How should investors think about long-term bitcoin returns?

Morgan Stanley Wealth Management

07/21/26How should investors expect bitcoin to perform in the coming decade? Here’s a framework to consider.

Key takeaways:

- Bitcoin’s remarkable average annual return over the last 10 years is unlikely to be repeated in the next decade.

- Investors can try to forecast bitcoin’s long-term returns using factors such as bitcoin’s supply, demand and assumptions on penetration.

- Under five different assumptions, the 10-year annualized return estimates range from a more bearish 3% to a more aggressive 10%.

- Some potential risks to investing in cryptocurrencies include broken encryption, software bugs, adverse government action, or loss of the entire investment.

Why does bitcoin matter to investors today?

Bitcoin, the world’s largest cryptocurrency, continues to draw attention due to volatile price movements. It has evolved from being thought of as purely a payment system to owners choosing to hold bitcoin for its store-of value properties1 and its allure as a financial asset. This has many investors wondering: How might bitcoin potentially fit into my portfolios and how can I go about estimating its performance from here?

For starters, cryptocurrencies are not for everyone, and forecasting bitcoin’s price can be notoriously challenging, given its short history and high volatility. While it has shown an unusually high average annual return over the last 10 years, Morgan Stanley strategists believe this performance is unlikely to be repeated in the next decade.

