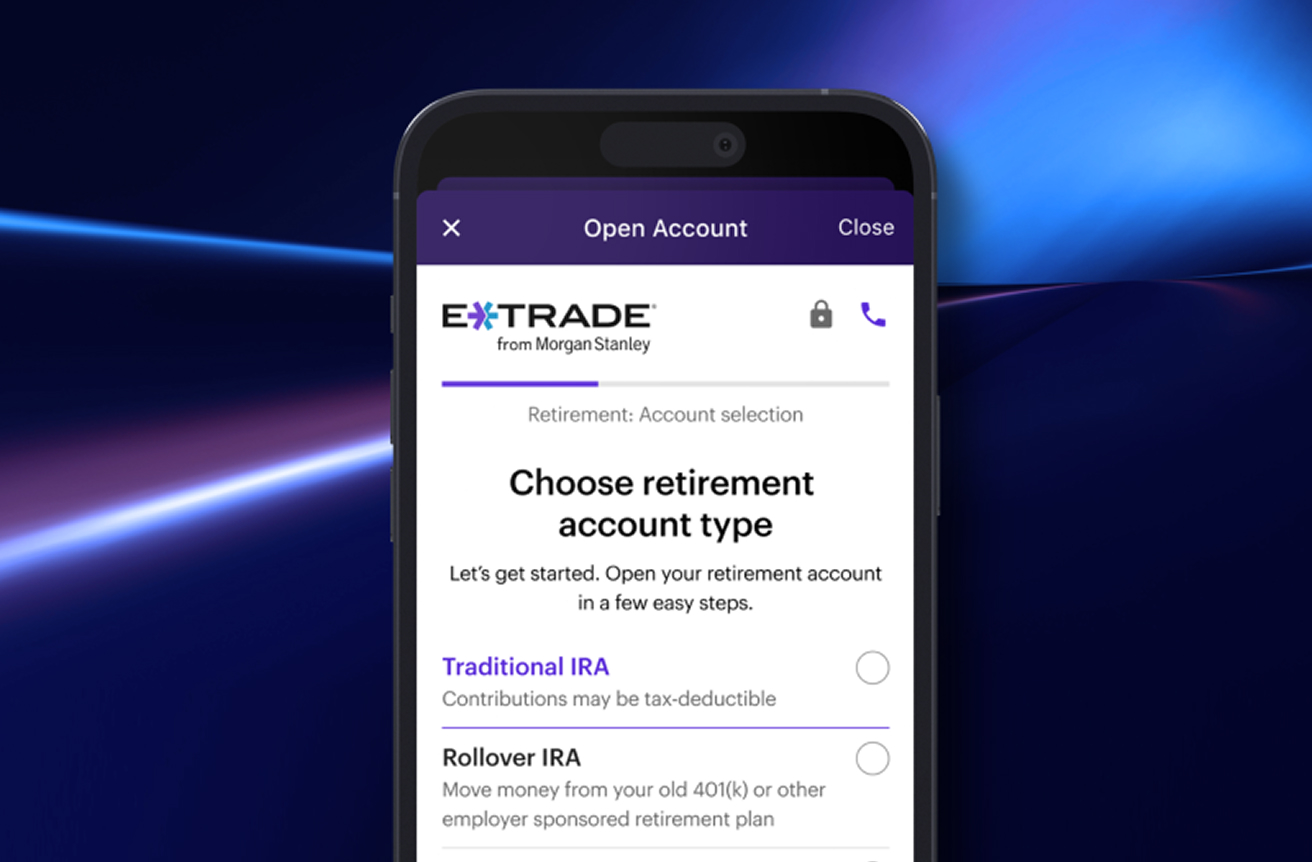

Retirement accounts

Take on your retirement with E*TRADE

Invest for the future with tax-qualified retirement accounts, easy-to-use tools, and a special limited-time cash credit.

Get up to $10,000 for a limited time1

Put our retirement accounts to work for you

Whether you're just starting to save for retirement or are weighing what to do with an old 401(k) or 403(b)2, we've got the tax-qualified accounts you may need.

Rollover IRA

Consider moving your 401(k)/403(b)2

Traditional IRA

Build your retirement nest egg

Roth IRA

Invest after-tax dollars

E*TRADE CompleteTM IRA

Inherited IRA

Small business plans

Get up to $10,000 cash credit1

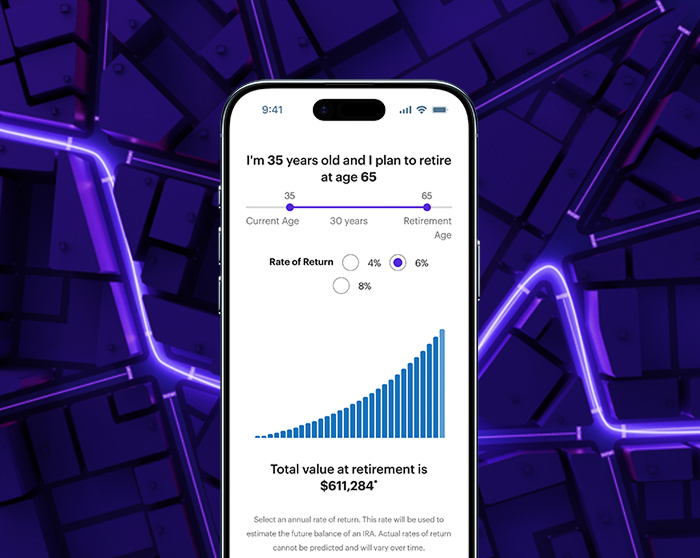

Retirement planning

Invest in tomorrow by starting today

Use our retirement calculator to see how much your savings could potentially grow in a tax-qualified retirement account.

