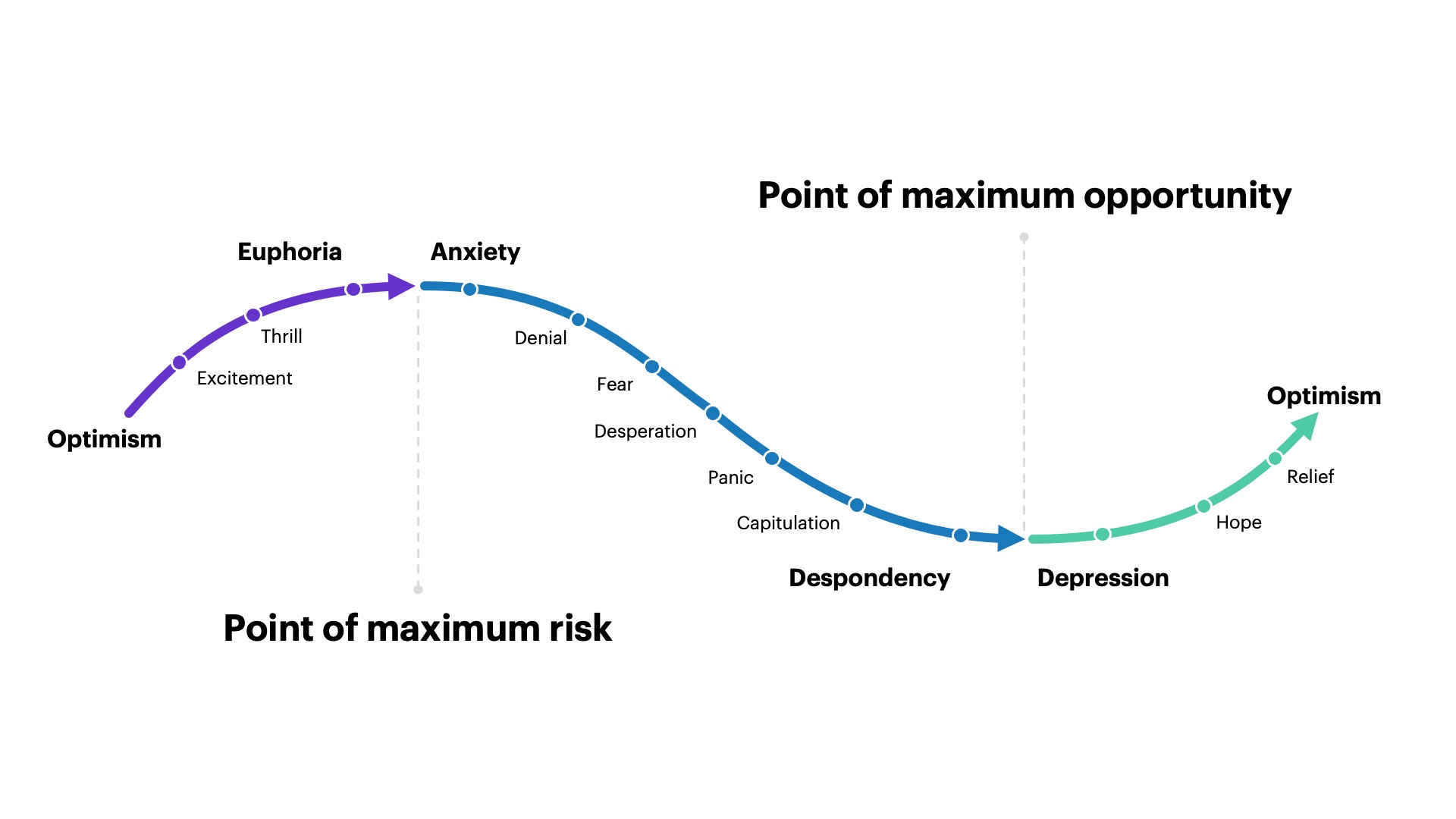

One of the most common pitfalls for investors is allowing emotions to drive investment decisions. Fear of unfavorable market conditions can often contribute to poor timing in buying and selling.

