What are small business retirement plans?

E*TRADE from Morgan Stanley

05/23/24Small business owners have many critical priorities, such as growing their business, making a profit, managing taxes, and attracting and rewarding valuable employees. A small business retirement plan may help them achieve these objectives. Most small business plans are easier to start up, less expensive to run, and simpler to manage than a typical employer sponsored qualified retirement.

What is a small business retirement plan? A small business plan is a tax-deferred plan that offers retirement savings for self-employed individuals and their spouses, or small business owners. Some define a small business owner as a business owner with less than 10 employees, but one of the plans we offer - a SIMPLE IRA - can be used as long as you have less than 100 employees. One of the advantages of a small business plan is that business owners can deduct contributions made to their own accounts, as well as contributions made on behalf of employees, as a business expense.

Who is eligible to set up a small business retirement plan? Anyone who has earned income from self-employment can establish a small business retirement plan. Examples include consultants, independent contractors, board members, store owners, sales representatives with 1099-MISC income, doctors, attorneys, real estate agents, people with home based businesses, and many more. Whether self-employed income is the primary income source, or an individual just has a small business on the side and continues to work for someone else, they are eligible to set up a small business retirement plan, using the income derived from being their own boss.

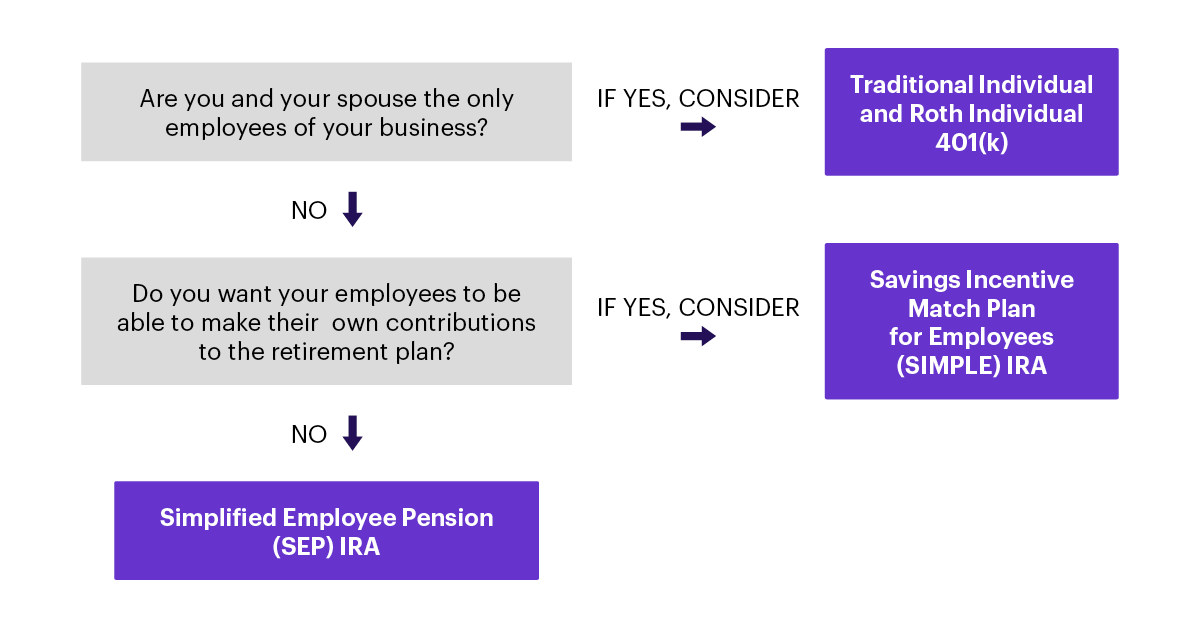

Three small business and self-employed retirement plans include: Individual 401(k) which offers a Roth 401(k) feature, SEP IRA, and a SIMPLE IRA.

Individual 401(k)

An Individual 401(k) plan is designed to maximize contributions for self-employed individuals and spouses, and it’s less complex and less costly to maintain than a conventional 401(k) plan. The first thing to understand about an Individual 401(k) is that contributions can come from two sources.

Owner's salary deferral

How this works is that the business owner defers, or foregoes, a percentage or dollar amount of their salary up to a maximum of $22,500 for 2023 ($23,000 for 2024). If over age 50, they can defer an additional $7,500 for 2023 and 2024, for a total of $30,000 for 2023 (and $30,500 for 2024) into the plan. Salary deferrals can be used to reduce income and thus tax liability now. Alternatively, they can designate all or a portion of salary deferrals as an Individual Roth 401(k) contribution if the plan permits. With a Roth contribution, the contribution cannot be deducted now, but the business owner can take tax-free qualified distributions later if certain requirements are met. A qualified distribution is generally a distribution that is made after a 5 year holding period and after age 59½.

Company contribution

The second part of the contribution is the company contribution, also called a profit sharing contribution. This piece can be as much as 25% of your income if the business is incorporated (or if the business owners receives a W-2), or 20% of income if they are a sole proprietor and file a Schedule C. The total of the two contribution pieces (salary deferral plus profit sharing) can total up to as much as $66,000 for 2023 ($69,000 for 2024). These limits are increased by 7,500 for 2023 and 2024 if age 50 or over. This plan allows a business owner to put away quite a large sum for retirement.