Three reasons to invest with an E*TRADE retirement account

1

Fee-free accounts

2

Wide range of offerings

3

Easy to use

Awards and recognition

E*TRADE Retirement Accounts won 'Best in Class' in Stockbrokers.com 2026 Annual Awards.

Education and resources

Insights to stay informed and inspired

Which IRA could be right for me?

Four things you should consider before rolling over your 401(k)

Understanding required minimum distributions (RMDs)

Frequently asked questions

-

An investor can contribute to an IRA account by transferring funds online from a bank or brokerage account, sending a check, or completing a wire transfer. For more information about ways to make a deposit to an account, see the Help topic, Contribute to an IRA account.

An investor is allowed to contribute 100% of earned income up to the annual contribution limit. View IRA Contribution Limits and Deadlines to learn more.

-

Requesting a distribution online may allow for faster access to funds. Complete the online form to get started. The request should be processed and on its way in 3–5 business days.

-

General:

- Must be 18 years of age or older with taxable compensation

- Must have Modified Adjusted Gross Income (MAGI) under certain thresholds (see ‘Single Filers’ or ‘Joint Filers’ for additional information). If your MAGI exceeds the MAGI limitations to contribute to a Roth IRA, you can still contribute to a Traditional IRA, but contributions will not tax deductible; however, you may still benefit from the potential of tax-deferred growth. Additionally, Traditional IRA assets may be converted to a Roth IRA, but the taxable portion of the converted assets will be subject to ordinary income taxes.

- To apply online, you must be a U.S. citizen or resident.

- Can open and make a contribution to your Roth IRA for a tax year at any time during the tax year or by your federal tax return filing deadline (not including extensions). This date is generally April 15 of each year. Applications postmarked by this date will be accepted.

Single Filers:

- If an investor’s MAGI is $153,000 or less in 2026, they may be eligible to make a full contribution. If their MAGI is between $153,000 and $168,000 in 2026, they may be eligible to make a partial contribution. An investor is not eligible to make a contribution if their MAGI is $168,000 or more in 2024.

Married, filed jointly:

- If a couple’s combined MAGI is $242,000 or less in 2026, they may be eligible to make a full contribution. If their combined MAGI is between $242,000 and $252,000 in 2026, a couple may be eligible to make a partial contribution. They are not eligible to make a contribution if MAGI is $252,000 or more in 2026.

Note: Modified adjusted gross income (MAGI) is used to determine whether an individual qualifies for certain tax deductions or other benefits. Most notably, it is used to determine how much of an individual's IRA contribution is deductible (if the individual or their spouse is covered by a workplace retirement plan) and whether an individual is eligible to contribute to a Roth IRA.

-

General:

- Must be 18 years of age or older with taxable compensation

- Must have Modified Adjusted Gross Income (MAGI) under certain thresholds to make tax-deductible contributions if you or your spouse is an active participant in an employer-sponsored retirement plan

- To apply online, you must be a U.S. citizen or resident

- Can open and make a contribution to your Traditional IRA for a tax year at any time during the tax year or by your individual federal tax return filing deadline (not including extensions). This date is generally April 15 of each year. Applications postmarked by this date will be accepted.

- Participation in an employer-sponsored retirement plans, such as a 401(k), 403(b), or 457 plan, may impact your ability to make tax-deductible contributions to your Traditional IRA. If neither you nor your spouse participates in an employer-sponsored plan, you may be able to make a contribution to your Traditional IRA that is fully deductible.

Single Filers:

- If taxpayer participates in an employer-sponsored retirement plan, and taxpayer’s MAGI is $77,000 or less in 2024 (or $79,000 or less in 2025), taxpayer may be eligible to deduct the entire contribution. If taxpayer’s MAGI is more than $77,000 but less than $87,000 in 2024 (or more than $79,000 but less than $89,000 in 2025), taxpayer may be eligible to deduct part of the contribution. Taxpayer is not eligible to make a tax-deductible contribution if MAGI is $87,000 or more in 2024 (or $89,000 or more in 2025).

Joint Filers:

- If taxpayer participates in an employer-sponsored retirement plan, and taxpayer’s MAGI is $123,000 or less in 2024 (or $126,000 or less in 2025), taxpayer may be eligible to deduct the entire contribution. If taxpayer’s MAGI is more than $123,000 but less than $143,000 in 2024 (or more than $126,000 but less than $146,000 in 2025), taxpayer may be eligible to deduct part of the contribution. Taxpayer is not eligible to make a tax-deductible contribution if MAGI is $143,000 or more in 2024 (or $146,000 or more in 2025).

- If taxpayer does not participate in an employer-sponsored retirement plan, but taxpayer’s spouse does, then the MAGI limits are different. If taxpayer’s MAGI is $230,000 or less in 2024 (or $236,000 or less in 2025), taxpayer may be eligible to deduct the entire contribution. If taxpayer’s MAGI is more than $230,000 but less than $240,000 in 2024 (or more than $236,000 but less than $246,000 in 2025), taxpayer may be eligible to deduct part of the contribution. Taxpayer is not eligible to make a tax-deductible contribution if MAGI is $240,000 or more in 2024 (or $246,000 or more in 2025), and taxpayer’s spouse participates in an employer-sponsored retirement plan.

-

401(k) or other employer-sponsored retirement plan assets may be rolled over to an E*TRADE IRA.

E*TRADE has teamed up with Capitalize to make rolling over a 401(k) simpler. When you open a new E*TRADE IRA, Capitalize can help navigate the rollover process for funding your account.

Learn about 4 options for rolling over your old employer plan arrow_forward

-

There are several options available to Inherited IRA beneficiaries. The options depend on whether the beneficiary is a spouse or non-spouse, and how old the original account holder was when they passed away. Use the Inherited IRA tool to help understand the options.