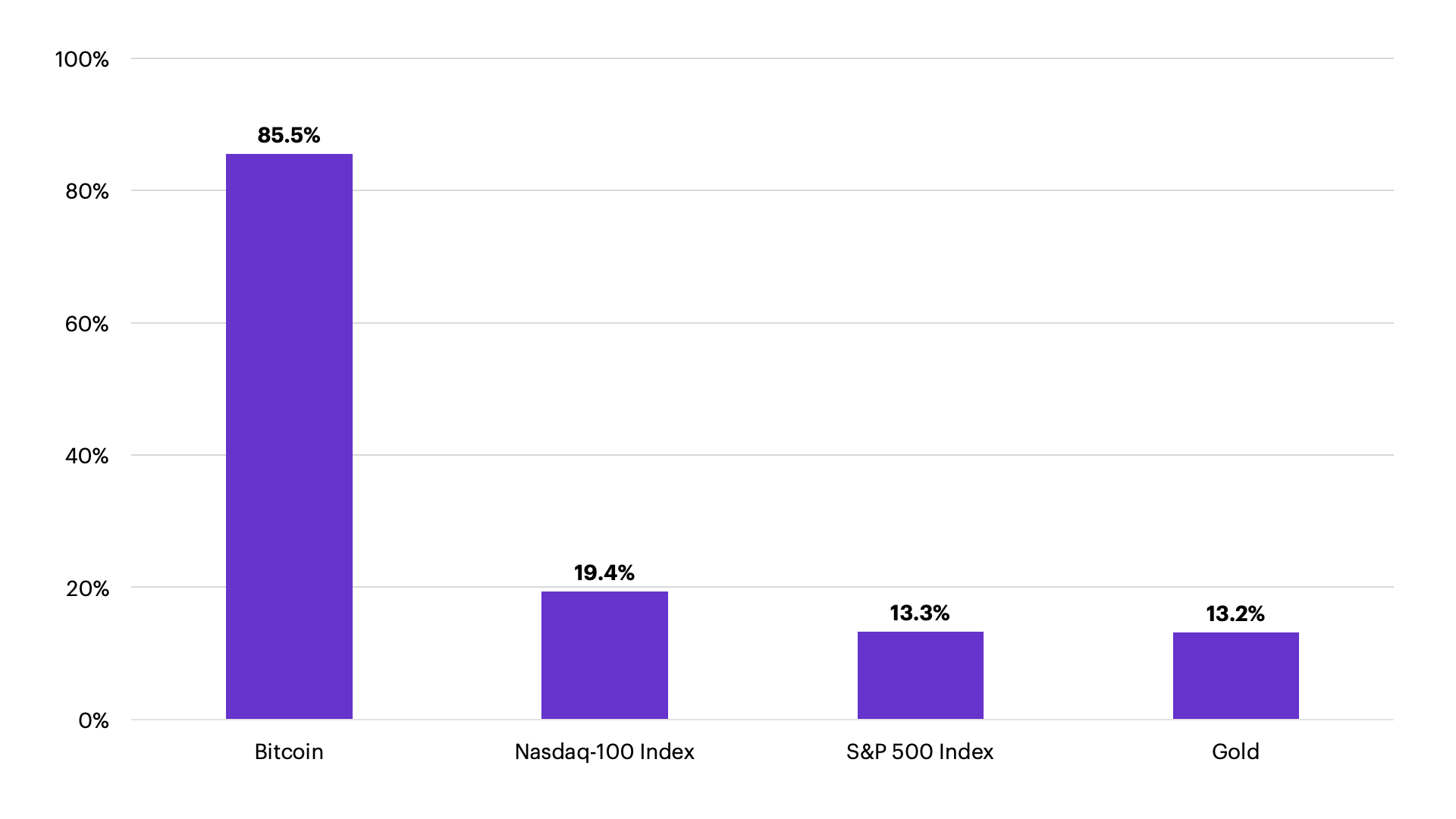

Bitcoin Has Risen Much Faster Than Other Assets Over the Past 10 Years

Source: Bloomberg, Morgan Stanley Wealth Management Global Investment Office as of Sept. 30, 2025

Past performance does not guarantee future results. Investing in cryptocurrency is highly speculative and may result in a loss of the entire investment. An investment cannot be made directly in a market index.

Forecasting potential bitcoin returns

Instead of treating cryptocurrencies like stocks or bonds, which are often valued based on projected cash flows, it may be useful to look at crypto assets as commodities2, which are priced based on supply and demand.

Using this framework, investors may consider three factors:

Supply

Supply is the easiest to forecast, as the software underlying bitcoin's network controls its growth. Today, the bitcoin money supply stands at approximately 19.9 million and is set to grow to approximately 20.8 million in the next 10 years. This supply limit is enforced by the governing algorithm and cannot change unless users agree.

Demand is the product of two assumptions: the addressable market and penetration.

The addressable market

The addressable market refers to the amount of wealth that could potentially be stored in bitcoin. For simplicity, investors can focus on liquid assets that can quickly be converted to cash, such as checking accounts, savings accounts, and other short-term saving vehicles such as certificates of deposit—what’s known by economists as the “M2” money supply—as well as gold and bitcoin. Today, Morgan Stanley strategists see around $130 trillion stored globally in such assets, based on October 2025 prices.

Penetration

Penetration can refer to the percentage of overall wealth actually stored in bitcoin. Simply dividing bitcoin’s market capitalization of $2.2 trillion as of October 2025 by $130 trillion in wealth, as defined above, suggests it has a penetration of about 2%.

Alternately, investors may define “penetration” as the percentage of investors with exposure to bitcoin in their portfolio.

Five potential scenarios for bitcoin’s long-term returns

Bitcoin supply growth has the least uncertainty and it is expected to grow about 0.8% in 2026 and trend lower over time as future halvings occur. For the growth of the addressable market, Morgan Stanley Strategists combine near-term M2 growth with the long-term average M2 growth. The last variable, penetration, is a wildcard and makes the most difference to long-term returns.

Here are five illustrative examples, but everyone’s estimates are likely to differ substantially, and Morgan Stanley does not favor any one estimate.

A Conservative Approach:

If bitcoin adoption has already peaked—meaning no meaningful new investors arrive and current holders don’t increase how much they own—bitcoin’s price would likely rise mostly in line with overall wealth. Because wealth can grow faster than bitcoin’s supply, the price per bitcoin could still increase. Using 10-year assumptions of 6.8% M2 growth and 0.4% supply growth, the model implies a 6.4% annualized return over 10 years.

A Moderately Aggressive Approach:

Alternately, you could assume bitcoin users will grow with the US population, and that younger people are more likely to adopt bitcoin than older ones. If bitcoin adoption grows alongside the U.S. population—and new users have similar wealth and allocate a similar share to bitcoin—demand could grow with M2 plus population, at roughly 7.6%. After adjusting for supply growth, that suggests a 7.2% annualized 10-year return.