A traditional individual 401(k) and Roth Individual 401(k) can also offer a loan feature, giving the opportunity to take a loan in the event of a setback. Generally, 50% of the vested account balance, up to $50,000 can be borrowed if permitted under the plan.

If there are any full or part-time employees other than a spouse, a small business owner is not able to establish this plan.

SEP IRA

Another popular plan for small businesses is a SEP IRA. A SEP IRA is very similar to a Traditional IRA, except it has higher discretionary contribution limits. The contribution limits for SEP IRAs are the lesser of (i) $66,000 in 2023/$69,000 in 2024 or (ii) 25% of employee compensation (or 20% of net earnings from self-employment), with compensation taken into account capped at $330,000 in 2023/$345,000 in 2024. The contributions made to a SEP IRA are generally not mandatory. Employers are generally able to set aside from 0 – 25% each year. Therefore, if they have a good year, they can generally put away the maximum amount. If on the other hand, they didn’t have as successful of a year as hoped, they can put away a small percentage or even skip a year of contributing altogether. Keep in mind that only employers can make SEP IRA contributions. So whatever percentage of salary a business owner contributes to their own SEP IRA, they must also contribute the same percentage of eligible employee’s salary into the eligible employee's SEP IRA accounts.

Business owners can let all employees participate in the SEP IRA or they can specify that a certain age and length of employment has to be met before contributions are made to employee accounts. The age limit cannot exceed 21 years old, the employment requirement is limited to 3 of the immediately preceding 5 years and received at least 750 in compensation (2023 and 2024) from the employer for the year. Once the employees exceed these requirements, business owners are obligated to contribute the same percentage of salary to their SEP IRAs as they contribute to their own account. This plan must be adopted by the business tax return filing deadline, plus extensions.

SIMPLE IRA

For employers who want employees to help fund their own retirement plan, they may be interested in a SIMPLRE IRA. A SIMPLE IRA is sometimes described as a mini- 401(k) plan, but it is only available for businesses with no more than 100 eligible employees. Contributions are made both by the employer and the employee.

Employee salary reduction contributions

Employees defer a percentage of their salary into the SIMPLE IRA, up to $15,500 for 2023 (or $16,000 for 2024) or, if age 50 or older, $19,000 for 2023 (or $19,500 for 2024). The salary deferral contributions are typically deducted from the paychecks of each participant during normal payroll. Effective for the 2024 tax year, the annual deferral limit is increasing to 110% of the 2024 SIMPLE IRA plan limit (as indexed) and the catch-up contribution limit at age 50 is increasing to 110% of the 2024 SIMPLE IRA plan limit (as indexed) in the case of an employer with no more than 25 employees. Employers with 26 to 100 employees are permitted to provide these higher deferral limits, provided that the employer either provides a 4% matching contribution or a 3% employer non-elective contribution (electing employer SIMPLE plan).

Employer contributions

Then the employer either matches contributions of employees that are participating in the plan, up to 3% (or 4% for electing employer SIMPLE plan) of salary, or can choose to provide a 2% (or 3% for electing employer SIMPLE plan) non-elective contribution to all eligible employees (the 2% non-elective contribution is subject to the compensation cap of $330,000 for 2023 or $345,000 for 2024), whether the employees participate in the salary deferral portion of the plan or not. Effective for the 2024 tax year, employers are permitted to make additional contributions to each participant in a uniform manner, provided the additional contribution does not exceed the lesser of 10% of a participant's compensation or $5,000 (as indexed).

One advantage of providing a 3% matching contribution is that the employer only contributes to those employees who elect make a salary reduction contribution. An advantage of the 2% non-elective contribution is that these contributions are subject to a compensation cap -- however they’ll have to contribute for all eligible employees even if they don’t participate in the salary deferral portion of the plan.

Two important things to know about SIMPLE IRAs are:

1. A vesting schedule cannot be imposed on the employer contribution, meaning that even if an employee leaves the company soon after they become eligible for an employer contribution, the money is still theirs to keep.

2. If the employees need to tap into their account within the first 2 years of funding, any withdrawals carry a hefty 25% tax penalty if the employees are under age 59 ½.

In general, the plan must be adopted by October 1 in order to make current year contributions.

Conclusion

The infograph below shows some options to help you find the small business retirement plan that may make sense for you.

Many business owners are too busy with the day to day details of running their business to think about planning for retirement. However, these plans are a way to help grow businesses and help employers retain and attract valuable employees. An employer sponsored retirement plan is often one of the crucial benefits individuals ask about when considering a new employment offer. Additionally, some plans have loan features, giving the opportunity to make a loan in the event of a setback. Also, tax credits exist for small business owners who establish new plans. Another big benefit is that contributions made to the employer’s account, or to employee accounts, are tax-advantaged. These contributions reduce the business’ taxable income and offer tax-deferred growth potential for the participants. Plus, contribution limits to these plans are much higher than the standard Traditional and Roth IRA contribution limits. A small business employer can control how much they contribute to their own account and employee’s accounts, and in some situations, employers may be able to skip funding one year if the business didn’t do as well as hoped.

How can E*TRADE from Morgan Stanley help?

Plan for your future

Explore easy-to-use planning tools and resources—designed to help you take control of your financial future.

Risk Assessment Tool

How risky is your portfolio?

Understanding risk is key to managing your investment performance. See your portfolio’s volatility, asset allocation and how you might fare in different hypothetical market scenarios.