It generally doesn’t pay to try to time the market. Disciplined investors who hold a diversified mix of investments through both good times and bad typically earn higher returns than those who try to repeatedly buy and sell. For instance, in March 2009, the Dow Jones Industrial Average plummeted to approximately 6600, down from a high of 14,000. Many investors wanted to sell during this downward movement with the intention of getting back into the market once the price was improved, but a risk of this strategy was not timing the recovery correctly and resulting in buying high and selling low, exactly the opposite of what they should be doing. Historical data and expert analysis suggest that maintaining a diversified investment portfolio and holding steady through market ups and downs typically yields higher returns.

It’s easy to let emotions get in the way

Having a plan and sticking to it can help you avoid common mistakes, such as buying and selling at the wrong time out of panic or exuberance.

Source: Morgan Stanley Wealth Management Global Investment Office

3. Trust the importance of diversification

We can’t stress this one enough: Don’t keep all your eggs in one basket. Diversification is a fundamental investing principle and having a diversified portfolio is critical during a market downturn. Spreading investments across various asset classes such as stocks, bonds, and cash, may help you mitigate the risks associated with market fluctuations. That’s because historically, different asset classes often do not move in tandem; for example, when stocks decline, bonds might rise. Of course, the right mix of assets depends on your goals, timeframe, and risk tolerance.

4. Be sure to rebalance your investments

As market conditions fluctuate, the value of your holdings can also change in relation to each other, drifting from your target allocation amounts. Therefore, it’s important to rebalance your portfolio periodically. Rebalancing simply means returning your portfolio back to the original desired level of asset allocation percentages. This is done by selling any overweight asset classes (those that have risen in value) and buying the underweight asset classes (those that have fallen in value). This practice not only keeps your portfolio aligned with your long-term investment strategy but also enforces the discipline of buying low and selling high. What’s more, rebalancing may result in higher cumulative total returns with less volatility than a portfolio that’s not rebalanced.

A well-crafted financial plan takes into account your investment timeframe and risk tolerance, helping to ensure that you are neither overexposed nor underexposed to risks.

5. Create and stick to a financial plan

Creating and adhering to a long-term financial plan can provide immense peace of mind during turbulent market periods and instill confidence. Markets will go up and down, and you will likely experience several major declines over several decades. Knowing when those ups and downs will happen or how long they will last is impossible.

A well-crafted financial plan takes into account your investment timeframe and risk tolerance, helping to ensure that you are neither overexposed nor underexposed to risks. Research indicates that long-term financial planning may significantly enhance average annual total returns, helping you to achieving your financial objectives.

6. Don’t hesitate to ask for help

Navigating the complexities of volatile markets can be overwhelming and there’s no reason you have to face market uncertainty alone. E*TRADE from Morgan Stanley offers an array of online tools and resources and advice to help you choose investments and build a diversified portfolio. We also offer Core Portfolios to help you navigate the markets. These services can help you select suitable investments and build a diversified portfolio tailored to your financial goals.

Consider speaking to a Financial Advisor about investment strategies consistent with your goals and objectives.

CRC# 4095409 01/2025

How can E*TRADE from Morgan Stanley help?

Brokerage account

Investing and trading account

Buy and sell stocks, ETFs, mutual funds, options, bonds, and more.

Certificates of Deposit (CD)

Now, lock in 4.40% Annual Percentage Yield1,2 for 12 months for a limited time

Secure a fixed rate when you open and fund a new Bank CD. Additional terms available from to .3

Morgan Stanley Private Bank, Member FDIC.

Bonds

Gain direct access to more than 50,000 bonds and fixed income products from issuers of every kind.

Risk Assessment Tool

How risky is your portfolio?

Understanding risk is key to managing your investment performance. See your portfolio’s volatility, asset allocation and how you might fare in different hypothetical market scenarios.