A More Aggressive Approach:

Bitcoin is becoming more popular and easier to buy. If monthly active user growth continues at its 2019–2025 rate of 3.4% for the next five years and remains at that pace for a full decade, the bitcoin supply and M2 assumptions imply a 9.8% annualized 10-year return.

A Bearish Approach:

Adoption doesn’t always move in one direction. Some investments appear to be gaining traction and then lose momentum due to scaling limits, tougher regulation, competition, or a major software issue that raises doubts about long-term viability. Since 2023, average monthly bitcoin transactions have declined at about a 2.2% annualized rate. If that trend continues, the model points to a 4.2% annualized return over 10 years.

A Sudden Drop in Penetration:

The biggest risks are a failure of bitcoin’s encryption or a serious software bug. Historically, smaller bugs across Bitcoin, Ethereum, and other blockchains have caused short-term drops in price and activity but has not reversed long-term adoption. Investors could see a larger or smaller adoption decline depending on how severe an unexpected event turns out to be.

Long-term return forecasts for bitcoin vary based on various penetration assumptions

| Penetration Assumption | Rationale | Penetration 10-Year CAGR (%) | Bitcoin Supply 10-Year CAGR (%) | M2 Growth 10-Year CAGR (%) | Annualized implied 10-Year Bitcoin Return (%) |

|---|---|---|---|---|---|

| No change | No change inpenetration | 0.0 | 0.4 | 6.8 | 6.4 |

| Grows in line with population | More popular with younger generations, might gain share as population grows | 0.8 | 0.4 | 6.8 | 7.2 |

| Grows with historical adoption curve | Previous adoption curve predicts future adoption | 3.4 | 0.4 | 6.8 | 9.8 |

| Shrinks with historical adoption curve | Monthly average transactions continue to decline at the 2023-2025 rate | -2.2 | 0.4 | 6.8 | 4.2 |

| Sudden drop in penetration | Encryption breaks within next 10 years, then adoption recovers | -3.8 | 0.4 | 6.8 | 2.6 |

Source: BlockWorks, Morgan Stanley Wealth Management Global Investment Office as of Oct 23, 2025.

For illustrative purposes only. There is no guarantee that these estimates will come to pass. Investing in cryptocurrency is highly speculative and may result in a loss of the entire investment.

Investors can use this framework to explore what they think will happen to money supply, user growth and penetration — and plan accordingly.

Consider the risks

It’s important to note that these estimates are illustrative of the three-variable framework, and Morgan Stanley does not endorse any of these assumptions. Further, they do not factor in potential major risks, such as adverse government actions.

These are hard to quantify and thus suggest investors err on the side of conservatism in their other assumptions. While these scenarios may be off the mark, they can still be useful for planning purposes. Most importantly, investors can use this framework to explore what they think will happen to money supply, user growth and penetration — and plan accordingly.

Morgan Stanley’s Global Investment Office makes no recommendation regarding whether to buy or sell bitcoin but encourages investors to get educated. Ultimately, investing in bitcoin or any other cryptocurrency should be based on thorough research and understanding of the asset class. Investing in cryptocurrency is highly speculative and may result in a loss of the entire investment.

1 Generally, a store-of-value asset should be liquid, should not deteriorate with time and should hold its value over time. Many bitcoin holders believe it has these characteristics, while others disagree.

2 Although this analysis is comparing bitcoin to commodities for the purpose of estimating returns, bitcoin has its own features and risks that are different than commodities. Specifically, bitcoin is a digital commodity subject to software and encryption risk which most other commodities do not have. Also, unlike most commodities it is not used up, it’s always available unless lost.

The source of this article, AlphaCurrents Crypto: A Framework for Long-Term Return Assumptions, by Denny Galindo, Sophia Psaila and Aashi H. Tailor, was originally published on December 9, 2025.

CRC#5714935 07/2026

How can E*TRADE from Morgan Stanley help?

Bitcoin Exchange-Traded Products (ETPs)

Spot bitcoin ETPs and futures-based bitcoin exchange-traded funds (ETFs) make it simple to invest in bitcoin without the trouble of owning the cryptocurrency itself.

Cryptocurrency

Explore how you can gain indirect exposure to popular cryptocurrencies via securities and futures at E*TRADE.