What is portfolio rebalancing and why should you care?

E*TRADE from Morgan Stanley

Summary: Rebalancing your portfolio is an important factor when aiming to meet your financial goals.

When you think about your portfolio's asset allocation, there's a related idea—rebalancing—that goes hand-in-hand with it. Essentially, rebalancing means selling some assets in your portfolio and buying others to help maintain your target asset allocation. This is especially important during times of significant market volatility.

Understanding rebalancing–and doing it well–is important in helping you meet your investing goals.

Why rebalance?

Changes in the market can cause your portfolio to drift from your target asset allocation. Over time, some assets may perform well and become a larger portion of your portfolio, while others may do poorly and shrink as a percentage of your investments.

When a portfolio drifts away from its target asset allocation, it may get riskier or, conversely, more conservative with potentially lower gains. Rebalancing allows you to realign your portfolio with your risk tolerance and overall investing strategy.

How it works

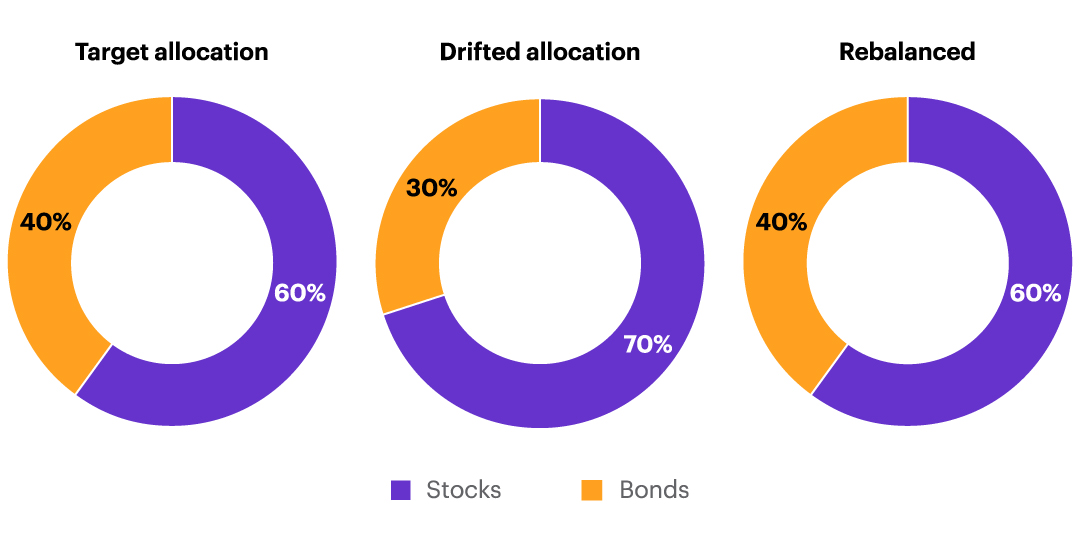

The basic idea is simple: Let’s say you start out with a mix of 60% stocks and 40% bonds, which has historically been known to provide investors with attractive risk-adjusted returns. Now, imagine that the market value of your stocks grows, but your bonds don't, and you end up with 70% of your portfolio value in stocks and only 30% in bonds. To rebalance, you would sell some of the stocks and buy more bonds—enough of both to bring the percentages back to 60/40.

Of course, your asset allocation is probably more granular than simply stocks vs. bonds. Let’s say that within your stock holdings, your asset allocation calls for certain percentages of large cap, mid cap, and emerging market stocks. Rebalancing can also correct drift from targets within those sub-categories.

For illustrative purposes only

When to rebalance: two approaches

How often you rebalance may sometimes be a balancing act itself. If you rebalance too often, you might miss out on some potential momentum gains, but if you don’t rebalance enough your portfolio may no longer be on track to meet your individual, financial goals. There are generally two approaches to rebalancing:

Calendar-based rebalancing

The calendar-based approach adjusts your portfolio on a regular timetable, such as quarterly or annually.

- Pros: Calendar-based rebalancing is simple to implement.

- Cons: Rebalancing may be out-of-sync with the actual changes in your portfolio's asset allocation. For example, a significant drift could happen between rebalancing intervals. Conversely, rebalancing could occur even if there was only a small change in your portfolio, potentially triggering an unwanted taxable capital gain (more on that below).

Trigger-based rebalancing

A method of rebalancing when a portfolio drifts beyond certain pre-determined limits—for example, if an asset class changes by 10% or more relative to its target allocation.

- Pros: Rebalances promptly when the portfolio drifts too far from its predetermined asset allocation goal but doesn't rebalance excessively or unnecessarily.

- Cons: The method may be a bit more difficult to implement. Also, in periods of high market volatility, trigger-based rebalancing might occur more frequently, resulting in potentially-taxable capital gains.

The bottom line is that rebalancing is one of the most critical parts of managing a portfolio, and it is key to keeping your investments aligned with your long-term goals.

CRC# 3669458 07/2024

How can E*TRADE from Morgan Stanley help?

Prebuilt Portfolios

Select your risk tolerance and easily invest in diversified, professionally selected portfolios of mutual funds or exchange-traded funds (ETFs). And you pay no trading commissions although fund fees and expenses still apply.

Get started with as little as $500 (mutual funds) or $2,500 (ETFs).

Risk Assessment Tool

How risky is your portfolio?

Understanding risk is key to managing your investment performance. See your portfolio’s volatility, asset allocation and how you might fare in different hypothetical market scenarios.

Review your portfolio’s performance

Use our interactive charts to view your rates of return over various time periods and compare your portfolio against multiple benchmarks.

Brokerage account

Investing and trading account

Buy and sell stocks, ETFs, mutual funds, options, bonds, and more.